- The Option Premium

- Posts

- Buy Your Umbrella Before the Storm: Why Smart Traders Purchase Volatility Protection When It's Cheap

Buy Your Umbrella Before the Storm: Why Smart Traders Purchase Volatility Protection When It's Cheap

Academic research proves VIX is a superior hedge that costs 3x less when bought during calm markets. Three practical methods for systematic volatility protection with a 1-2% annual budget.

Andrew Crowder

April 04, 2026

Buy Your Umbrella Before the Storm: Why Smart Traders Purchase Volatility Protection When It's Cheap

You don't buy homeowner's insurance while your house is on fire. You don't buy flood insurance during a hurricane. And you shouldn't buy portfolio protection when the VIX is at 35 and panic is everywhere. Yet that's exactly what most traders do: they ignore volatility protection during calm markets and scramble to buy it when fear is already priced in.

The academic research on this is unambiguous. Volatility protection purchased during low-VIX environments is cheaper, more effective, and produces better risk-adjusted portfolio returns than protection purchased reactively during a crisis. The VIX (the CBOE Volatility Index) is a forward-looking measure of expected 30-day volatility on the S&P 500, derived from options prices. When it's low, protection is cheap. When it's high, protection is expensive and often too late.

This article covers what the research says, why the math works the way it does, and exactly how to implement a systematic hedging program that buys protection during calm periods so you're covered before the next storm arrives.

What the VIX Actually Tells You

The VIX was formally described by Robert Whaley in his foundational 2009 paper "Understanding the VIX" in the Journal of Portfolio Management. Whaley characterized it as a "fear gauge" that reflects the market's consensus expectation of future volatility. When the S&P 500 falls sharply, investors rush to buy put options for protection, driving up options prices and pushing the VIX higher. When markets are calm and rising, demand for protection falls, options get cheaper, and the VIX drops.

There are several well-documented properties of the VIX that matter for hedging decisions. Multiple academic studies have confirmed a persistent negative correlation between the VIX and equity returns (Brenner and Galai 1989, Whaley 2009). Researchers have also documented mean reversion, where VIX tends to return to its long-run average after spikes (Hafner 2003, Bali and Demirtas 2006). The VIX also displays asymmetric volatility, reacting more strongly to negative market moves than positive ones (Whaley 2009), and volatility clustering, where high-volatility periods tend to be followed by more high volatility before eventually subsiding (Cont 2005).

The mean reversion property is the key to the entire hedging argument. When VIX is at 12-15, it's historically low. When it spikes to 30-40 during a selloff, it will eventually revert toward its long-term average (historically around 19-20). This means: protection bought when VIX is low is bought at a discount to its average cost. Protection bought when VIX is high is bought at a premium to its average cost. The directional move you're hedging against has likely already happened by the time VIX is elevated.

The Research: VIX Beats Gold, Bonds, and Everything Else as a Hedge

One of the most cited studies on this topic is Hood and Malik (2013), published in the Review of Financial Economics. They evaluated the role of gold, silver, platinum, and the VIX as hedges and safe havens for US equities using daily data from November 1995 to November 2010. Their findings were decisive.

Gold served as a hedge (negatively correlated with stocks on average) and a weak safe haven (negatively correlated during extreme stock market declines). But the VIX served as a very strong hedge and a strong safe haven. The critical distinction: during periods of extremely low or high volatility, gold lost its negative correlation with stocks entirely. The VIX maintained its negative correlation with US equities even during the most extreme market conditions. When you need protection the most, gold can fail you. The VIX does not.

This finding has been confirmed repeatedly. Research from Siranosian at Stanford evaluated a strategy of systematic hedging using out-of-the-money VIX call options. The study found that while these options frequently expire worthless during calm markets (creating a modest drag on returns), they can return 10 to 100 times their initial value during volatility spikes. A systematic allocation of 1-2% of a portfolio to VIX call hedges improved risk-adjusted returns over full market cycles, including the periods where the options expired worthless.

QuantPedia's research on VIXY-based hedging strategies confirmed that portfolios including volatility-linked assets performed better in out-of-sample testing than portfolios relying solely on diversification. The key finding: diversification alone fails during the exact moments you need protection most, because correlations converge during crises. All asset classes tend to move together during panics, which is precisely when a volatility hedge pays off.

Why Protection Is Cheaper When VIX Is Low (and How Much Cheaper)

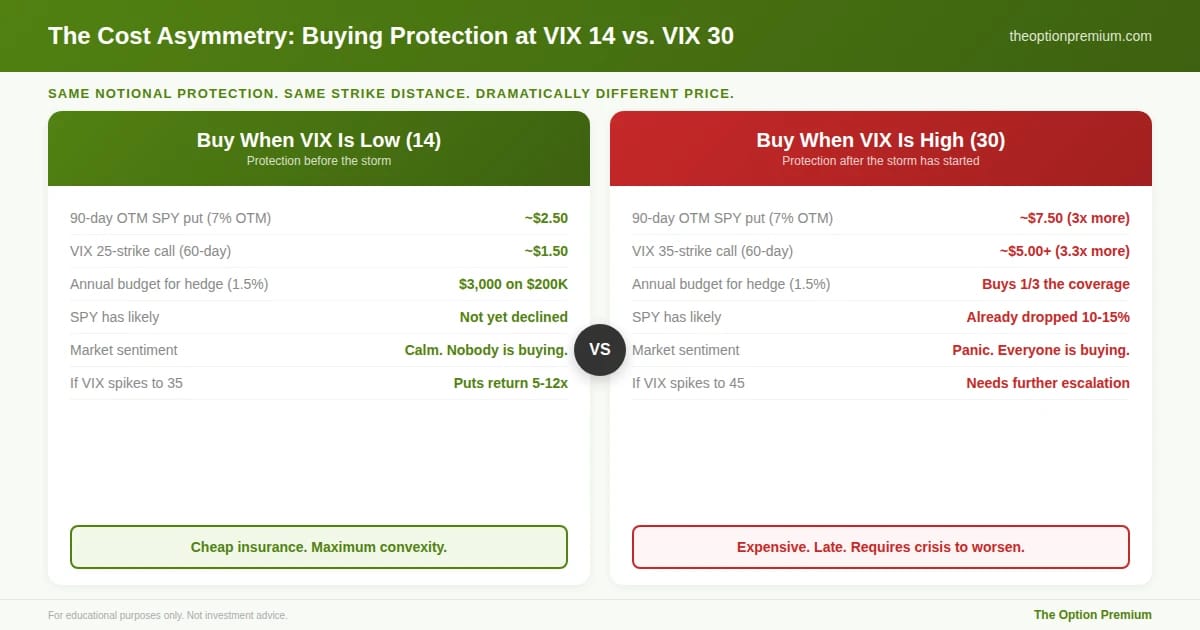

The cost difference between buying protection at VIX 14 versus VIX 30 is not incremental. It's exponential.

Options prices are directly derived from implied volatility. When VIX is at 14, a 90-day out-of-the-money SPY put might cost $2.50. When VIX is at 30, that same put (same strike distance, same expiration) might cost $7.00-$8.00. You're paying nearly 3x more for the same notional protection, and the underlying has likely already fallen 10-15% by the time VIX reaches 30.

VIX call options show the same pattern. A VIX 25-strike call option with 60 days to expiration might cost $1.50 when VIX is at 14. That same option costs $5.00+ when VIX is already at 22. And if VIX is already at 30, you're buying calls at 35 or 40 for elevated premiums on protection that may not pay off unless the crisis escalates further.

Kownatzki (2016), in the Journal of Accounting and Finance, documented an important asymmetry in the VIX's predictive behavior. The VIX systematically overestimates actual realized volatility during non-crisis periods (when VIX is low, actual moves tend to be even smaller). But it underestimates actual volatility during crises (when VIX is high, the actual moves can be even larger than implied). This means: when you buy protection cheaply during calm markets, you're buying from sellers who are overestimating the near-term risk, giving you a slight edge. When you buy during a crisis, you're buying from sellers who may still be underestimating how bad it can get, and you're paying a massive premium for the privilege.

The cost asymmetry is not incremental. It's exponential. A 90-day OTM SPY put costs roughly $2.50 when VIX is at 14, but $7.50 when VIX is at 30. That's 3x more for the same notional protection, and the underlying has likely already fallen 10-15% by the time VIX reaches 30. When you buy cheap, every dollar of hedging budget buys maximum coverage with maximum convexity. When you buy during a panic, you're paying peak prices for protection that requires the crisis to worsen further just to break even.

The Behavioral Trap: Why Most Traders Get This Backwards

If the math is so clear, why does almost everyone buy protection at the wrong time?

Recency bias. During calm markets (VIX at 12-15), it feels like the calm will last forever. There's no visible threat. Spending money on protection when your portfolio is making money every week feels wasteful. The premium you pay for puts or VIX calls feels like a tax on your returns.

Loss aversion in reverse. During a crisis (VIX at 30+), the pain of recent losses makes the cost of protection feel justified at any price. The fear of further losses overwhelms the rational calculation that protection is now 3x more expensive and the underlying has already moved.

The insurance analogy is perfect. Home insurance costs $1,500 per year when your house is standing. If you could somehow buy it after a fire started, it would cost $50,000. The rational choice is obvious. Yet in financial markets, the majority of "insurance" buying happens after the fire has started. The institutional research from HL Hunt confirms this pattern: dynamic hedging that adjusts to volatility regimes systematically outperforms static or reactive approaches. Their framework suggests that protection should be heaviest when VVIX (the volatility of VIX itself) is below 100 and VIX is below 20, not when fear is already elevated.

How to Implement: A Practical Hedging Framework

Here's a systematic approach to buying volatility protection that any options trader can implement. The goal is to maintain consistent, affordable protection that's already in place before the next crisis hits.

Method 1: Rolling OTM SPY Puts (The Simplest Approach)

Buy out-of-the-money SPY puts, 5-10% below the current price, with 60-90 days to expiration. Roll them every 30 days to maintain consistent coverage. Budget 1-2% of your portfolio value per year on this protection.

When VIX is below 18: buy the puts at full allocation (1-2% of portfolio per year). This is when protection is cheapest and you get the most strikes-per-dollar of protection.

When VIX is 18-25: maintain but don't add. Continue rolling existing puts but don't increase the allocation. Protection is moderately priced.

When VIX is above 25: your puts are already working. Do not buy additional protection at inflated prices. If your puts are showing large gains, consider taking partial profits and repositioning when VIX normalizes.

Example: $200,000 portfolio. Annual hedging budget: $3,000 (1.5%). That's roughly $250 per month. With VIX at 14, a 90-day SPY put 7% out of the money might cost $2.50 ($250 per contract). You buy 1 contract per month, rolling as they approach 30 DTE. If SPY drops 15% and VIX spikes to 35, those $250 puts could be worth $1,500-$3,000 each. The 3-4 puts you have in place could generate $5,000-$10,000 of hedge value against a $30,000 portfolio loss, reducing the drawdown by 15-30%.

Method 2: VIX Call Options (The Convexity Approach)

Buy out-of-the-money VIX calls (strike 25-30 when VIX is at 14-18) with 60-90 days to expiration. The Siranosian research at Stanford found that 0.10 delta VIX calls (far OTM) provide the most convexity: they cost very little but can return 10-100x during severe spikes. Budget 0.5-1% of portfolio per year.

The advantage of VIX calls over SPY puts: VIX has a more explosive upside during crises. SPY might fall 20%, but VIX can rise 200-300%. This convexity means a small allocation to VIX calls can generate outsized protection during the worst scenarios.

The disadvantage: VIX options are settled in cash and expire on Wednesdays (not Fridays). They're based on VIX futures, not spot VIX, which means there's a basis risk. During moderate selloffs, VIX calls may not pay as much as expected because VIX futures don't move 1:1 with spot VIX.

When to use this: Best for tail risk hedging (the 2008, March 2020, or August 2024 type events). Less effective for routine 5-7% corrections.

Method 3: The Collar (For Premium Sellers)

If you're already running a premium selling portfolio with credit spreads and iron condors, you can fund your hedging program from the premium you collect. Dedicate 10-15% of your monthly premium income to purchasing protective puts or VIX calls.

On a portfolio generating $2,000 per month in premium: allocate $200-$300 to rolling OTM puts or VIX calls. Your net income drops from $2,000 to $1,700-$1,800 per month, but you have crash protection in place permanently. When the next 20% selloff arrives, your hedges offset a significant portion of the losses on your short premium positions. The premium sellers who survive decades in this business all have some version of this approach.

Three approaches for systematic volatility protection, each suited to different portfolios and experience levels. Method 1 (rolling OTM SPY puts) is the simplest: 5-10% OTM, 60-90 days, rolled monthly, 1-2% annual budget. It protects against both moderate and severe declines. Method 2 (OTM VIX calls) provides maximum convexity: 0.10 delta calls can return 10-100x during severe crises on just 0.5-1% annual budget, but they're less effective in mild corrections. Method 3 (the funded collar) is for premium sellers: dedicate 10-15% of your monthly premium income to protective puts or VIX calls. Your net income drops slightly, but you have permanent crash protection. This is how the premium sellers who survive decades do it.

When to Activate, When to Wait, and When to Take Profits

VIX below 15 (complacency): Maximum hedge allocation. Protection is at its cheapest. Buy your full allocation of puts or VIX calls. This is the fire insurance equivalent of buying coverage on a sunny Tuesday.

VIX 15-20 (normal): Standard allocation. Roll existing hedges. Don't increase or decrease. The market is pricing risk fairly.

VIX 20-25 (elevated concern): Maintain, don't add. Your existing hedges are gaining value. Adding more at this level is more expensive per unit of protection. If you don't have any hedges in place, this is your last chance to buy at reasonable prices, but keep the allocation modest.

VIX above 25 (fear/crisis): Your hedges are working. Do not buy more. Consider taking partial profits on hedges that have appreciated 3-5x. If VIX spikes above 35-40, sell 50-75% of your hedge positions (they've done their job) and set aside the proceeds to re-establish hedges once VIX normalizes back below 20.

VVIX above 120 (elevated tail risk): Be alert. Research from institutional volatility analysis frameworks indicates that VVIX readings above 120 suggest options market participants are pricing increased probability of extreme moves. If your hedges are not already in place and VVIX is above 120 while VIX is still below 20, that's a particularly urgent signal to establish protection.

Match your hedging activity to the VIX regime. Below 15 (complacency): maximum allocation, protection is cheapest, nobody is buying. 15-20 (normal): roll existing hedges at fair prices. 20-25 (elevated): your hedges are gaining value, don't add at expensive levels. Above 25 (fear/crisis): your hedges are working. Take profits on positions that have appreciated 3-5x. Then re-establish at full allocation once VIX normalizes below 20. This is the opposite of what most traders do, which is exactly why it works.

The Cost of Not Hedging: What the Data Shows

The argument against systematic hedging is always the same: "It's a drag on returns." And that's true. Spending 1-2% per year on protection that usually expires worthless does reduce your annual return by 1-2% in calm years.

But the math of drawdowns is unforgiving. A 30% drawdown requires a 43% gain to recover. A 50% drawdown requires a 100% gain. The 2008 financial crisis took the S&P 500 from its 2007 highs to a March 2009 low of roughly 57% below that peak. Recovering that loss took over four years.

A portfolio with 1.5% annual hedging cost that reduces a 30% drawdown to a 20% drawdown gives up perhaps 1.5% per year in 7 calm years (10.5% cumulative cost) but avoids 10 percentage points of drawdown in the crisis year. The net math: the hedge cost 10.5% over the calm years and saved 10% in the crisis. Nearly break-even on absolute numbers, but the psychological and practical benefits (not being forced to sell at the bottom, not needing 43% to recover versus 25%) are enormous.

The Siranosian research found that systematic VIX call buying with a 1-2% allocation improved both overall and risk-adjusted portfolio returns over full market cycles. The cost during calm years was more than offset by the payoffs during crises.

The math of drawdowns is unforgiving and asymmetric. A 30% loss doesn't require 30% to recover. It requires 42.9%. A 50% loss requires 100%. The 2008 crisis took over four years to recover from peak to prior high. A hedged portfolio spending 1.5% annually that reduces a 30% drawdown to 20% needs only 25% to recover instead of 43%. Over a full cycle, the cost (1.5% x 7 calm years = 10.5%) nearly equals the savings (10 percentage points of avoided drawdown), and the psychological benefit of not being forced to sell at the bottom is incalculable.

The Practitioner Edge: My Hedging Rules

Always be hedged. Maintain some level of protection at all times. The crisis you don't see coming is the one that matters.

Budget 1-2% of portfolio value annually for hedging. Think of it as insurance, not a profit center. Some years it costs you money. The year it saves you, it saves your account.

Buy the most protection when it's cheapest (VIX below 18). This is counterintuitive because there's nothing to worry about. That's the point.

Take hedge profits during spikes, then re-establish. When VIX spikes above 30-35, your hedges have likely appreciated 3-5x or more. Take 50-75% off the table. Wait for VIX to normalize (below 20), then re-establish the full hedge.

Never buy protection reactively. If you don't have hedges and VIX is already at 30, the horse has left the barn. Accept the current drawdown, manage your existing positions, and plan to establish hedges once volatility normalizes. Buying expensive protection in a panic is how traders compound their losses.

Review quarterly. Track your hedging cost, the current protection level, and whether your strikes need adjustment based on the portfolio's current value. A put that was 7% OTM three months ago may be 12% OTM after a rally, offering less effective protection.

Risk Reality Check

Systematic hedging is not a magic bullet. There are real costs and limitations.

The drag is real. In a decade with no major crisis, you'll spend 10-20% of cumulative returns on protection that never pays off. Some investors find this psychologically difficult.

VIX products have structural costs. VIX futures trade in contango most of the time (further-dated futures are more expensive than near-term). This means VIX-based ETFs like VIXY lose value steadily during calm markets. If you use VIX ETFs instead of options, the decay is significant.

Basis risk exists. VIX options are based on VIX futures, not spot VIX. During moderate selloffs, spot VIX might spike to 25 but VIX futures only move to 21-22. Your VIX calls may not pay as much as expected in these scenarios.

The hedge can expire just before the crisis. If you're rolling 60-day puts monthly and the crash happens the day after your old puts expire and before your new puts are established, you have a gap. Staggering your hedges (holding 2-3 different expirations simultaneously) reduces this risk.

Key Takeaways

Academic research consistently shows the VIX is a superior hedge and stronger safe haven than gold, bonds, or other traditional defensive assets. Hood and Malik (2013) found that VIX maintains its negative correlation with equities even during extreme market conditions, while gold's correlation breaks down precisely when you need it most.

Volatility is mean-reverting (Hafner 2003, Bali and Demirtas 2006, Whaley 2009). When VIX is low, it will eventually spike. When it spikes, it will eventually revert. This means protection bought during calm, low-VIX periods is purchased at a structural discount to its average value, and the explosive upside of volatility during crises creates convexity that can return 10-100x on hedging positions.

The cost asymmetry is massive. The same notional protection costs roughly 3x more when VIX is at 30 versus VIX at 14. Buying reactively during a crisis means paying peak prices for protection after the market has already fallen. Buying systematically during calm periods means paying discount prices before the move happens.

Implementation requires discipline and a budget: allocate 1-2% of portfolio value annually to rolling OTM SPY puts (5-10% below current price, 60-90 days out) or 0.5-1% to OTM VIX calls. Buy the most when VIX is below 18 (cheapest), maintain when VIX is 18-25, and take profits when VIX spikes above 30. Never buy reactively at inflated prices.

The math of drawdowns justifies the cost: a 30% loss requires a 43% gain to recover. A 1.5% annual hedging cost that reduces a 30% drawdown to 20% pays for itself over a market cycle, both in absolute terms and in the psychological and practical benefits of avoiding forced selling at the bottom.

You don't buy an umbrella during the storm. You buy it on a sunny day, when it's cheap, when nobody else is thinking about rain, and when you can choose exactly the one you want. The same principle applies to your portfolio.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply