- The Option Premium

- Posts

- 📩 The Option Premium Weekly Issue - March 15, 2026

📩 The Option Premium Weekly Issue - March 15, 2026

Fewer Than 30% of Stocks Are Above Their 50-Day. The Premiums Are the Richest All Year.

March 15, 2026

📰 What the Data Said This Week

The war continued. The selloff deepened. And the volatility map got even wider.

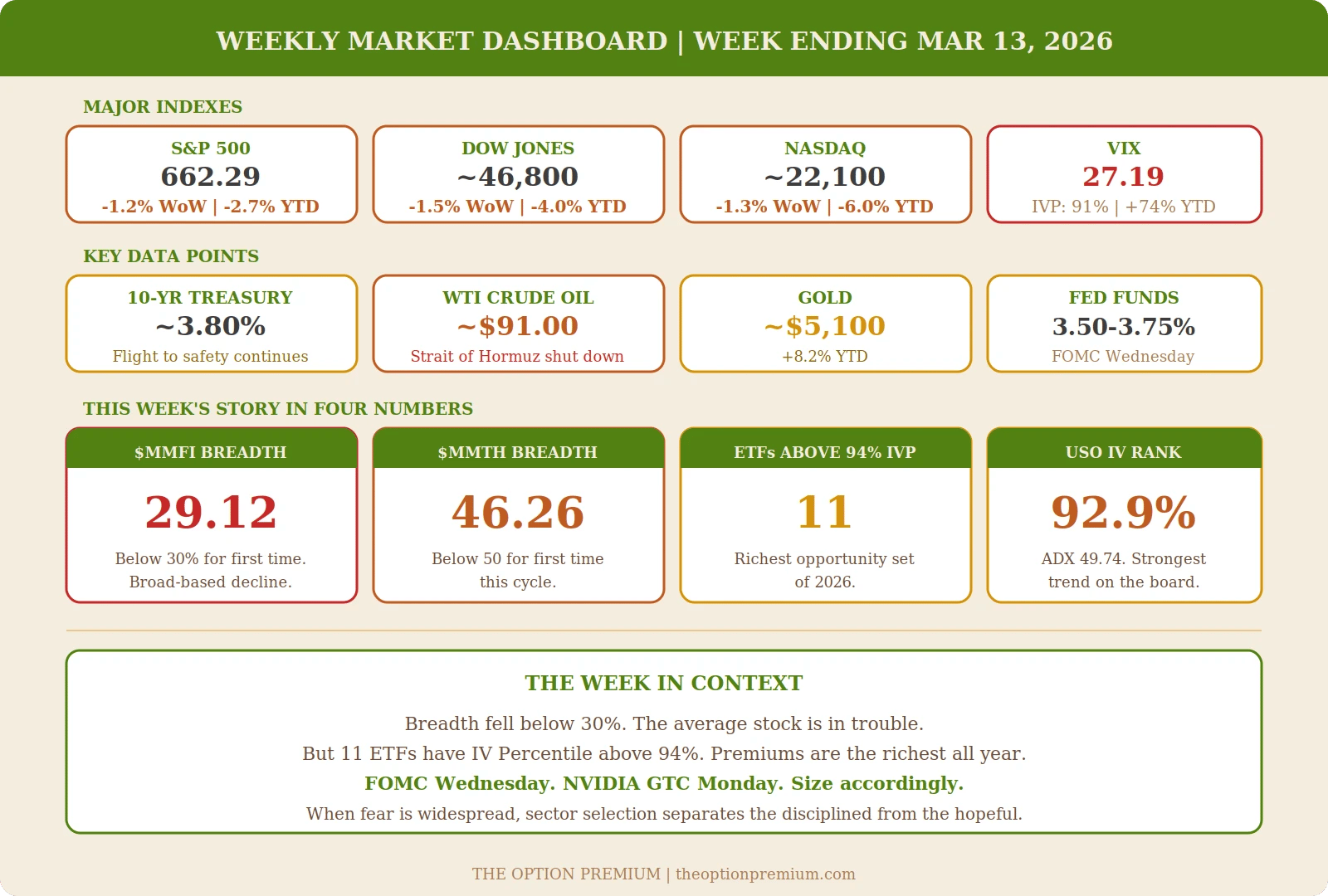

Markets fell for the second straight week as the U.S.-Iran conflict showed no signs of resolution. The S&P 500 dropped to 662.29, extending losses to roughly 4% off its January high. The Dow fell below 47,000. The Nasdaq slid further into negative territory for the year. The Russell 2000, once the lone bright spot, is barely clinging to positive YTD returns.

Oil remained the dominant force. WTI held above $90 after last week's historic 35% surge, with the Strait of Hormuz still effectively shut down. USO's IV Rank sits at 92.89% with 99% IV Percentile. That's not a spike. That's persistent, sellable elevation. Energy continues to be the only sector where +DI dominates and relative strength is rising. XLE's ADX hit 44.82 (institutional conviction). XOP and USO are following the same pattern. If you're not positioned in energy right now, the trend data is telling you something.

The breadth picture deteriorated significantly. $MMFI crashed to 29.12. Fewer than 30% of stocks are now above their 50-day moving average. $MMTH dropped below 50 for the first time this cycle at 46.26. Both indicators show "Below 30" RSI momentum with -DI above 48. This is no longer a narrowing rally or a rotation. This is a broad-based decline. The average stock is in trouble, even if the headline indexes don't fully reflect it yet.

The VIX cooled slightly to 27.19 from last week's 29.86 spike, but IV Percentile remains at 91%. Fear pulled back from its peak but premiums are still universally rich. Eleven ETFs have IV Percentile above 94% this week. That's the widest opportunity set we've seen all year for premium sellers.

CPI on Wednesday will set the tone going forward. With oil above $90 and last week's negative payrolls number still fresh, a hot print would put stagflation squarely on the table. A cooler reading could trigger the relief rally that contrarians have been waiting for. Either way, the 30-60 DTE window captures the aftermath without binary event risk.

NVIDIA's GTC conference begins Monday with Jensen Huang's keynote. Morgan Stanley expects a new four-year roadmap. After February's brutal tech selloff, this is the event that could reset the AI narrative. Watch semiconductor IV closely. SMH's IVR sits at 45.56% with 94% IV Percentile.

This week, Implied Perspective members received two new trade entries with specific strikes, deltas, and management plans before the market opened. Both are hedge-based. With IV metrics looking favorable, I plan to add two more trades this week. The full trade log and real-time alerts are part of every Implied Perspective subscription.

👉 [See what members are trading this week at theoptionpremium.com →]

📅 The Week Ahead

Date | Event | Time (ET) |

|---|---|---|

Mon, Mar 16 | NVIDIA GTC Keynote (Jensen Huang) | TBD |

Mar 16-19 | NVIDIA GTC Conference | All Week |

Wed, Mar 18 | FOMC Rate Decision + Press Conference | 2:00 p.m. |

Thu, Mar 19 | Weekly Jobless Claims | 8:30 a.m. |

The FOMC meeting Wednesday is the defining event. After negative payrolls and oil above $90, the market needs clarity on the Fed's thinking. Rate futures are pricing no change, but the statement and press conference will reveal how the Fed is weighing stagflation risk. NVIDIA's GTC runs simultaneously, creating a rare week where both macro and micro catalysts hit at once. Volatility should remain elevated.

📊 Weekly Market Stats

Index / Indicator | Close | Week | YTD |

|---|---|---|---|

S&P 500 | 662.29 | -1.2% | -2.7% |

Dow Jones | ~46,800 | -1.5% | -4.0% |

NASDAQ Composite | ~22,100 | -1.3% | -6.0% |

Russell 2000 | ~2,480 | -1.6% | +1.0% |

10-Year Treasury | ~3.80% | -5 bps | -39 bps |

WTI Crude Oil | ~$91.00 | +0.5% | +56% |

Gold | ~$5,100 | -1.0% | +8.2% |

VIX | 27.19 | -9% | +74% |

Fed Funds Rate | 3.50-3.75% | Unchanged | Unchanged |

The Numbers Don't Lie

Let's talk results. Both sides of our framework.

Credit Spreads (The Implied Perspective)

Our positions closed from March through April are showing a cumulative total return of 68.7%. Since last October, our cumulative return now stands at more than 186%. Not hypothetical. Not backtested. Every entry shared in real time with Implied Perspective members before the market opened.

“I highly appreciate your option trader services. I cannot remember ever having had a successful and instructive service like this in my 40 year career as an active investor!”…Stefan

“You explain options in a clear way & you try not to make them complex. That’s why I followed you. There are too many people on the net that teach options, but don’t explain them to ordinary people to make them understandable and comfortable to trade. They make them complicated. Most people I know say, oh you can lose lots of money, they’re dangerous, stay away! You know the story I am sure. They make these statements from hearsay. You’re not one of them. Keep the good work going Andy!”…Ian F.

“I just wanted to share with you my .02, this service so far has been the best investment I have made. I retired earlier this year with part of retirement strategy to live off my existing dividend income only and not touch the principal investments. Your trades have provided an additional income stream which has been very helpful. Thank you and keep up the great work!”…Ron

“Off and on, I have subscribed to different options services, and yours is by far the best for achieving high probability with reliable risk management. My win rate is 87% and my comfort level is high. Thanks for an excellent service!”…Anne

This is not one lucky trade. This is a process that works across different stocks, different market conditions, and different time periods.

2025 Small Dogs Portfolio: JNJ returned +93.49%. CSCO returned +77.40%. MRK returned +76.58%. KO returned +18.10%. VZ was our one loss at -8.30%. Portfolio total: +52.74%, turning $14,775 into $22,568. Four of five positions won. The one loss was small. The winners more than compensated.

Buffett Portfolio (closed): AAPL returned +69.67%. CVX returned +36.75%. AMZN returned +23.17%.

2026 Small Dogs and other Portfolios (current): Up 13.19% ($1,906 in profit) in just ten weeks. Plus COP, which we closed and banked at +47.40%. Meanwhile, the S&P 500 is down 3.4% over the same period. That's a 16.6 percentage point advantage. Four of five current positions are profitable in the Small Dogs. The one losing position is cushioned by premium collected and time remaining.

The pattern repeats. Not every position wins. VZ lost in 2025. One position is lagging now. But the winners more than compensate. JNJ returned +93%. Current VZ is up +57%. AAPL returned +70%. The basket approach provides stability. The process repeats across time periods. The math works. The process works. The structure works.

Wealth Without Shares members see every LEAPS entry, every short call, every roll decision, and every management alert across all five portfolios in real time.

👉 [See the full trade log and join at Wealth Without Shares →]

📰 Weekly In-Depth Articles

🗓️ Tuesday, March 10th: Investing Without Probabilities: Are We Ignoring the Odds?

🗓️ Thursday, March 12th: LEAPS vs. Stock: Why "Efficient Stock" Actually Works

🗓️ The Research Desk

📈 LEAPS for Part-Time Traders: A Low-Maintenance Framework (Updated with new images and visuals)

Not everyone can watch the screen all day. This practical framework is built for traders with limited screen time: structured entries, a simple review cadence, and realistic expectations for what LEAPS can deliver when you check in once or twice a week, not once an hour.

👉 Read the full framework: LEAPS for Part-Time Traders

📈 When to Roll the LEAPS Itself (Updated with new images and visuals)

Your LEAPS loses delta efficiency over time. Extrinsic value collapses. Elasticity fades. This guide covers the mechanical signals that tell you it's time to reset your long call position: when delta drift, extrinsic collapse, and leverage erosion cross the thresholds that matter.

👉 Read the full guide: When to Roll the LEAPS

🎓 Options 101: Call Options Explained: When to Buy vs. When to Sell

A call option is the most fundamental bullish contract in options trading. But here's what most beginners miss: buying a call and selling a call are two completely different strategies with different risk profiles, different probability characteristics, and entirely different roles in a portfolio.

This week, I published a complete guide covering both sides of the call option. You'll learn why buying calls works best with strong directional conviction and low IV (where leverage is cheap), why selling covered calls is built for neutral-to-bullish environments with elevated IV (where time decay works for you instead of against you), a side-by-side comparison of probability profiles (30-40% POP for buyers vs. 70-85% for sellers), and my 80/20 framework: roughly 80% of my call activity is selling, 20% is buying as part of defined-risk structures like PMCCs. Same contract, two completely different strategies. Knowing when each makes sense is what separates consistent traders from expensive lessons.

👉 Read the full breakdown: Call Options Explained: When to Buy vs. When to Sell

🧠 Mental Capital: Iron Condor Strategy Explained: Defined-Risk Neutral Trading

Most options strategies require you to pick a direction. The iron condor flips that entirely. Instead of predicting where a stock is going, you define a range where you believe the stock won't go, collect premium for that belief, and profit when the stock stays inside the boundaries.

This week, I published a complete guide to the iron condor. You'll learn how the four-leg structure works (bull put spread below + bear call spread above), when to use them (neutral outlook, IVR above 30, 30-45 DTE, high liquidity), the strike selection framework (0.15-0.20 delta on both sides, credit-to-width ratio above 1/3), and the four management decisions every iron condor requires: take profit at 50%, roll the untested side, close the losing side, or exit before max loss. After 24+ years of selling premium, I can tell you that stocks spend far more time chopping sideways than making dramatic moves. The iron condor lets you monetize that reality.

👉 Read the full article: Iron Condor Strategy Explained: Defined-Risk Neutral Trading

Educational Corner: Credit Spread Strike Selection: A Probability-Based Approach

Strike selection is where credit spreads are won or lost. Not at management. Not at exit. At entry. The strikes you choose determine your probability of profit, return on capital, breakeven distance, and risk-reward ratio before a single day passes.

This week, I published the complete framework I use after thousands of credit spread trades. You'll learn why delta is your primary selection tool (not premium), the 0.15-0.25 delta sweet spot and what happens when you go outside it, the five-step process from delta selection through IV confirmation, how IV environment shifts your target delta (low IV: skip entirely; moderate: 0.15-0.20; elevated: 0.12-0.15; extreme: caution), and why breakeven distance of at least 4-5% is the most underappreciated metric in spread selection.

Implied Perspective members see this framework applied in real time every week with specific tickers, strikes, and management rules.

👉 Read the full breakdown: Credit Spread Strike Selection: A Probability-Based Approach

👉 [See the framework in action with real trades at The Implied Perspective →]

📊 The Implied Truth

The Weekly ETF Volatility and Trend Intelligence Report

ETF Watchlist for March 15, 2026

Where the Probabilities Favor Selling (IV Rank > 50%)

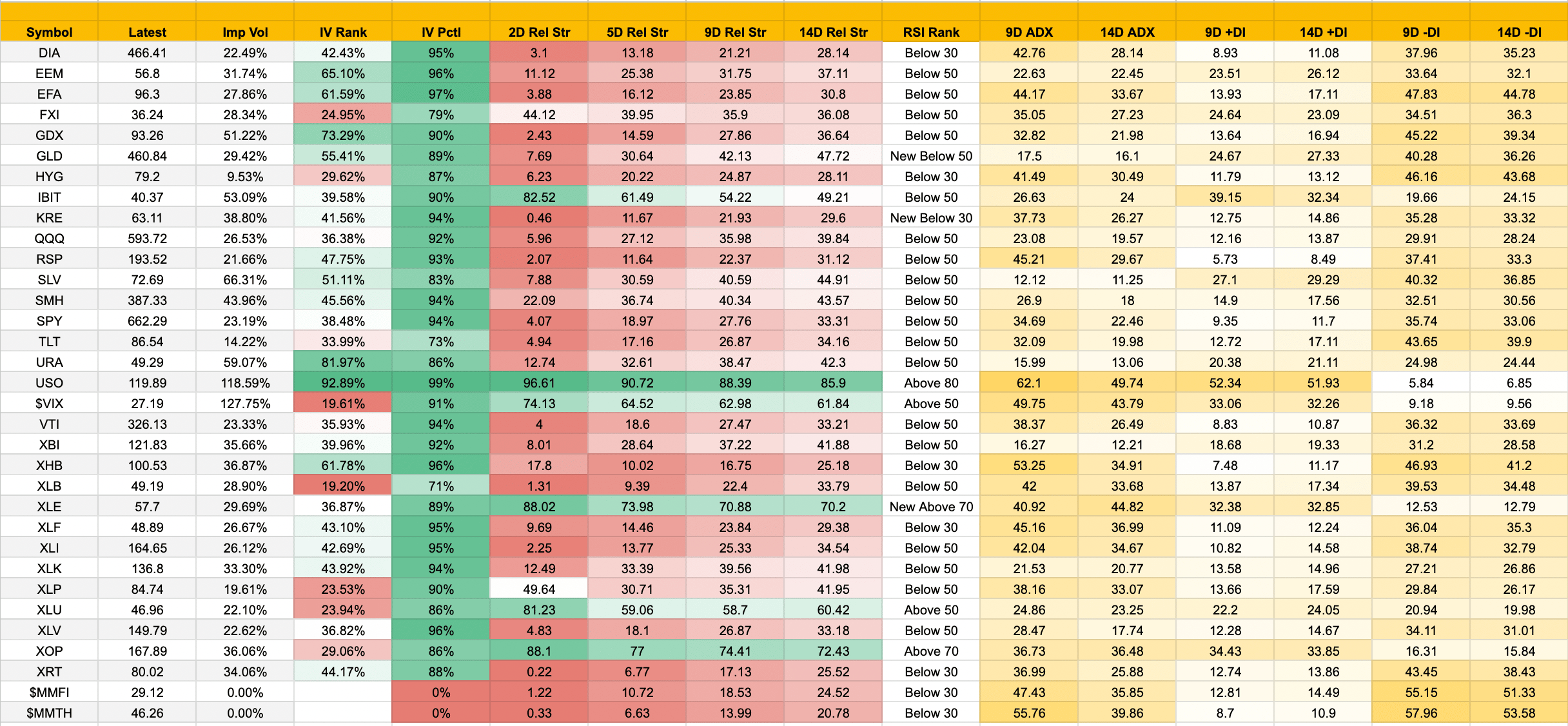

Eight ETFs sit above 50% IVR this week, down from nine last week as SMH cooled from 56.69% to 45.56%. The commodity and geopolitical cluster still dominates.

USO leads at 92.89% IVR, 99% IVP. Oil volatility is persistent, not a one-day event. ADX at 49.74 with +DI at 51.93 crushing -DI at 6.85. This is one of the strongest directional readings in the entire watchlist.

URA at 81.97% IVR, 86% IVP. Uranium continues to print rich premiums. ADX is low at 13.06, which means range-bound conditions with expensive options. Premium sellers welcome.

EEM at 65.10% IVR, 96% IVP. Emerging markets remain firmly in the sell zone with -DI dominant at 32.10 vs +DI at 26.12. Credit spreads with bearish bias work here.

The remaining five ETFs above 50% IVR, their directional readings, and the specific framework for how to trade each one are in this week's Implied Perspective.

👉 [Get the full 8-ETF breakdown and 100+ equity watchlist at theoptionpremium.com→]

Respect the Trend

Energy is still the only sector where +DI dominates with rising relative strength. XLE sits at ADX 44.82 (institutional conviction), RS 70.20, with a "New Above 70" RSI reading. USO and XOP follow the same pattern. PMCCs with conservative deltas (10 delta or lower) remain the approach here.

XHB flipped into a monster downtrend. ADX surged to 34.91 with -DI at 41.20 crushing +DI at 11.17. This is the strongest bearish trend on the board. Despite 61.78% IVR and 96% IVP, selling puts here means fighting the trend. Bear call spreads or simply avoid.

XLU remains the lone defensive trend with +DI (24.05) above -DI (19.98) and RS at 60.42, but IVR is only 23.94%. The math says don't sell premium. LEAPS and debit spreads only.

The Vol Shift Continued

Last week the VIX jumped 50%. This week it cooled slightly to 27.19, but the repricing held. Index IVR settled into the 36-42% range: SPY at 38.48%, QQQ at 36.38%, DIA at 42.43%. All three have IV Percentile above 92%. The math is improving. If IVR pushes above 40-45%, the expected value equation tips firmly in favor of selling. DIA is closest to that threshold.

Only four ETFs remain cheap: XLP (23.53%), XLU (23.94%), XLB (19.20%), and FXI (24.95%). Don't sell premium here.

TLT is worth watching. IVR jumped from 17.70% to 33.99% as the 10-year yield compressed further on flight-to-safety flows. Not rich enough to sell yet, but moving in the right direction.

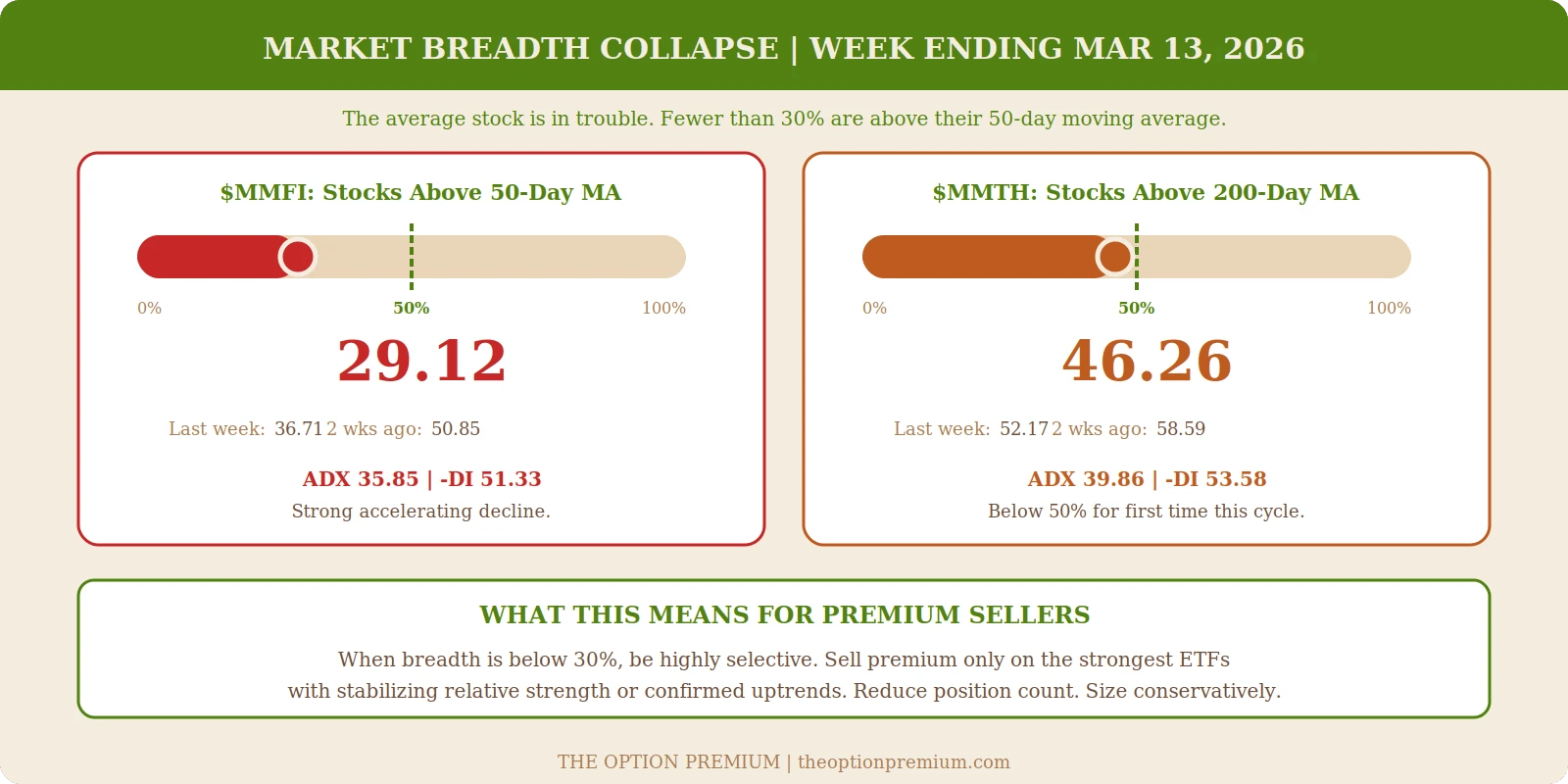

Breadth Collapsed Further

$MMFI crashed to 29.12. Fewer than 30% of stocks are above their 50-day moving average. This is a level that historically marks oversold territory for the broad market. $MMTH dropped below 50 to 46.26. Both indicators show ADX above 35 with -DI above 48. This is a strong, accelerating decline in market internals.

When breadth is this weak, be highly selective. Sell premium only on the strongest-looking ETFs: those with the highest relative strength readings or signs of stabilization. Reduce overall position count and keep position sizing conservative.

The full Notable Moves section, this week's complete framework, and the 100+ equity volatility breakdown are available in The Implied Perspective.

👉 [Read this week's Implied Perspective at theoptionpremium.com →]

Field | What It Tells You |

|---|---|

IV Rank (IVR) | Where today's IV sits vs. 52-week range. >35% favors premium selling |

IV Percentile (IVP) | % of trading days with lower IV. Confirms persistent elevation |

Relative Strength (RS) | Momentum vs. broader market. Above 65 = leader |

ADX | Trend strength. >25 established, >35 strong, >40 institutional |

The Bottom Line

The decline broadened. $MMFI fell below 30% for the first time. $MMTH broke below 50. The average stock is now below its 200-day moving average. Meanwhile, the VIX sits at 27.19 and eleven ETFs have IV Percentile above 94%. Fear is widespread. Premiums are rich. And sector selection has never mattered more.

For probability-based traders, this is the environment the framework was built for. When breadth collapses, you narrow your focus. When IV is elevated, you sell premium where the math confirms it. When trends are strong, you ride them with defined risk instead of fighting them.

FOMC Wednesday and NVIDIA's GTC this week will provide the next catalysts. Size accordingly. Follow the math. And make sure your capital is still here when the dust settles.

🎓 Coming Soon: PMCC Mastery

PMCC Mastery covers everything: LEAPS selection, short call management, the roll decisions that separate sustainable income from frustrating losses. This isn't a strategy overview. It's a complete implementation system with clear rules, real examples, and the decision frameworks I use every week in our live portfolios.

You won't be left alone with a PDF. Every student joins the dedicated PMCC community forum for questions, real-time discussion, and accountability to a process that works.

Following PMCC Mastery:

Credit Spreads: The Probability Player's Edge

The Complete Wheel Strategy Course

Want early access? Reply to this email with "PMCC" in the subject line to [email protected]. I'll make sure you're first in line.

Note: Anyone on the $1,495 annual all-access plan receives every course I release at no extra cost, including PMCC Mastery and everything that follows.

A Quick Note

I can't thank everyone enough for the continued support. The emails and testimonials over the past few months have been overwhelming, and I mean that sincerely. Every message I receive reminds me why I started this.

I want you to know something: I will continue to create a marketing-free experience. We are all tired of the nonstop, excessive marketing emails that this industry brings. Not from real traders, but from bloated direct marketing firms that staff 25 employees with 23 of them centered around marketing. That's not what this is. That's not what this will ever be.

I'm one person. I trade. I teach. I write. That's it.

For all of you who open this email every Sunday evening, who forward it to a friend, who trust me with your time and your education: thank you, thank you, thank you.

🔗 Let's Stay Connected

Have questions, feedback, or just want to say hello? I'd love to hear from you. 📩 Email me anytime at [email protected]

📺 Subscribe on YouTube so you'll be notified when the first videos are released.

👥 Join the private Facebook group or connect with me on X. Send me your topic requests, whether for the newsletter, YouTube, or webinars. Seriously, send them. 🙂

Thanks again for reading. I hope you found today's insights valuable and worth your time.

Trade Smart. Trade Thoughtfully.

Andy Crowder Founder | Editor-in-Chief | Chief Options Strategist | The Option Premium

The Option Premium is published for educational purposes only and does not constitute personalized investment advice. Options involve risk and are not suitable for all investors. Past performance does not guarantee future results. Always confirm details and manage risk prudently.

Reply