- The Option Premium

- Posts

- Scaling Up in a Small Account: How to Grow a Sub-$10K Options Portfolio Without Blowing It Up

Scaling Up in a Small Account: How to Grow a Sub-$10K Options Portfolio Without Blowing It Up

More contracts first. Diversification second. Wider spreads third. The 5-phase roadmap from $5K to $30K+ with specific thresholds for adding complexity, plus the compounding math that makes patience the real scaling engine.

Andrew Crowder

April 25, 2026

Scaling Up in a Small Account: How to Grow a Sub-$10K Options Portfolio Without Blowing It Up

There's a question that every premium seller with a small account eventually asks. The account is working. The process is sound. The win rate is in the 75-80% range. The positions are profitable more often than not. But the dollar amounts feel small. A $0.85 credit on a $2-wide spread generates $85 per contract. After commissions and the occasional loss, the monthly income might be $200 to $400 on an $8,000 account. That's real money, and the percentage return is excellent, but it doesn't feel like it's moving the needle fast enough.

And so the temptation arrives. Should I trade more contracts? Should I switch to wider, more expensive strategies that collect bigger credits? Should I start selling naked puts instead of spreads? Should I move to higher-priced underlyings where the premiums are richer?

Every one of those questions is reasonable. And every one of them can destroy a small account if answered wrong. The challenge isn't knowing what to scale. It's knowing the order in which to scale, and understanding which scaling decisions increase your income proportionally to your risk versus which ones increase your risk faster than your income.

This article walks through the framework I'd use to scale a sub-$10,000 options account. The principles are the same ones I've applied over 24 years of professional trading. The application is specific to the constraints and opportunities that small accounts face.

The Math That Governs Everything in a Small Account

Before we talk about scaling, we need to confront the math that makes small accounts fundamentally different from large ones.

On a $10,000 account, a 2% position sizing rule means your maximum loss per trade is $200. That's one contract of a $2-wide credit spread. If you're collecting one-third of the spread width ($0.65 credit on a $2 spread), your max profit per trade is $65. Your max loss is $135 ($200 minus the $65 credit).

Those are small numbers. But the percentages are identical to what a $500,000 account produces at the same position sizing. You're generating the same return on capital. The only difference is the denominator. This matters because the temptation in a small account is always to make the denominator feel bigger by increasing risk. And the moment you do that, you've changed the fundamental risk profile that was making the account grow in the first place.

A $10,000 account that compounds at 2-3% per month (which is achievable with disciplined premium selling in elevated IV environments) grows to approximately $12,700 to $14,300 in one year. That's a 27-43% annual return. In two years, it's $16,000 to $20,400. In three years, it's $20,300 to $29,200. The compounding is doing the work. But it requires patience, and patience is the resource that small account traders have the least of.

Every scaling decision should be evaluated against this baseline: does this change increase my expected compounding rate, or does it increase my risk of a drawdown that resets the compounding clock?

The First Scaling Move: More Contracts on the Same Structure

The safest way to scale a small account is to increase the number of contracts on the same credit spread structure you're already trading successfully.

If you've been trading one contract of a $2-wide bull put spread on SPY, and the account has grown from $8,000 to $10,000, you can now trade two contracts of the same spread while maintaining the same percentage risk. One contract at $200 max loss was 2.5% of $8,000. Two contracts at $400 max loss is 4% of $10,000. You've increased your dollar exposure proportionally to your account growth while keeping the percentage risk within the 2-5% range.

This is the scaling method I recommend first because it changes nothing about the trade except the size. The delta is the same. The expected move relationship is the same. The management rules are the same. The probability of profit is the same. The only thing that changes is the dollar amount of the credit collected and the dollar amount of the max loss. Your edge doesn't change. Your risk profile doesn't change. Your income scales linearly.

When to do this. When your account has grown by 20-25% through consistent profitable trading. If you started at $8,000 and you're now at $10,000, you've earned the right to increase from one contract to two on your core positions. Don't do it because you're impatient. Do it because the math supports it.

The key discipline. When you add the second contract, your max loss doubles. That means your stop loss, measured in dollars, also doubles. Make sure the larger dollar loss doesn't trigger a different emotional response than the smaller one. If losing $135 on one contract felt manageable but losing $270 on two contracts makes you hesitate to follow your management rules, you've scaled too fast. Scale back to one contract and wait until the larger loss feels routine.

The Second Scaling Move: Widening the Spread (Carefully)

Once you're comfortable trading multiple contracts of $2-wide spreads, the next scaling option is to widen the spread to $3 or $5 while potentially reducing back to one contract.

A $5-wide spread on SPY at the same 0.15-0.20 delta collects more premium per contract than a $2-wide spread at the same delta. If the $2-wide spread collects $0.65 ($65 per contract), the $5-wide spread might collect $1.40 ($140 per contract). The max loss also increases: $360 on the $5-wide spread versus $135 on the $2-wide spread.

The risk-reward ratio is similar. You're collecting roughly one-third of the spread width in both cases. But the dollar amounts are larger per contract, which means you can run fewer contracts to achieve the same income. One contract of a $5-wide spread produces roughly the same credit as two contracts of a $2-wide spread, but with slightly different risk characteristics.

The advantage of wider spreads. Fewer contracts means fewer commissions. It also means simpler management. Rolling one contract is easier than rolling two. Closing one position uses less buying power impact than closing two.

The disadvantage. Your max loss per contract is larger, which means a single losing trade takes a bigger bite out of the account. On a $10,000 account, a $360 max loss on one $5-wide spread is 3.6% of the account. That's within the 2-5% range, but it's at the higher end. Two losing trades in a row at this size is a 7.2% drawdown, which starts to feel significant on a small account.

My recommendation for sub-$10K accounts. Start with $2-wide spreads and scale by adding contracts. Move to $3-wide spreads once the account is consistently above $12,000. Move to $5-wide spreads once the account is above $20,000. At each step, confirm that the max loss per position stays within 2-5% of the current account value.

The Third Scaling Move: Adding a Second Uncorrelated Position

This is the move that most small account traders skip, and it's arguably the most important one.

Instead of putting more capital into the same trade, allocate the growth in your account to a second position on a different, uncorrelated underlying. If you've been trading SPY credit spreads exclusively and the account has grown to $12,000, don't just trade two SPY spreads. Trade one SPY spread and one spread on an uncorrelated underlying like XLE (energy), GLD (gold), or XLV (healthcare).

The total capital deployed is similar. The total risk is similar. But the correlation profile is fundamentally different. Two SPY spreads are one bet on the broad market. One SPY spread and one XLE spread are two bets on different market segments. When SPY drops on a tech-driven selloff, XLE might be flat or rising on oil prices. The diversification benefit at the portfolio level is significant, even with just two positions.

Account thresholds for position count. $8,000-$10,000: 1-2 positions. $10,000-$15,000: 2-3 positions. $15,000-$25,000: 3-5 positions. $25,000+: 5-8 positions. At each level, position sizing stays at 2-5% per trade. The number of positions grows with the account, not the size of individual positions.

The underlyings that work in small accounts. You need tight bid-ask spreads and liquid options chains. SPY is the starting point for almost everyone. After that: QQQ (tech-heavy, but liquid), IWM (small cap, different risk profile), XLE (energy), XLV (healthcare), GLD (gold, often inversely correlated to equities), and TLT (long-term bonds, also often inversely correlated during equity stress). Single-stock options on mega-caps (AAPL, MSFT) work too, but the spread widths available are sometimes less favorable than ETFs for small accounts.

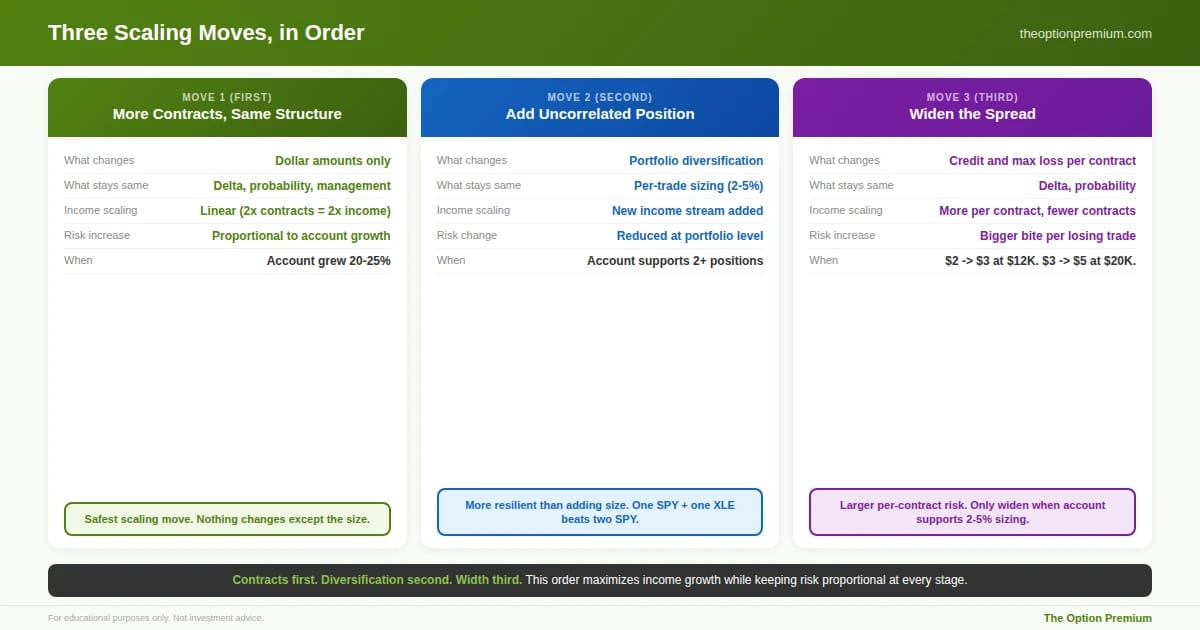

Three scaling moves, in the order that matters. Move 1: add contracts on the same structure you're already trading. Income scales linearly. Edge unchanged. Probability unchanged. Nothing changes except the dollar amounts. This is always the safest first move. Move 2: add an uncorrelated position rather than a bigger position. One SPY spread plus one XLE spread is more resilient than two SPY spreads. The diversification benefit is significant even with just two positions. Move 3: widen the spread. $2-wide to $3-wide above $12K, $3-wide to $5-wide above $20K. More premium per contract, but a bigger bite when the trade loses. Only widen when the max loss stays within 2-5% of account value.

The Trap: Moving to "Bigger" Strategies Too Soon

Here's where small account traders get into serious trouble.

The account is at $10,000. The $2-wide credit spreads are generating $200-$400 per month. The trader reads about iron condors and thinks: if I can collect from both sides, I'll double my income. Or the trader discovers cash-secured puts and thinks: if I sell puts on a $45 stock, I can collect $1.50 per contract ($150) on a single trade. Or the trader considers naked strangles because the credits are massive.

Each of these strategies has its place. None of them belong in a $10,000 account that hasn't yet demonstrated consistent profitability with basic credit spreads.

Iron condors in small accounts. An iron condor is two credit spreads. On a $10,000 account with $2-wide wings on both sides, the margin requirement is approximately $200 per condor (the width of one side, since only one side can lose). The credit collected is roughly $0.50 to $0.80 per condor. The math works, but the management complexity doubles. You now have two spreads to monitor, two potential adjustment scenarios, and the probability that at least one side gets tested is approximately 50% at 0.15 delta on each wing. For a trader who hasn't yet mastered single-side spread management, adding the complexity of two-sided management is a scaling decision that increases stress faster than it increases income.

My recommendation. Master credit spreads first. Demonstrate 6 months of consistent profitability with single-side spreads before adding iron condors. When you do add them, start with one condor at minimal size and treat it as a learning position, not an income position.

Cash-secured puts in small accounts. A cash-secured put on a $45 stock requires $4,500 of buying power. On a $10,000 account, that's 45% of your capital locked in a single position. If the stock drops 20% and you're assigned, you now own $4,500 of a stock that's worth $3,600, and 45% of your account is concentrated in one name. This is the opposite of diversified, disciplined portfolio management.

Cash-secured puts are excellent strategies, but they require enough capital to keep any single put at 5% or less of the account. On a $10,000 account, that means puts on stocks priced at $5 or below, which limits you to names that typically have poor liquidity and wide bid-ask spreads. The strategy doesn't scale well until the account is above $25,000-$30,000.

Naked options in small accounts. Just don't. The undefined risk profile means a single adverse move can destroy 20-50% of a small account. The margin requirements are also punitive for small accounts, often consuming buying power that would be better allocated to multiple defined-risk positions. Naked strategies belong in accounts above $100,000 with experienced traders who understand the risk intimately. In a sub-$10K account, every dollar of buying power is precious. Don't waste it on undefined risk.

The strategies that destroy small accounts when adopted too early. Iron condors double management complexity and should wait until Phase 3 ($12K+) after 6 months of consistent spread profitability. Cash-secured puts on $45 stocks consume 45% of a $10K account in one position, the opposite of diversification, and should wait until Phase 4 ($20K+). Naked options expose small accounts to catastrophic undefined risk and belong only in accounts above $100K. $10-wide spreads create 8.5% risk per trade on a $10K account. The safest scaling move is always the simplest: more contracts of the same structure that's already working.

The Scaling Sequence: A Practical Roadmap

Here's the order I'd recommend for scaling a sub-$10,000 account.

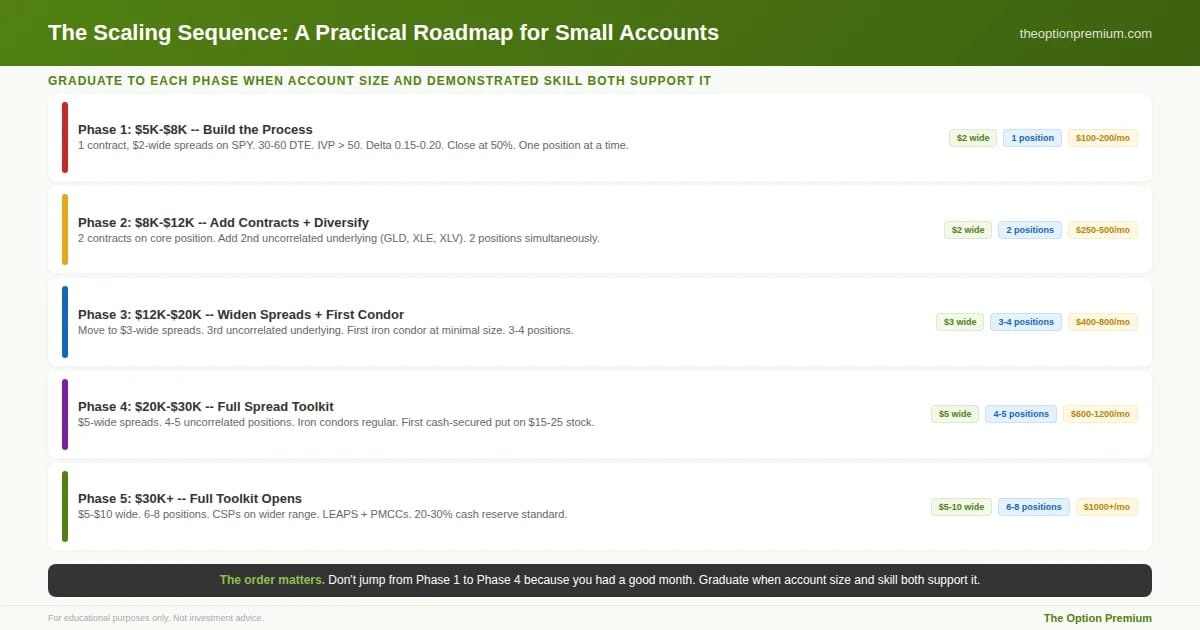

Phase 1: $5,000-$8,000. Trade one contract of $2-wide credit spreads on SPY or another highly liquid ETF. One position at a time. 30-60 DTE. IV Percentile above 50. Delta 0.15-0.20. Close at 50% profit. Stop at 2-2.5x credit. This phase is about building the process, not the income. If the monthly return is $100-$200, that's fine. The percentage return is strong. Let it compound.

Phase 2: $8,000-$12,000. Add a second contract on your core position when the account supports it within 2-5% sizing. Begin adding a second uncorrelated underlying. You're now running 2 positions simultaneously: perhaps 2 contracts of a SPY spread and 1 contract of a GLD or XLE spread. Monthly income: $250-$500.

Phase 3: $12,000-$20,000. Widen to $3-wide spreads while maintaining 2-5% sizing. Add a third uncorrelated underlying. Consider your first iron condor on a position you know well, at minimal size. You're now running 3-4 positions. Monthly income: $400-$800.

Phase 4: $20,000-$30,000. Move to $5-wide spreads on liquid ETFs. 4-5 uncorrelated positions. Iron condors become a regular strategy. The first cash-secured put becomes viable on a lower-priced stock ($15-$25 range) where the buying power commitment stays within 5% of the account. Monthly income: $600-$1,200.

Phase 5: $30,000+. The full toolkit opens. $5-$10 wide spreads. 6-8 uncorrelated positions. Cash-secured puts on a wider range of underlyings. Iron condors as a core strategy. Consider adding LEAPS and poor man's covered calls for capital-efficient stock exposure. The 20-30% cash reserve becomes standard.

Each phase builds on the skills and capital of the previous one. The order matters. You don't jump from Phase 1 to Phase 4 because you had a good month. You graduate to the next phase when the account size and your demonstrated skill both support it.

The five-phase scaling roadmap. Phase 1 ($5-8K): build the process with 1 contract of $2-wide spreads on SPY, one position at a time, targeting $100-200/month. Phase 2 ($8-12K): add a second contract and a second uncorrelated underlying, 2 positions, $250-500/month. Phase 3 ($12-20K): widen to $3, add a third underlying, first iron condor at minimal size, $400-800/month. Phase 4 ($20-30K): $5-wide spreads, 4-5 positions, iron condors regular, first cash-secured put viable, $600-1,200/month. Phase 5 ($30K+): full toolkit opens with 6-8 positions, LEAPS, and 20-30% cash reserve. Graduate when account size and demonstrated skill both support it.

The Hardest Part: Patience With the Compounding

I'll be direct. The hardest part of scaling a small account is not the strategy. It's the patience.

At $8,000, earning $250 per month feels slow. But $250 per month is a 3.1% monthly return. Annualized, that's a 37% return on capital. Professional hedge funds would celebrate that number. The problem isn't the return. The problem is that 37% of $8,000 is $2,960, and $2,960 doesn't feel like it's changing your life.

But $2,960 added to $8,000 makes $10,960. And 37% of $10,960 is $4,055. Now you have $15,015. And 37% of $15,015 is $5,556. Now you have $20,571. In three years, the $8,000 account has become $20,571, and the monthly income at the same percentage return is now $640 instead of $250.

The traders who reach $50,000 and $100,000 in their options accounts didn't get there by taking bigger risks at $10,000. They got there by protecting the $10,000, letting it compound, and scaling the position count and spread width gradually as the account grew. Every time they were tempted to accelerate, they asked the right question: does this increase my compounding rate, or does it increase my risk of a drawdown that resets the clock?

The answer almost always pointed toward patience.

The compounding math that makes patience the real scaling engine. An $8,000 account at 3% monthly return (37% annualized, which is achievable with disciplined premium selling in elevated IV environments) grows to $47,376 in five years without a single additional deposit. Monthly income goes from $240 to $1,421. The account grows 492%. Same process. Same percentages. Same 2-5% position sizing. The compounding did the work. Every scaling decision should be evaluated against this baseline: does this change increase my compounding rate, or does it increase my risk of a drawdown that resets the clock?

Risk Reality Check

Small accounts are inherently more fragile than large ones. A single max-loss trade at 5% of a $10,000 account is $500. That's a 5% drawdown that requires a 5.3% gain to recover. Manageable. But two max-loss trades in the same week is a 10% drawdown, and now you need 11.1% to break even. On a $10,000 account with limited position diversity, correlated losses are more likely because you simply can't spread across as many underlyings.

This fragility is exactly why the scaling sequence matters. The order in which you add complexity protects the account during the period when it's most vulnerable. Adding contracts before adding complexity. Adding diversification before adding strategy types. Adding wider spreads before adding undefined risk. Each step increases income while keeping risk proportional, and each step builds the skill base needed for the next level.

The math of compounding is the small account trader's greatest asset. The math of recovery is their greatest threat. Every scaling decision should protect the first and avoid the second.

Key Takeaways

The safest first scaling move is adding contracts on the same credit spread structure. Moving from one to two contracts of a $2-wide spread doubles your income while keeping percentage risk constant. Nothing about the trade changes except the dollar amounts. Your edge, probability, and management rules remain identical. Scale this way first.

The second scaling move is adding an uncorrelated position, not a bigger position. One SPY spread plus one XLE spread is more resilient than two SPY spreads. The diversification benefit at the portfolio level is significant even with just two positions. Account thresholds: 1-2 positions at $8-10K, 2-3 at $10-15K, 3-5 at $15-25K.

Widen spreads gradually as the account grows. Start with $2-wide. Move to $3-wide above $12,000. Move to $5-wide above $20,000. At each step, confirm that max loss per position stays within 2-5% of account value. Wider spreads collect more per contract but take a bigger bite when they lose.

Avoid "bigger" strategies until the account and skill level support them. Iron condors double management complexity (master single-side spreads for 6 months first). Cash-secured puts require enough capital to keep any single put at 5% or less of account (not viable until $25K+). Naked options don't belong in sub-$10K accounts under any circumstances.

The compounding math is the real scaling engine. $8,000 at 3% monthly becomes $20,571 in three years without any additional deposits. The traders who reach $50K and $100K didn't get there by taking bigger risks at $10K. They got there by protecting the capital, letting it compound, and scaling gradually. Every scaling decision should increase the compounding rate, not the risk of a drawdown that resets the clock.

The account is small. The principles are not. Trade the same process, at the same probabilities, with the same discipline that a $500,000 account uses. The only thing that changes as the account grows is the number of contracts, the width of spreads, and the number of uncorrelated positions. The edge stays the same. The math stays the same. The patience is what makes it all work.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply