- The Option Premium

- Posts

- Call Options Explained: When to Buy vs When to Sell

Call Options Explained: When to Buy vs When to Sell

Learn both sides of call options: when buying calls makes sense for directional leverage and when selling covered calls generates income. Step-by-step examples, the 80/20 approach, and common mistakes.

Andrew Crowder

March 15, 2026

Call Options Explained: When to Buy vs When to Sell

A call option is the most fundamental bullish contract in options trading. It gives the buyer the right to purchase 100 shares of a stock at a specific price before a specific date. But here's what most beginners don't realize: buying a call and selling a call are two completely different strategies with different risk profiles, different probability characteristics, and different roles in a portfolio.

Understanding both sides of the call option isn't optional. It's essential. Whether you're buying calls for directional upside or selling them to generate income against shares you own, knowing when each approach makes sense will determine whether calls become a consistent tool in your trading or an expensive lesson.

What Is a Call Option?

A call option is a contract between a buyer and a seller. The buyer pays a premium for the right to buy 100 shares at the strike price before the expiration date. The seller collects that premium and takes on the obligation to deliver 100 shares at the strike price if the buyer exercises.

Every call option has four components. The underlying stock is the stock the contract is based on. The strike price is the price at which the buyer can purchase shares. The expiration date is when the contract ceases to exist. And the premium is the price of the contract itself, determined by intrinsic value, time value, and implied volatility.

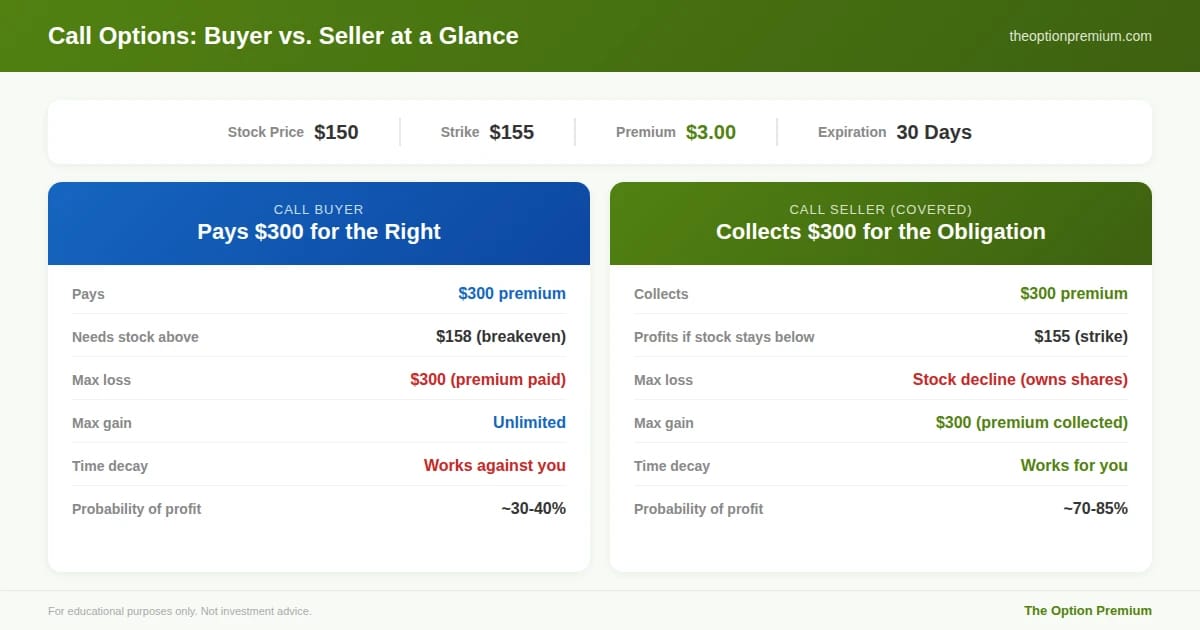

A quick example to ground this. A stock trades at $150. You're looking at a $155 call expiring in 30 days, priced at $3.00. The buyer pays $300 for the right to buy 100 shares at $155 anytime before expiration. The seller collects $300 and agrees to sell 100 shares at $155 if called upon.

If the stock rises to $165, that $155 call is now worth at least $10 in intrinsic value. The buyer profits. If the stock stays at $150 or drops, the call expires worthless. The buyer loses the $300 premium. The seller keeps it.

Same contract. Two very different outcomes depending on which side you're on.

Same contract, two completely different strategies. The buyer pays $300 for the right to leveraged upside (30-40% probability of profit). The seller collects $300 for taking on the obligation (70-85% probability of profit). Time decay works against the buyer every day and for the seller every day.

Buying Calls: The Bullish Bet

When you buy a call, you're making a directional bet that the stock will rise above the strike price plus the premium paid before expiration. Your risk is limited to the premium you paid. Your upside is theoretically unlimited.

How buying calls works in practice. You buy the $155 call for $3.00. Your total cost is $300. Your breakeven at expiration is $158 (the $155 strike plus $3.00 premium). Below $158, you lose money. Above $158, every dollar the stock rises adds $100 to your profit. At $165, your profit is $700. At $170, it's $1,200.

The appeal is leverage. Instead of buying 100 shares at $150 ($15,000), you control the same 100 shares for $300. That's 50:1 leverage. If the stock rises 10% to $165, your call option returns over 230%. The same move in stock returns just 10%.

But leverage cuts both ways. If the stock rises only 3% to $154.50, you still lose your entire $300 because the stock didn't clear your breakeven. In fact, you can be right about the direction and still lose money if the move isn't large enough or fast enough. This is the core tension of buying options: time and magnitude both have to cooperate.

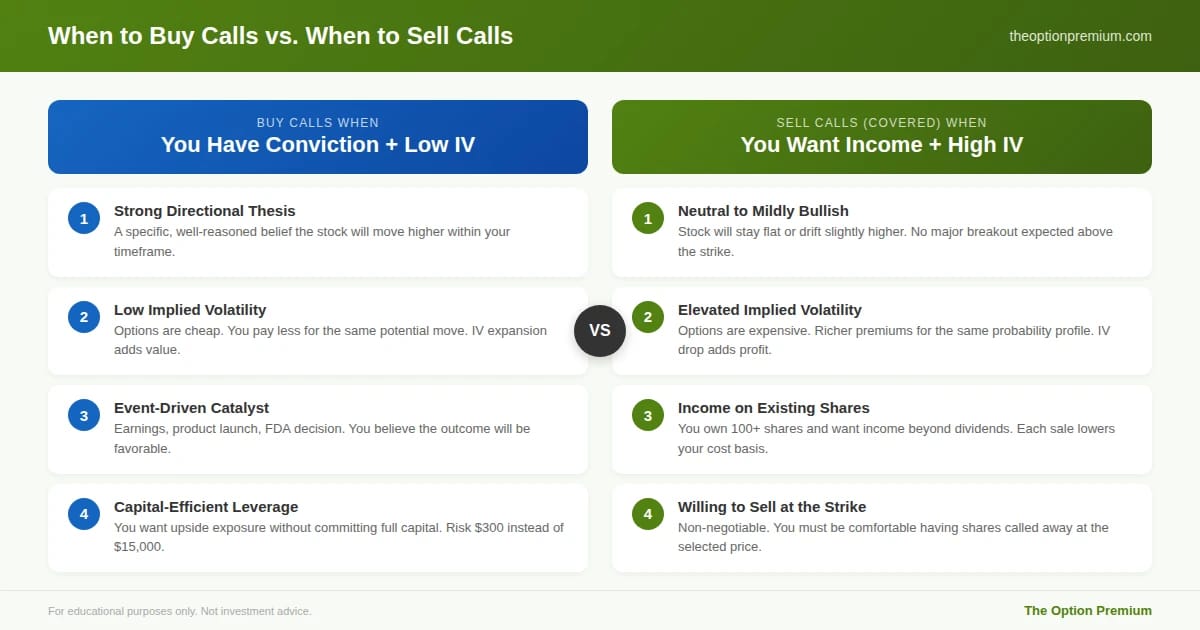

When buying calls makes sense:

Strong directional conviction. You have a specific, well-reasoned thesis that a stock will move higher within a defined timeframe. Vague bullishness isn't enough. You need the stock to move enough to overcome your premium cost.

Low implied volatility environment. When IV is low, options are relatively cheap. Buying calls in a low-IV environment means you're paying less for the same potential move. If IV subsequently rises, your call gains value from both the stock move and the volatility expansion.

Defined-risk alternative to stock. You want upside exposure without committing full capital to buying shares. Buying a call risks $300 instead of $15,000. For a conviction trade where you want to limit your dollar risk, calls are capital-efficient.

Event-driven catalysts. Earnings, product launches, FDA decisions, or other binary events where you believe the outcome will be favorable. The leverage of a call amplifies the payoff if you're right.

Portfolio hedging with calls. If you have a short stock position or are heavily positioned for a downturn, buying calls provides upside protection if you're wrong about the direction.

Selling Calls: The Income Generator

Selling a call means collecting premium in exchange for the obligation to deliver shares at the strike price. When you sell calls against shares you already own, this is a covered call, one of the most widely used income strategies in options trading. It's also the second phase of the Wheel Strategy after being assigned on a cash-secured put.

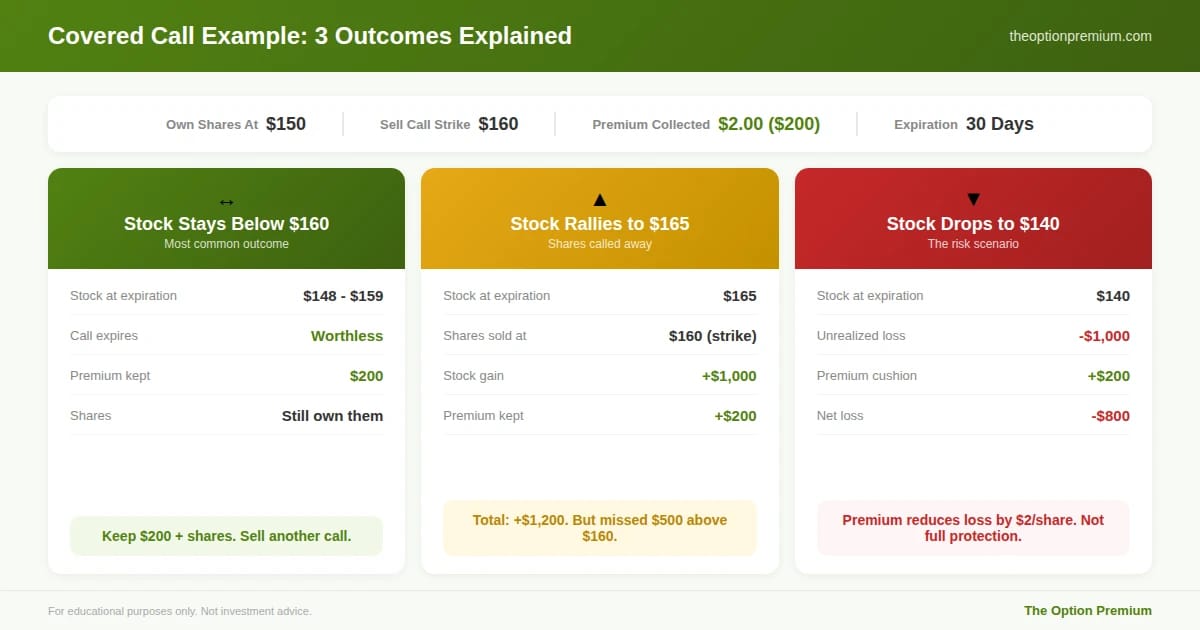

How selling covered calls works in practice. You own 100 shares of a stock at $150. You sell the $160 call expiring in 30 days for $2.00. You collect $200 immediately.

Three outcomes unfold. If the stock stays below $160, the call expires worthless and you keep the $200 plus your shares. If the stock rises to $165, your shares are called away at $160 and you keep the $200 premium, for a total gain of $1,200 ($10 stock appreciation plus $2 premium) but you miss the move from $160 to $165. If the stock drops to $140, you still own shares at a loss, but the $200 premium reduces your effective loss by $2 per share.

Three outcomes of selling a $160 covered call on shares owned at $150 for $2.00 premium. Stock stays flat: keep $200 plus shares (most common). Stock rallies past $160: shares called away, total gain $1,200 but miss upside above $160. Stock drops: premium cushion reduces loss by $2 per share but doesn't provide full protection.

The trade-off is clear. You cap your upside at the strike price in exchange for immediate income. Every covered call involves this exchange: premium today for potential upside tomorrow.

When selling calls makes sense:

Neutral to mildly bullish outlook. You think the stock will stay relatively flat or drift slightly higher. You don't expect a major breakout above your strike. The premium you collect is your primary profit driver.

Income generation on existing positions. You own shares and want to generate income beyond dividends. Selling calls against your position creates a consistent income stream. Many Wheel Strategy practitioners sell covered calls as a routine part of managing assigned positions.

Reducing cost basis. Each covered call you sell lowers your effective cost basis on the shares. If you were assigned shares at $150 through a cash-secured put and collect $2 per month in covered call premium, your effective cost basis drops to $148 after one month, $146 after two, and so on.

Elevated implied volatility. When IV is high, call premiums are richer. The same 0.20 delta call that pays $1.00 in a low-IV environment might pay $2.50 when IV is elevated. Selling into elevated IV gives you more income for the same probability profile.

Willing to sell at the strike. This is non-negotiable. If you sell a $160 call, you must be comfortable having your shares called away at $160. If you'd regret selling at that price, either choose a higher strike or don't sell the call.

Buy calls when you have strong directional conviction, IV is low, a specific catalyst exists, or you want capital-efficient leverage. Sell covered calls when you're neutral to mildly bullish, IV is elevated, you want income on existing shares, and you'd be comfortable having shares called away at the strike.

The Side-by-Side Comparison

The differences between buying and selling calls come down to what you're paying for versus what you're being paid for.

Who pays and who collects. The buyer pays premium. The seller collects it. This single difference drives everything else. The buyer needs the stock to move enough to overcome their cost. The seller profits when it doesn't.

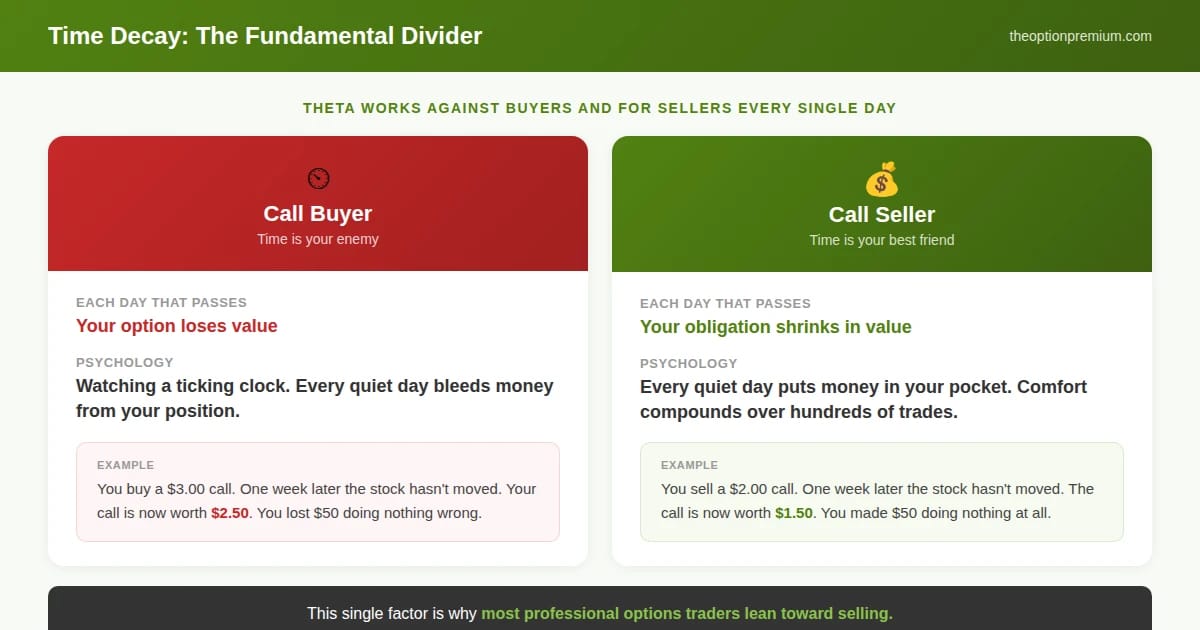

Time decay. Theta works against the buyer every single day. An option that costs $3.00 today might be worth $2.50 in a week even if the stock hasn't moved. For the seller, that same daily decay puts money in their pocket. Time is the buyer's enemy and the seller's best friend.

Probability profile. Buying an OTM call has a relatively low probability of profit, often 30-40%. Selling an OTM covered call has a high probability of collecting the premium, typically 70-85% depending on the delta selected. The buyer bets on the unlikely but large outcome. The seller bets on the likely but limited outcome.

Risk and reward. The buyer's risk is the premium paid. The reward is theoretically unlimited. The seller's reward is the premium collected. The risk on a covered call is the stock declining (you still own the shares) plus the opportunity cost of capping your upside.

The fundamental divider between buying and selling calls. A quiet week costs the buyer $50 as theta erodes the option's value. The same quiet week earns the seller $50 as their obligation shrinks. Over hundreds of trades, this compounding comfort vs. compounding stress affects decision-making and shows up in results.

Capital requirement. Buying a call requires the premium cost, a relatively small amount. Selling a covered call requires owning 100 shares, which means significant capital commitment. This is why the poor man's covered call exists, replacing the 100-share requirement with a deep ITM LEAPS option.

The Practitioner Edge: My 80/20 Approach to Calls

After two decades of trading, I've settled into a framework that uses both sides of the call option, but not equally.

Roughly 80% of my call activity is selling. Covered calls against existing positions, call spreads as part of iron condors, and short calls as the income leg of PMCCs. The math favors the seller over time. Implied volatility overestimates actual moves 80-85% of the time, which means options are systematically overpriced. Selling captures that edge.

The other 20% is buying. Deep ITM LEAPS calls as stock replacements in PMCC structures, and long calls as the protective wings in credit spreads. I'm rarely buying OTM calls as standalone directional bets. When I do, it's with a very specific thesis, a short timeframe, and money I've sized as risk capital, not portfolio capital.

The mental capital factor matters here. Buying calls creates a psychological environment of watching a ticking clock. Every day the stock doesn't move enough, your position bleeds value. Selling calls creates the opposite: every quiet day puts money in your pocket. Over hundreds of trades, the compounding stress of buying versus the compounding comfort of selling affects your decision-making in ways that show up in your results.

Common Mistakes With Call Options

Buying calls on hype. A stock is running, everyone is talking about it, and you buy calls at the top. By the time excitement reaches the mainstream, IV is elevated (making calls expensive) and the easy move has already happened. You're paying maximum premium for minimum remaining upside.

Ignoring time decay when buying. A $3.00 call expiring in 7 days needs the stock to move fast. Every day that passes without a move is money lost. If you're buying calls, give yourself enough time, at least 45-60 DTE, to be right without the clock running out.

Selling calls too close to the money. Choosing a $152 call on a $150 stock generates more premium but creates a high probability of having shares called away. For covered calls, use delta to select strikes, typically 0.15-0.30, depending on how much upside you're willing to cap.

Selling calls on stocks you don't own. Selling naked calls (without owning the underlying shares) has theoretically unlimited risk. The stock can rise indefinitely, and you're on the hook. Unless you're an experienced trader using defined-risk spreads, stick to covered calls where you own the shares.

Not having an exit plan for either side. Buying a call? Know your profit target and stop-loss before entry. Selling a covered call? Know when you'll close early (50-75% of max profit) and what you'll do if the stock rallies past your strike.

Risk Reality Check

Buying calls: you can lose 100% of your premium. In fact, most OTM calls expire worthless. The data is clear. If you're buying calls consistently without a disciplined approach to strike selection, timeframe, and position sizing, you will lose money over time.

Selling covered calls: your shares can be called away during a rally, causing you to miss upside. This isn't technically a "loss," but it feels like one. The real risk is the stock declining while you hold it. The covered call premium provides a small cushion, not full protection.

The responsible approach to both: size positions so that losing on any single trade doesn't materially impact your account. Buying calls? Risk no more than 1-2% of your account per trade. Selling covered calls? Ensure you're comfortable owning the shares regardless of short-term price action.

Key Takeaways

A call option gives the buyer the right to buy 100 shares at the strike price. Buyers pay premium for leveraged upside. Sellers collect premium for taking on the obligation. Same contract, two completely different strategies.

Buy calls when you have strong directional conviction, IV is low, you want defined-risk leverage, or you're trading a specific catalyst. Give yourself at least 45-60 DTE and size as risk capital.

Sell calls (covered) when you're neutral to mildly bullish, want income on existing shares, IV is elevated, and you'd be comfortable having shares called away at the strike. Use delta (0.15-0.30) for strike selection, not round numbers.

Time decay is the fundamental divider. It works against buyers every day and for sellers every day. This single factor is why most professional options traders lean toward selling.

Both sides have a place. The 80/20 approach (80% selling, 20% buying as part of defined-risk structures) captures the seller's probability edge while using call buying for capital-efficient stock replacement and portfolio protection.

Calls aren't inherently bullish or bearish, risky or safe. It depends entirely on which side of the contract you're on and whether you've matched the strategy to the situation.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply