- The Option Premium

- Posts

- LEAPS vs. Stock: Why "Efficient Stock" Actually Works

LEAPS vs. Stock: Why "Efficient Stock" Actually Works

LEAPS vs. stock: how deep ITM calls (12 to 24 months) deliver stock-like exposure with less capital, delta targets, extrinsic tests, and income via short calls.

LEAPS vs. Stock: Why "Efficient Stock" Actually Works

The Capital Question Nobody Asks

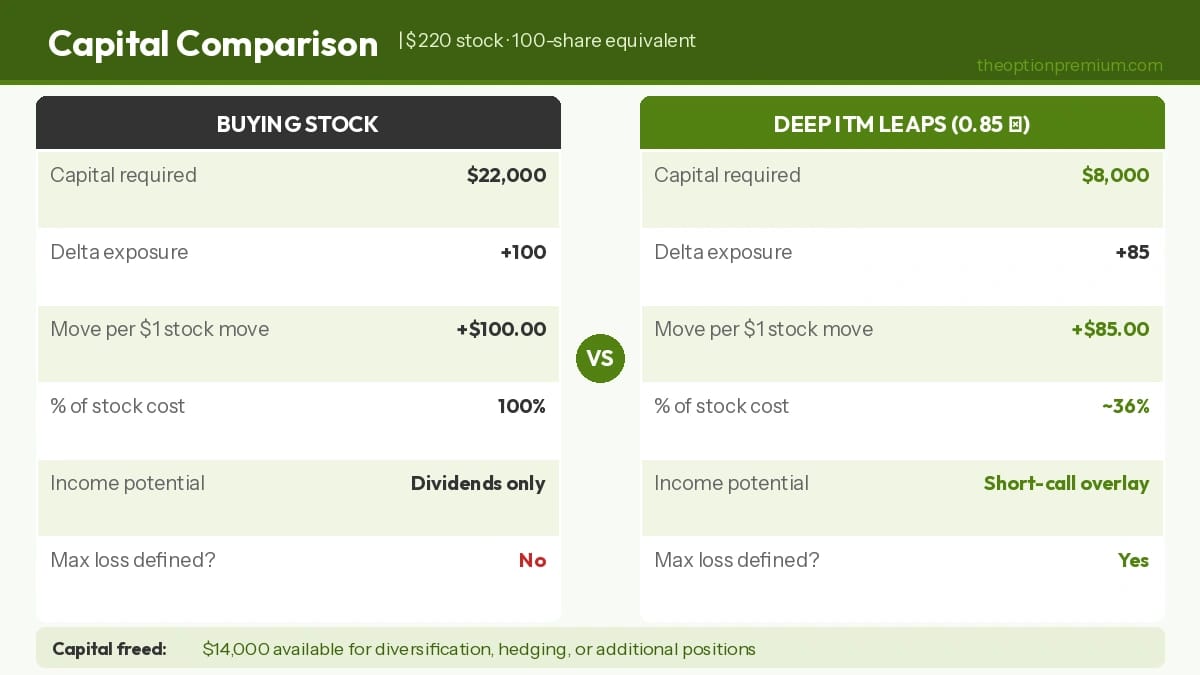

Here's the problem with buying shares: they work perfectly, but they're capital-hungry. One hundred shares of a $220 stock costs $22,000. That's real money sitting in one position, earning whatever the stock delivers, and nothing more.

LEAPS, specifically deep in-the-money calls with 12 to 24 months until expiration, let you capture 70% to 95% of the stock's move using a fraction of that capital. You're not gambling. You're not speculating. You're getting stock-like exposure with less cash tied up.

The trade-off? You give up dividends. You accept some volatility sensitivity. And you need to actually understand what you're buying instead of just clicking "buy 100 shares."

But if you do it right, deep in-the-money, modest time value, delta around 0.75 to 0.90, you get something shares can't give you: capital flexibility and the ability to layer income on top through systematic short-call selling.

The Real Numbers (Not Hypotheticals)

Stock trading at $220. You want exposure.

The stock approach:

Buy 100 shares = $22,000 cash

Portfolio delta = +100 (moves $100 for every $1 the stock moves)

Simple. Clean. Capital-intensive.

The LEAPS approach:

Buy an 18 to 24-month call with a $150 strike, costs about $80

Total cost = $8,000 per contract (controls 100 shares)

Delta ≈ +0.85 → Portfolio delta ≈ +85

Captures about 85% of the stock's move

What you just saved: $14,000 in capital.

What that $14,000 buys you:

The ability to add a second position

A cash buffer for market turbulence

Room to run a short-call income program on top

When the stock moves $1, shares give you $100 in P&L. The LEAPS gives you $85 (plus or minus small adjustments from the Greeks). You're getting most of the move with about 36% of the capital.

That's not leverage in the dangerous sense. That's efficiency.

The stock costs $22,000. The deep ITM LEAPS costs $8,000. Both give you exposure to the same 100-share move. Only one of them also gives you $14,000 back to deploy elsewhere.

Delta Targets: Where the Magic Happens

Think of delta as your exposure dial. For LEAPS that behave like "efficient stock," these are the practical ranges:

Delta around 0.70 ("elastic core")

Pros: Cheaper entry. More elasticity if the stock moves. Less sensitivity to volatility drops.

Cons: You give up more upside versus shares. Can drift too shallow if you're not disciplined about rolling.

Best for: Early trend entries, high-volatility names, or when implied volatility is rich and you want to minimize time value.

Delta around 0.80 ("balanced engine")

Pros: The classic Poor Man's Covered Call setup. Strong participation in the stock's moves with manageable theta and vega. This is the sweet spot for most traders.

Cons: Costs more than 0.70 delta. May require rolling up after big rallies to keep elasticity.

Best for: Steady compounders where you plan to sell calls frequently against the LEAPS.

Delta around 0.90 ("near-stock feel")

Pros: Closest to owning shares without paying full cash. Minimal slippage on upside moves.

Cons: Higher cost. Time value is very small (which is good), but volatility swings can still surprise you on mark-to-market.

Best for: Low-volatility blue chips, or when you want nearly full exposure with capital relief.

Rule of thumb: Start around 0.80 delta when volatility is normal. In high-volatility environments, favor 0.70 to 0.80 to give yourself breathing room. In quiet markets, 0.85 to 0.90 can be efficient without overpaying for time.

0.70 for elastic entries in high-IV environments, 0.80 as the PMCC sweet spot, 0.90 when you want near-stock feel with capital relief. The right delta depends on volatility conditions, not preference.

The Extrinsic Value Test (Don't Skip This)

Your LEAPS should behave like stock, not like a speculation. Here's the quick check:

Extrinsic percentage = (Option Price − Intrinsic Value) ÷ Option Price

You want extrinsic value at 10% to 15% or less for a core position. The lower, the better.

If the time value is fat, say, 20% or more of the option's price, walk further in-the-money or add more time until the option is mostly intrinsic value.

Why this matters: Low extrinsic means less theta bleed and your profit-and-loss tracks the stock's actual movement (via delta), not the slow drain of time decay.

High extrinsic means you're making a volatility bet. That's fine for a trade. It's not fine for a core position.

Three Real Scenarios (What Actually Happens)

Assume a $220 stock. You can buy 100 shares or one deep in-the-money LEAPS with 0.85 delta. No dividends. No short calls yet.

Scenario A: Stock rallies to $250 (+$30 move)

Stock: +$3,000 profit

LEAPS: About +$2,550 profit (0.85 × $30 × 100 shares, minus small theta and vega effects)

What you captured: 85% of the move with 36% of the capital.

Scenario B: Stock drifts sideways (stays around $220)

Stock: Roughly flat (ignoring dividends)

LEAPS: Slight decay in the option's time value, muted if you went deep in-the-money. Mark-to-market wobbles with implied volatility changes.

The LEAPS won't be perfectly flat like shares. If implied volatility drops, your mark can dip even though the stock hasn't moved. Deep in-the-money positioning keeps this wobble modest.

Scenario C: Stock drops to $200 (−$20 move)

Stock: -$2,000 loss

LEAPS: About -$1,700 loss (0.85 × $20 × 100 shares, offset by any short-call income if you're running a PMCC)

What happened: You lost less than stock in dollar terms, and you lost it using far less capital.

Rally, sideways, or drop: in two of three outcomes the LEAPS dollar result is comparable to shares. In all three, it uses 36% of the capital. That asymmetry is the whole point.

Where Short Calls Fit (The Income Layer)

Once your LEAPS is in place, you can systematically sell calls 30 to 45 days out at 10 to 20 delta. This accomplishes several things:

Reduces your LEAPS cost basis over time

Funds future rolls when you need to adjust the LEAPS

Creates a repeatable rhythm: sell, manage winners early, roll on schedule

Keep it conservative: One short call per LEAPS contract. This isn't about getting rich on one trade. It's about running an income engine month after month.

Size and manage this like a business, not a hero trade.

Rolling Rules (That Keep You Out of Trouble)

After a rally (LEAPS delta climbs to 0.92 or higher):

Roll the LEAPS up one or two strikes and out in time to restore delta back into your target range (0.75 to 0.85). This also resets the time value dynamic and keeps short-call premiums collectible.

If you don't do this, your LEAPS starts acting exactly like stock, which defeats the purpose, and short-call credits dry up.

After a slump:

Do not panic-sell your core position. Deep in-the-money positioning cushions downside. Let time work for you and keep selling prudent short calls. Revisit your thesis, not your nerves.

Calendar discipline:

Check your extrinsic percentage once a month. If time value creeps higher (maybe implied volatility jumped), you may be able to roll deeper in-the-money at similar cost and tame theta and vega effects.

Decision Tree (Use This Before Every Trade)

1. Define the job: Is this a core long position or a tactical swing trade?

Core long → LEAPS

Swing trade → Shares or short-dated options

2. Pick the time frame: 12 to 24 months

Sweet spot for controlled theta decay and manageable volatility sensitivity

3. Set your delta target: 0.75 to 0.90 based on volatility and your temperament

High IV environment → 0.70 to 0.80

Low IV environment → 0.85 to 0.90

4. Check extrinsic value: Should be 10% to 15% or less

Too high? Go deeper in-the-money or add time

5. Add income (optional): Sell 30 to 45-day calls at 10 to 20 delta

Manage early at 50% to 65% of max profit or when 14 to 21 days remain

6. Maintain:

Roll up and out when LEAPS delta exceeds 0.90

Keep selling calls on a schedule

Re-evaluate your thesis every quarter

The Risks (Straight Talk)

Volatility moves matter: LEAPS prices move with implied volatility changes. Deep in-the-money helps, but earnings announcements and market shocks can swing your marks short-term even if the stock doesn't move much.

Opportunity cost on explosions: If the stock rips higher fast, shares deliver +100 delta instantly. LEAPS will lag unless you're at 0.90 delta or higher.

No dividends: You won't receive them with calls. You can approximate the value over time by collecting call premium, but it's not the same.

Assignment risk on short calls: It's part of the game. Use modest deltas on your short calls, manage them early, and have a rolling playbook ready.

You must manage this: Shares sit there. LEAPS require attention. If you're not willing to check deltas monthly and roll when needed, stick with shares.

Quick Checklist (Before Every LEAPS Purchase)

☐ Time to expiration: 12 to 24 months

☐ Delta in target range: 0.75 to 0.90

☐ Extrinsic value: 10% to 15% or less

☐ Underlying has excellent liquidity (tight bid-ask, deep open interest)

☐ Your thesis horizon is at least 6 to 12 months

☐ Short-call plan ready: 30 to 45 days out, 10 to 20 delta, take winners early

Six boxes. Expiration, delta, extrinsic value, liquidity, thesis horizon, and a short-call plan. If one doesn't check out, the setup isn't ready.

Stock vs. LEAPS: The Side-by-Side

Capital (per 100 shares) | Delta | Dividend | Theta Impact | Vega Impact | Best For | |

|---|---|---|---|---|---|---|

Stock | $22,000 | +100 | Yes | None | None | Maximumsimplicity, full exposure |

LEAPS (deep ITM) | $7,000–$9,000 | +70 to +90 | No | Low (if deep ITM) | Moderate | Capital efficiency,controlled exposure |

LEAPS + Short Calls | Same as LEAPS-premium of short calls | +60 to +90 (net) | No | Net neutral to slightly positive | Moderate | Income plus durable core (PMCC) |

(Numbers are illustrative; vary by stock and volatility.)

A Simple Example (Mechanics Only, Not a Recommendation)

Stock at $220.

Buy an 18-month call with a $150 strike for $80. Delta around 0.85. Extrinsic value about 8% of the option's price.

Add a short-call overlay: Sell a 35-day call at 10 delta for $1.30. Manage at 50% to 65% of max profit.

What happens in different scenarios:

Sideways to small upside: The short call decays. You keep $0.65 to $1.00 repeatedly over time.

Big upside: You roll the short call to a higher strike. LEAPS gains outpace any call adjustments.

Downside: LEAPS loses less in dollars than stock would. Call income cushions the loss.

The long-run engine is the consistent call cycle, not the one-off home run. That's the whole point.

When Stock Is Still Better

Dividends are central to your thesis. High-yield stocks where dividends drive a big portion of total return, just own the shares.

You want zero complexity. No rolling. No Greeks. No delta monitoring. Shares are simple.

Tax considerations favor shares in your specific account type. Rules vary by situation. Talk to a tax professional.

How to Actually Use This in a Portfolio

Core exposure: Use LEAPS to set your long market exposure at the delta level you're comfortable with. You're controlling your risk profile, not just buying what "feels" right.

Income sleeve: Layer short calls to steadily reduce your LEAPS basis and fund future rolls.

Position sizing: Keep it modest. Even efficient stock can hurt if you oversize.

Review cadence: Weekly for short-call management. Monthly for LEAPS delta and time value. Quarterly for thesis review.

Common Questions

Q: What if implied volatility collapses after I buy the LEAPS?

A: Deep in-the-money helps. You may see a mark-to-market dip, but most of your value is intrinsic. Keep your time horizon. Short calls provide ongoing offset.

Q: How often should I roll the LEAPS itself?

A: Only when delta exceeds 0.90 or time remaining drops under 9 to 12 months and you want to keep the structure running. Roll up and out in one transaction when possible.

Q: Is 0.70 delta "worse" than 0.90 delta?

A: Not worse, different. 0.70 is more elastic and cheaper. 0.90 tracks closer to shares. Pick the range that fits volatility and your comfort level.

Q: How many short calls per LEAPS?

A: One-for-one. Keep it clean. Don't get fancy.

The Bottom Line

Shares are the blunt instrument. Maximum simplicity. Maximum capital requirement.

LEAPS are the scalpel. Targeted delta. Lower cash outlay. A structure built for disciplined income overlays.

If you insist on simple, stick with shares. If you want a capital-efficient core position you can precisely tune, and you're willing to actually manage it, deep in-the-money LEAPS with 12 to 24 months, low time value, and a sensible delta target are hard to beat.

Most traders won't do this because it requires discipline, monthly attention, and the willingness to follow rules instead of feelings. But the ones who do it right, who keep extrinsic low, deltas honest, and call cycles systematic, build steady returns while using far less capital than the crowd.

And in the long run, efficiency compounds just as surely as returns do.

Probabilities over predictions,

Andy Crowder

🎯 Ready to Elevate Your Options Trading?

Subscribe to The Option Premium, a free weekly newsletter delivering:

✅ Actionable strategies.

✅ Step-by-step trade breakdowns.

✅ Market insights for all conditions (bullish, bearish, or neutral).

📩 Get smarter, more confident trading insights delivered to your inbox every week.

📺 Follow Me on YouTube:

🎥 Explore in-depth tutorials, trade setups, and exclusive content to sharpen your skills.

📘 Join the conversation on Facebook.

Disclaimer: This is educational content only. Not investment, tax, or legal advice. Options involve risk and aren't suitable for all investors. Examples are illustrative. Real results will vary. Talk to professionals before you risk real money.

Reply