- The Option Premium

- Posts

- Iron Condor Strike Selection: Using Expected Move for Optimal Placement

Iron Condor Strike Selection: Using Expected Move for Optimal Placement

Learn to place iron condor strikes using the expected move formula. Covers IV-adjusted width (sell wider when IVP is high), ADX-based symmetry, a 5-step checklist, and 3 real SPY examples.

Andrew Crowder

March 26, 2026

Iron Condor Strike Selection: Using Expected Move for Optimal Placement

Strike selection is what separates iron condors that consistently produce income from iron condors that blow up every other month. You can understand the structure perfectly, know exactly how theta decay works, and still lose money if you're placing your strikes in the wrong spots.

The expected move is the tool that solves this problem. It tells you, based on current implied volatility, how far the market expects the underlying to move over a given period. Place your short strikes outside the expected move, and you're selling premium in the zone where the market is pricing a low probability of the stock reaching. That's not a guarantee. It's an edge, and over hundreds of trades, it's the edge that compounds into consistent results.

This guide covers how to calculate the expected move, where to place your strikes relative to it, and the adjustments I make based on IV Percentile, ADX, and market conditions.

What the Expected Move Is (and Isn't)

The expected move is the market's implied one-standard-deviation price range over a specific time period. It's derived from the underlying's implied volatility and tells you the range within which the stock has approximately a 68% probability of staying.

The formula:

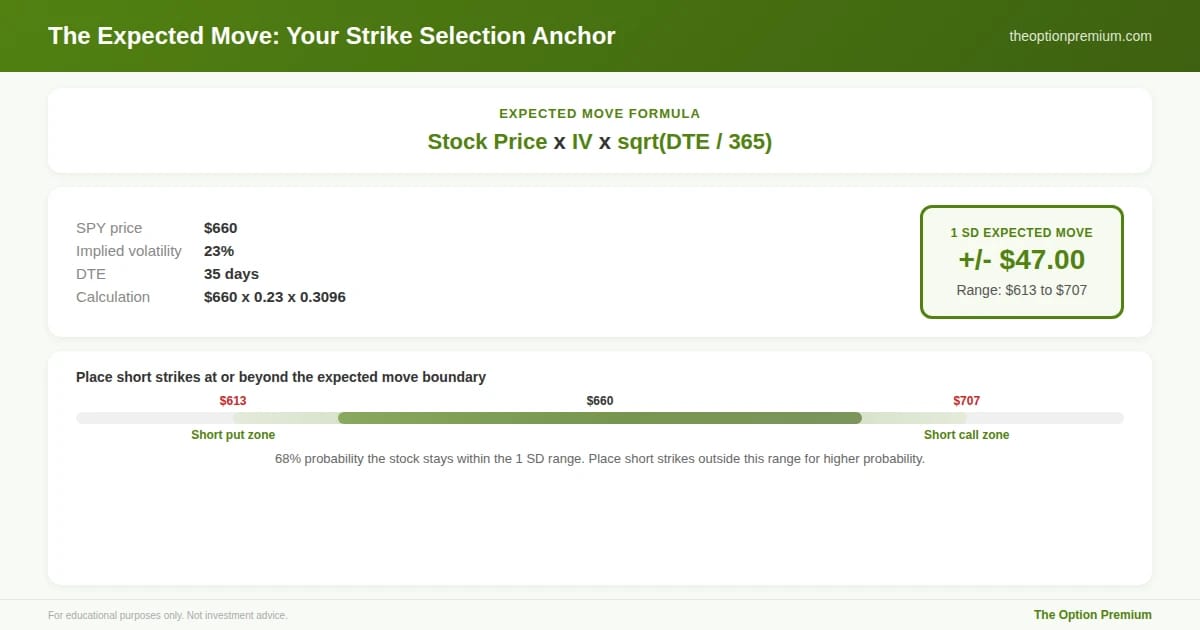

Expected Move = Stock Price x Implied Volatility x Square Root of (DTE / 365)

Example: SPY at $660. IV at 23%. 35 DTE.

Expected Move = $660 x 0.23 x sqrt(35/365) = $660 x 0.23 x 0.3096 = $46.98

One standard deviation (1 SD) range: $613 to $707. The market expects SPY to stay within roughly $47 of its current price over the next 35 days, with about 68% probability.

What it is: A probability-based price range derived from options pricing. It reflects the collective positioning of every market participant. When IV is high, the expected move is wide (the market expects large moves). When IV is low, the expected move is narrow.

What it isn't: A prediction. A guarantee. A ceiling or floor. The stock can and does move beyond the expected move roughly 32% of the time (one out of three occurrences at one standard deviation). The expected move is a probability anchor, not a boundary.

The expected move formula takes 10 seconds and anchors every strike selection decision. SPY at $660 with 23% IV and 35 DTE produces a one-standard-deviation expected move of plus or minus $47, creating a range from $613 to $707. The market expects SPY to stay within this range roughly 68% of the time. Place your short strikes at or beyond these boundaries to sell premium where the market prices low probability. The expected move isn't a prediction. It's a probability anchor.

Placing Short Strikes: The 1 SD Starting Point

The most common approach for iron condor strike selection is to place your short strikes at or near the one-standard-deviation expected move. This gives you approximately 68% probability that each individual side expires out of the money.

On the SPY example above: Short put: near $613 (one SD below) Short call: near $707 (one SD above)

But 68% probability per side isn't the full picture. The iron condor profits if the stock stays between both short strikes, which requires both sides to expire OTM. The combined probability is higher because the stock can only breach one side at a time. An iron condor with 0.16 delta on each short strike (roughly the 1 SD level) typically has a 65-72% probability of full profit.

The practical problem with pure 1 SD placement: The premiums at exactly one standard deviation are often thin. On SPY, a $5 wide put spread at the 1 SD level might pay only $0.60-$0.80. Combined with a similar call spread, the total iron condor credit might be $1.20-$1.60. That can produce ROC below 25%, which doesn't meet the minimum threshold for many premium sellers.

This is why experienced traders adjust their strike placement based on IV environment, not fixed delta targets.

The IV-Adjusted Strike Framework

Instead of placing strikes at a fixed delta or distance, I adjust strike placement based on the current IV Percentile environment. When premiums are rich, I can afford to sell further from the money. When premiums are thin, I need to sell closer to collect adequate premium, but that tighter placement only makes sense when the market is calm enough to support it.

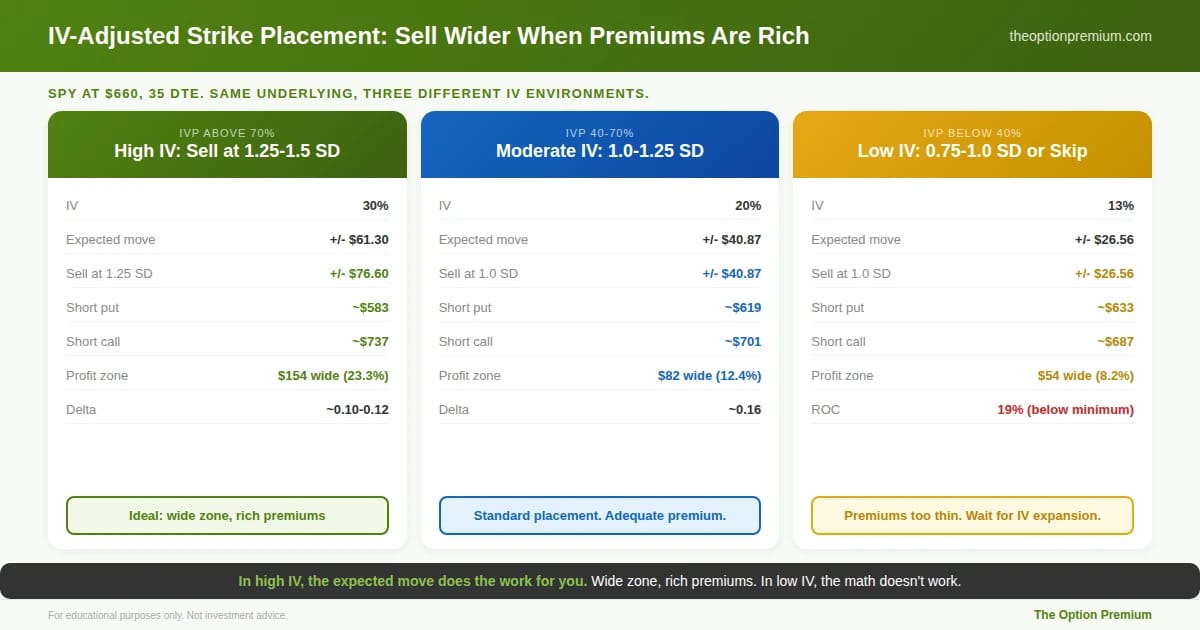

High IV environment (IVP above 70%). Sell at 1.25-1.5 SD from the current price. The expanded expected move means your strikes are further from the stock in absolute dollar terms, yet premiums are still rich. This is the ideal setup: wide profit zone, elevated premium.

On SPY at $660 with 30% IV (IVP above 80%): Expected move = $660 x 0.30 x 0.3096 = $61.30. Selling at 1.25 SD puts your short strikes $76.60 away from the stock. Short put near $583. Short call near $737. The profit zone is $154 wide, or 23.3% of SPY's price. Premium collected is rich because IV is elevated.

Moderate IV environment (IVP 40-70%). Sell at 1.0-1.25 SD. Standard placement. The expected move provides adequate premium at reasonable distance.

Low IV environment (IVP below 40%). Consider selling at 0.75-1.0 SD, closer to the money, to collect adequate premium. But recognize that the tighter placement increases the probability of being tested. In truly low-IV environments (IVP below 25%), iron condors may not offer acceptable risk-reward, and it's often better to wait for volatility to expand.

The key insight: In high IV, the expected move does the work for you. The market is pricing large moves, so your 1.25 SD strikes are far from the money and still pay well. In low IV, the expected move is narrow, forcing you closer to the money for the same premium. This is why iron condors work best when IV Percentile is elevated.

Same underlying (SPY at $660), three different IV environments, dramatically different strike placement. At high IVP (above 70%, IV at 30%), selling at 1.25 SD creates a $154 profit zone (23.3% of price) with rich premiums and 0.10-0.12 delta. At moderate IVP (40-70%), standard 1.0 SD placement gives an $82 zone. At low IVP (below 40%, IV at 13%), the 1.0 SD strikes produce only 19% ROC, below the 25% minimum. In high IV, the expected move does the work for you. In low IV, the math doesn't work.

Factoring in ADX: Trend Strength Matters

The expected move tells you how far the stock might move. ADX tells you whether the stock is likely to move directionally or oscillate. Both matter for iron condor strike selection.

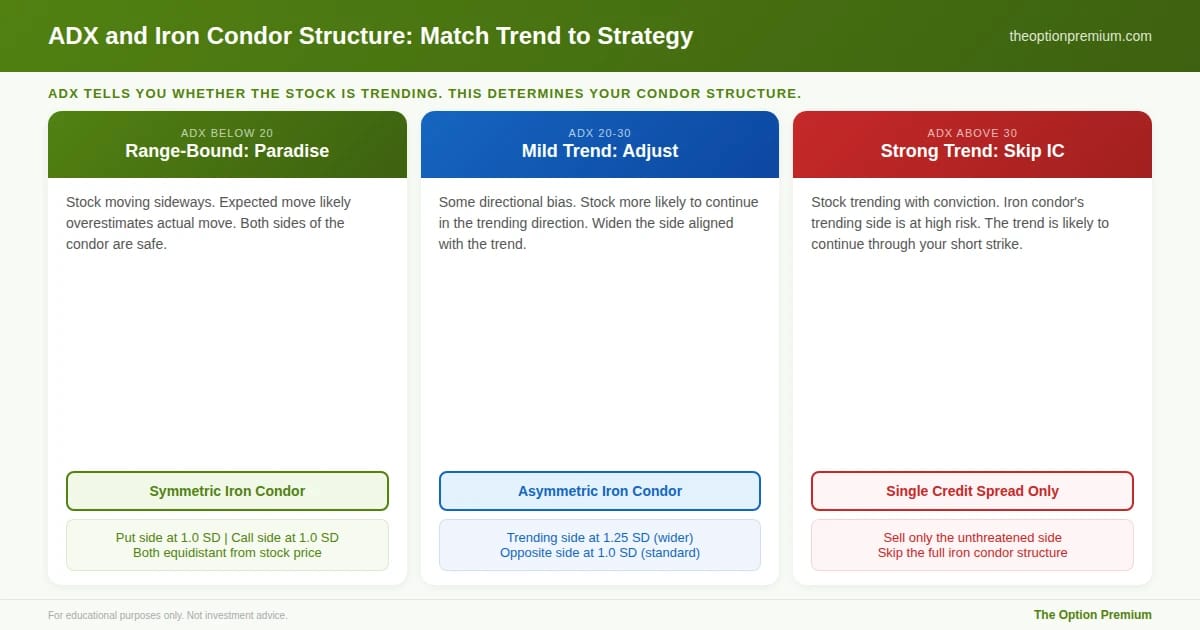

Low ADX (below 20): Range-bound conditions. This is iron condor paradise. The stock is moving sideways, and the expected move is likely to overestimate the actual move. You can place strikes at 1.0 SD with confidence because the stock isn't trending.

Moderate ADX (20-30): Mild trend. The stock has some directional bias but isn't strongly trending. Widen the strikes on the trending side. If the directional indicators show -DI above +DI (bearish lean), move the short put further from the money (1.25 SD) while keeping the short call at 1.0 SD. This creates an asymmetric iron condor that accounts for the directional bias.

High ADX (above 30): Strong trend. Iron condors are risky in strong trends because the stock is likely to keep moving directionally. If ADX is above 30 with a clear directional bias, consider a credit spread on the side opposite the trend instead of a full iron condor. Selling the unthreatened side alone collects less premium but eliminates the risk of the trend continuing through your short strike.

ADX tells you whether the stock is trending and determines your condor structure. Below 20 (range-bound paradise): symmetric iron condor, both sides equidistant at 1.0 SD. The expected move likely overestimates the actual move. ADX 20-30 (mild trend): asymmetric condor, widen the side aligned with the trend to 1.25 SD, keep the opposite side at 1.0. Above 30 (strong trend): skip the iron condor entirely. A single credit spread on the unthreatened side is safer.

Strike Selection Checklist: The 5-Step Process

Here's the exact process I follow for every iron condor.

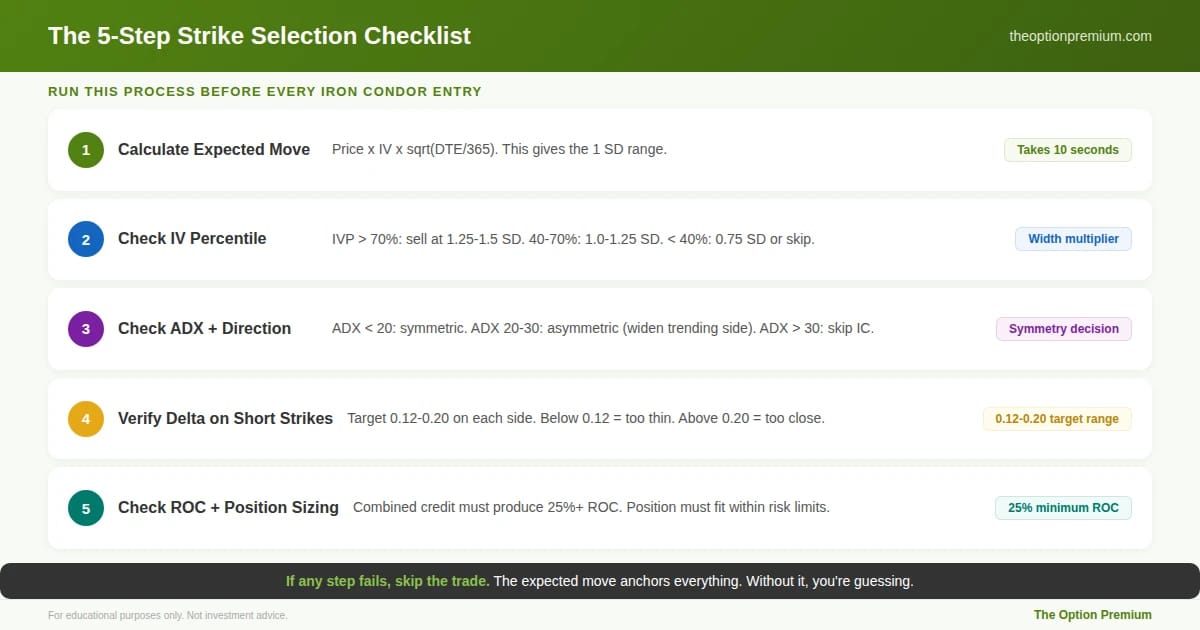

Step 1: Calculate the expected move. Stock price x IV x sqrt(DTE/365). This gives you the one-standard-deviation range.

Step 2: Check IV Percentile. This determines how far outside the expected move you can sell while still collecting adequate premium. IVP above 70% = sell at 1.25-1.5 SD. IVP 40-70% = sell at 1.0-1.25 SD. IVP below 40% = sell at 0.75-1.0 SD or skip.

Step 3: Check ADX and directional indicators. ADX below 20 = symmetric iron condor (both sides equidistant). ADX 20-30 = widen the side aligned with the trend. ADX above 30 = consider a single credit spread instead.

Step 4: Verify delta on the short strikes. After selecting strikes based on expected move and IV environment, check the delta. Target range: 0.12-0.20 on each short strike. Below 0.12 and premiums are too thin. Above 0.20 and the probability of being tested is too high for an iron condor.

Step 5: Check ROC and position sizing. Combined credit on the iron condor must produce at least 25% ROC on the risk. If it doesn't, the trade doesn't meet minimum standards. Check that the position fits within your per-trade and aggregate risk limits.

Run this checklist before every iron condor entry. Step 1: calculate the expected move (10 seconds, anchors everything). Step 2: check IV Percentile to determine how wide to sell (the width multiplier). Step 3: check ADX and directional indicators to decide symmetric vs. asymmetric structure. Step 4: verify the delta on your selected short strikes falls between 0.12 and 0.20. Step 5: confirm the combined credit produces at least 25% ROC and the position fits within your risk limits. If any step fails, skip the trade.

Real Examples: Iron Condor Strike Selection on SPY

Example 1: High IV, range-bound (ideal). SPY at $660. IV at 28% (IVP 92%). ADX at 15. Expected move: $660 x 0.28 x 0.3096 = $57.25. At 1.25 SD: short put near $588, short call near $732. Using available strikes: sell $590/$585 put spread and $730/$735 call spread. Combined credit: $2.10. Max loss per side: $2.90. ROC: 72.4%. Profit zone: $587.90 to $732.10, or $144.20 wide (21.8% of price). Delta on short strikes: ~0.10-0.12.

This is the textbook setup. Wide profit zone, rich premium, low ADX confirming range-bound conditions. The expected move is doing the heavy lifting.

Example 2: Moderate IV, mild bearish lean. SPY at $660. IV at 20% (IVP 55%). ADX at 24. -DI above +DI. Expected move: $660 x 0.20 x 0.3096 = $40.87. Standard 1.0 SD: $619 to $701. But with a bearish lean, widen the put side to 1.25 SD: short put near $609. Keep the call side at 1.0 SD: short call near $701. Sell $610/$605 put spread and $700/$705 call spread. Combined credit: $1.45. Max loss per side: $3.55. ROC: 40.8%. Profit zone asymmetric, wider on the downside.

Example 3: Low IV, skip or tighten. SPY at $660. IV at 13% (IVP 18%). ADX at 12. Expected move: $660 x 0.13 x 0.3096 = $26.56. At 1.0 SD: $633 to $687. Strikes at this level: $635/$630 put spread and $685/$690 call spread. Combined credit: $0.80. ROC: 19%. Below the 25% minimum. This trade doesn't meet standards. Wait for IV to expand.

The Expected Move vs. Actual Move: Why This Works

Implied volatility consistently overestimates actual realized volatility. This is the volatility risk premium: the reason premium selling works. The market prices in larger moves than typically occur because participants pay extra for the insurance of protection.

On SPY specifically, studies have shown that implied volatility exceeds realized volatility roughly 80-85% of the time. This means the expected move is wider than the stock actually moves in most periods. When you sell your short strikes outside the expected move, you're selling in a zone the market is pricing as unlikely, and historically, it's even more unlikely than the pricing suggests.

This doesn't mean you win every trade. The 15-20% of the time when realized volatility exceeds implied volatility is when your iron condors get tested. That's why adjustment strategies and position sizing matter. But it does mean the structural edge is real and consistent over large numbers of trades.

The Practitioner Edge: My Strike Selection Rules

Always calculate the expected move before choosing strikes. It takes 10 seconds and it anchors every decision. Without it, you're guessing.

Sell at 1.0-1.25 SD as default. Wider in high IV. Tighter only when ADX is below 15 and the market is clearly range-bound.

Asymmetric iron condors when ADX shows directional bias. Widen the side aligned with the trend. Keep the opposite side at standard width. This small adjustment improves win rate meaningfully.

Skip iron condors when ADX exceeds 30. Strong trends break iron condors. A single credit spread on the unthreatened side is safer and often collects similar premium to the threatened side of a condor.

Review actual move vs. expected move monthly. I track whether the stock stayed inside the expected move each expiration. Over time, this data tells me whether I should be selling wider or tighter for the current regime.

Risk Reality Check

The expected move is derived from implied volatility, which is forward-looking and constantly changing. A trade placed when IV was 20% can see IV expand to 30% during the life of the trade, effectively widening the expected move after you've already placed your strikes. This is why closing at 50% of max profit and not holding to expiration is so important: you capture your profit before conditions change.

The other risk is regime change. In low-volatility environments, the expected move is narrow and iron condors with tight strikes work well for months. Then volatility spikes, the narrow strikes get blown through, and multiple iron condors take max loss in the same week. This is why the aggregate portfolio cap (20-25% of account) and diversification across underlyings exist: no single regime change should take down your account.

Key Takeaways

The expected move (stock price x IV x sqrt(DTE/365)) tells you the market's one-standard-deviation range for a given period. Place your short strikes at or outside this range to sell premium where the market prices low probability. On SPY at $660 with 23% IV and 35 DTE, the one SD expected move is roughly $47.

Adjust strike placement by IV Percentile environment: sell at 1.25-1.5 SD when IVP is above 70% (wide profit zone, rich premiums), 1.0-1.25 SD in moderate IV, and consider 0.75-1.0 SD or skipping when IVP is below 40% (premiums too thin for the risk).

Factor in ADX for directional context: ADX below 20 is iron condor paradise (symmetric strikes), ADX 20-30 warrants asymmetric placement (widen the trending side), and ADX above 30 is too strong for iron condors (use a single credit spread on the unthreatened side instead).

The 5-step process: calculate expected move, check IVP for width multiplier, check ADX for symmetry, verify delta on short strikes (target 0.12-0.20), and confirm ROC and position sizing pass minimum thresholds.

The structural edge is real: implied volatility overestimates realized volatility roughly 80-85% of the time on SPY. Your short strikes outside the expected move are in a zone that's even more unlikely than the pricing suggests. Over hundreds of trades, this edge compounds into consistent results.

The expected move doesn't predict where the stock will go. It tells you where the market thinks the boundaries are. Sell outside those boundaries, and probabilities do the rest.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply