- The Option Premium

- Posts

- 📩 The Option Premium Weekly Issue – March 23, 2025

📩 The Option Premium Weekly Issue – March 23, 2025

This Week’s Must-Know IV Ranks, Oversold Trades & Strategic Takeaways

⚡ In This Issue: Time Decay, Mispriced Volatility, and Where the Trading Edge Is Now

Markets finally bounced this week after a month of weakness, with small-caps leading the move higher and volatility pulling back. But under the surface, the story is more about positioning and potential than momentum. Hedge funds remain defensively postured, tech is starting to show signs of real fatigue, and capital is beginning to rotate — slowly — into areas that have been overlooked for most of the year. That kind of shift doesn’t always lead to immediate follow-through, but it often sets the stage for better two-sided trading opportunities.

What we’re seeing now is a market in transition. Breadth is improving, volatility is stable, and short-term fear is easing — conditions that often favor range-bound setups and premium-selling strategies. But with economic data on deck and macro uncertainty still in the background, staying nimble remains essential. This isn’t a time to chase; it’s a time to structure trades carefully, take what the market is giving, and stay focused on process over prediction.

In this week’s issue of The Option Premium, we focus on what matters most for options traders:

Why time decay remains the most consistent edge — and how to structure a portfolio that takes advantage of it

How recent shifts in hedge fund positioning, tech sector fatigue, and improving breadth are creating new premium-selling opportunities

Where volatility is being mispriced, and how to trade it using iron condors, vertical spreads, and short puts

A breakdown of this week’s top IV Rank and RSI trade setups — including tickers like XHB, XLF, XRT, and EEM — and why these conditions matter right now

We’ll also cover the most common execution mistake traders make — and how to close the gap between having a solid strategy and consistently following it.

This issue is built to help you focus on process, stay objective, and trade setups with real statistical edge. Let’s get started.

🚀 Big Changes Are Coming to The Option Premium!

Options trading isn’t about luck—it’s about process. Strategy, discipline, and risk management drive long-term success. Too many traders jump into setups without a clear plan.

That’s why after 23+ years as a professional options trader I’m launching three focused services in the next two weeks—designed to help you build a repeatable, structured system for trading options. These aren’t quick-fix tools. They’re frameworks developed from experience and grounded in probability.

I’m not here to flood your inbox with sales pitches or pressure you into upsells. Unlike 99% of all the options trading newsletters out there, I’m not a direct marketer. I’m an options trader. My focus is on building something real—a community of traders, both new and experienced, who value long-term consistency and transparency over hype and noise.

Use what’s helpful—free or paid. If it helps you grow, share it with others who might be able use it.

Stay tuned.

📈 Market Snapshot & Commentary

Market Performance Overview

Markets took a breath this week.

After a month of slow bleed and chop, all four major indices finally managed to close in the green. It wasn’t a runaway rally, but it was meaningful—especially when viewed through the lens of positioning, implied vol, and where the bid showed up.

S&P 500: +0.5%

Dow Jones (DIA): +1.2%

Nasdaq 100 (QQQ): +0.2%

Russell 2000 (IWM): +0.5%

The leadership wasn’t flashy. Tech cooled, mega caps treaded water, but the Dow quietly led, driven by industrials and energy. Small caps (IWM) had a subdued bounce—less than last week’s surge—but still noteworthy, considering the unwind in risk-off positioning we've been tracking.

That’s the part to watch.

When fear gets priced out of small caps first, it’s not just a sigh of relief—it’s often an early signal of broader recalibration. Dealers lighten up, hedges come off, and liquidity pockets start to form where the tape had been dead.

Volatility backed off again, with the VIX settling into the 19–20 range. That doesn’t scream “all clear,” but it does suggest fewer immediate catalysts on the horizon. The market isn’t pricing in macro shock, but it’s also not leaning bullish. Just… less hedged.

In a word: equilibrium. Fragile, maybe. But for now, it holds.

Key Influences

1. The Fed Didn’t Blink — And That Was Enough

Powell didn’t offer surprises—he just didn’t tighten the screws. Rate cuts remain on the table for later in the year, even with hotter inflation prints. That was all the market needed. On Wednesday, we saw one of the strongest “Fed Day” rallies since last summer.

2. Hedge Funds Are Hedging—Heavily

According to Goldman Sachs, hedge fund positioning is the most defensive since 2020. Some of that is macro—they’re chasing non-U.S. growth. But it also reflects crowding into a narrow tech leadership trade. That crowded positioning is fragile, which could fuel both air pockets and sharp reversals in high beta names.

3. Tech’s Cracks Widen

Apple, Tesla, and even semis like Nvidia looked tired. There’s rotation under the hood, and while that doesn’t scream “top,” it does signal the easy beta trade may be behind us—for now.

4. Breadth Is Quietly Improving

Advance-decline lines are stabilizing, and we're seeing better participation outside of the Magnificent 7. That’s constructive, especially for premium sellers focused on range-bound setups.

Looking Ahead

This week is all about data and digestion.

Here’s what traders should keep on the radar:

Monday: Flash PMIs — watch for growth surprises.

Tuesday: Consumer Confidence — cracks here could shake the soft landing narrative.

Wednesday: Durable Goods — a backward-looking report, but the market’s on edge for signs of slowing.

Friday: PCE Inflation — this is the Fed’s favorite metric. If it comes in hot, the soft glidepath for cuts gets harder to justify.

The Bottom Line for Options Traders

Volatility is hovering around 20—ideal for premium selling, but stay nimble. Markets are coiled, not complacent.

Breadth improving + small-cap strength = potential for iron condors and strangles across IWM, mid-tier ETFs, and sector names with mean-reverting tendencies.

Tech fatigue + defensive flows = vertical spread opportunities in overbought/oversold names with lagging breath (watch RSI + IV Rank divergences).

Hedge fund defensiveness isn’t a short signal, but it does mean reversion trades could accelerate if the crowd gets caught offside.

🔹 Market Meter:

📜 Investment Quote of the Week

💬 “The goal is not to predict the future, but to profit from the passage of time.”

This idea is the central philosophy behind The Option Premium: a shift away from the futile exercise of market forecasting and toward building systematic, probability-driven trades that let time and volatility work in our favor.

Most retail traders wake up each morning trying to guess what the market will do next. They chase headlines, overanalyze short-term price action, and convince themselves that if they just find the right chart or indicator, they can predict the future. But predicting the future is not a requirement for success in options trading — in fact, it’s often a liability.

The consistent edge lies in understanding how time functions within an options contract. Every day that passes, theta — time decay — does its work. Prices can whip around. Volatility can spike. News can surprise. But time always marches forward, and if your portfolio is structured properly, that passage of time becomes your income.

Theta decay is not theoretical — it’s the core engine of every premium-selling strategy we trade. Iron condors collect premium as long as price remains within a defined range. Strangles and straddles profit from overstated implied volatility. Cash-secured puts reward you for waiting patiently on a better entry, and poor man’s covered calls offer a capital-efficient strategy that generates steady income while systematically reducing cost basis. These strategies have one thing in common: they are not dependent on price direction. They are dependent on expectation versus reality — and the market's persistent tendency to overprice movement. That mispricing is where we find our edge.

Constructing a time-based options portfolio requires a different mindset. Rather than making one-off directional bets, the goal is to create a structure that generates income consistently across varying timeframes, volatility regimes, and probability ranges. Think of it like managing a well-run insurance business. The focus is on selling risk — but only at the right price and across a diverse book of policies.

One of the most effective methods is to ladder your expirations. Concentrating all of your positions in the same expiration window is a common mistake. Instead, use a mix of short-term (0–7 DTE) trades to capture rapid theta decay, intermediate (30–45 DTE) trades for core income positions, and longer-term (60–90 DTE) setups for lower maintenance and smoother P&L. The result is a rolling series of expirations — a calendar of consistent decay that functions like a dividend-paying portfolio.

Equally important is matching your strategy to the volatility environment. When implied volatility is high — especially relative to its historical percentile — you want to be a net seller of premium. That’s when wide strangles, iron condors, and credit spreads offer the most favorable risk-reward profile. When IV is low, selling naked premium is less attractive. In those conditions, consider using calendar spreads, diagonals, or defined-risk verticals to benefit from potential reversion in volatility or directional lean. Don’t trade based on feel — trade based on where volatility is priced relative to realized movement.

Lastly, structure your portfolio for probability, not excitement. It’s tempting to chase high-delta trades that offer big potential returns, but those setups rarely work over the long haul. The professionals — the traders who consistently take money out of the market — focus on high-probability setups in the 65%–85% range. Small edges, repeated over dozens of trades, create meaningful, compounding returns. That’s not speculation. That’s a business model.

As a practice this week, before placing any trade, ask yourself: am I trying to predict the market, or am I building a portfolio that profits from mispriced expectations? If your portfolio only works when you’re right on direction, you’re not truly managing risk — you’re gambling.

Review your open trades. Are they concentrated in one expiration? Are you unintentionally leaning too hard in one direction? Are you using implied volatility rank to guide your strategy choices? If the answer to any of those questions is yes, it might be time to realign. A healthy premium-selling portfolio should resemble a factory — generating consistent income from time, not depending on a single outcome.

In the end, time decay is a gift — one the market offers every day. But only traders who understand how to structure their portfolios around it will be in a position to accept it.

📰 Weekly In-Depth Articles

🗓️ Tuesday, March 18th: How to Build a Dividend Aristocrats Portfolio Using a Poor Man’s Covered Call Strategy

🗓️ Thursday, March 20th: March Madness and Options Trading: The Statistical Edge Every Trader Needs

🗓️ Friday, March 21st: Liquidity: The Lifeblood of Options Trading

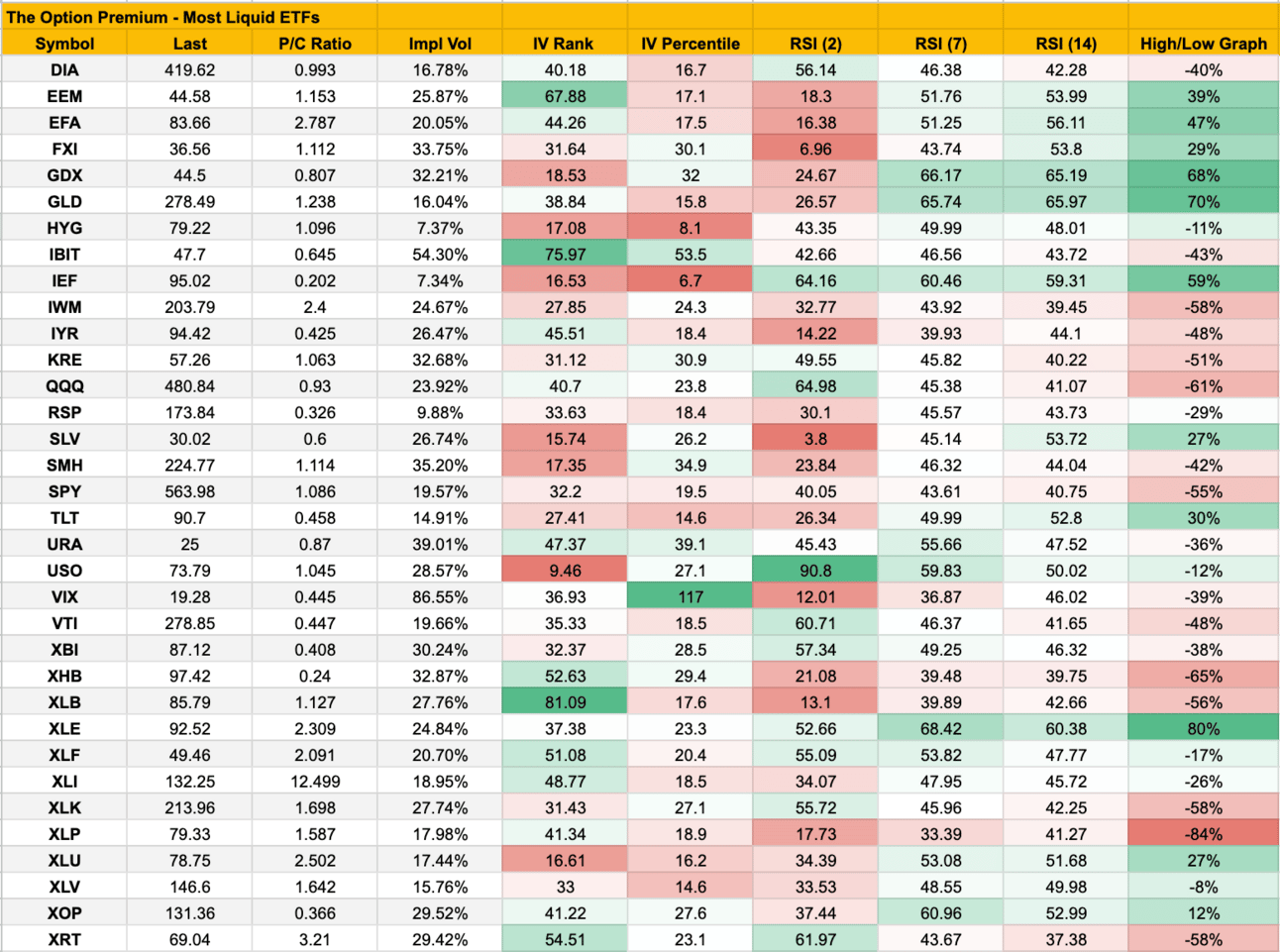

📊 Weekly Table Overview: The Implied Truth

Now we’ve arrived at what’s quickly become the most popular section of The Option Premium. As always, if you have any questions please do not hesitate to email me. I’m more than happy to help in any way I can.

This week’s snapshot distills the signals that matter: where volatility is overpriced, momentum is stretched, and risk is mispriced — the sweet spots for premium sellers.

Options traders aren’t in the business of guessing direction. We exploit misalignments — when implied volatility deviates from realized moves, or when momentum pushes markets into extremes. The Implied Truth pulls from the most liquid ETFs to surface exactly that.

Right now, we’re seeing a bifurcated tape. A few sectors are swimming in premium — perfect for iron condors, strangles, and other theta-friendly setups. Others? They’re hitting RSI levels that historically precede mean reversion.

This is where edges are found — not in noise, but in the dislocations.

Here’s what the data is implying this week.

At the close March 21, 2025

(IV Rank > 50 = Rich Premiums)

These ETFs are showing historically expensive option pricing and offer strong setups for short premium trades:

XLB (Materials) – IV Rank: 81.1

Volatility is quietly building despite low IV percentile. This suggests compression within a volatile range—ideal for iron condors or wide call/put spreads.XHB (Homebuilders) – IV Rank: 52.6

Elevated IV plus low RSI(7) makes this a dual setup: short puts or iron condors can capitalize on mean reversion and inflated premiums.XLF (Financials) – IV Rank: 51.1

Stable momentum with modestly high IV makes this a textbook credit spread candidate.XRT (Retail) – IV Rank: 54.5

This ETF is oversold across all RSIs, and premiums are rich. Ideal for structured put spreads or wide-range condors.

📌 Takeaway: These names offer some of the best premium-selling environments we've seen in weeks—especially where elevated IV meets emotional RSI extremes (like XHB and XRT).

2. RSI Extremes: When Momentum Overreacts

(RSI(2), RSI(7), and RSI(14) aligned = Contrarian Opportunity)

🔻 Oversold Reversal Candidates

SLV (Silver) – RSI(2): 3.8

Extreme short-term weakness. While IV is low, the setup favors long calls or diagonal spreads for a defined-risk reversal.XLP (Staples) – RSI(2): 17.7 | RSI(7): 33.3

A high-beta defensive sector under pressure. Consider bull put spreads as vol cools and price stabilizes.XHB (Homebuilders) – RSI(2): 21.0 | IV Rank: 52.6

Rare alignment: oversold and high IV. Offers the best of both worlds—premium-selling + mean reversion.EFA (Developed Int’l) – RSI(2): 16.4

Short-term oversold with healthy IV. Bounce setups supported by bullish short put spreads.EEM (Emerging Markets) – RSI(2): 18.3 | IV Rank: 67.8

Oversold and volatile—ideal for short puts or defined-risk spreads that benefit from a snapback and elevated IV.

📌 Takeaway: These names show high emotional selling. When RSI is stretched across multiple periods, short puts and reversals offer strong edge—especially where IV supports premium-selling (XHB, EEM, XRT).

USO (Oil) – RSI(2): 90.8 | IV Rank: 9.5

Momentum is overcooked, but premium is too low. Best treated as a directional short if a reversal confirms—not ideal for selling options.XLE (Energy) – RSI(7): 68.4

Approaching overbought territory. Monitor for topping behavior, but IV isn’t high enough to justify premium selling yet.

📌 Takeaway: Fewer overbought setups this week. USO and XLE may pull back, but without sufficient IV, the premium-selling edge isn’t there.

3. VIX & Broad Market Volatility

VIX: 19.28

IV Rank: 36.9%

RSI(7): 36.8

Vol remains rangebound and in the “goldilocks zone” for premium sellers—not too high, not too low. But keep your eye on the horizon: a move above 21–22 could flip flows quickly and require more active hedging.

Some setups stand out for reasons outside the typical metrics:

IBIT (Bitcoin ETF) – IV Rank: 76

Volatility remains elevated while RSI is neutral. This is a prime setup for strangles or iron condors, especially for experienced traders comfortable with crypto exposure.GDX (Gold Miners) – RSI(7) + RSI(14) elevated, IV Rank: 18

A stealth momentum setup—vol is underpricing potential movement. Consider directional plays like call diagonals or debit spreads.XLU (Utilities) – IV Rank: 16, mixed RSI

Quiet sector, but low IV could set up trend-following or calendar spreads if RSI firms up.

Final Signals from The Implied Truth

💰 Premium-Selling Edge

→ XLB, XHB, XLF, XRT

📉 Mean Reversion Trades

→ SLV, XHB, XRT, EEM

🎯 Volatility Watchlist

→ IBIT, XLU, GDX

⚠️ Fades to Watch (But Not Yet Sell Premium)

→ USO, XLE

📊 Quick Reference: The Implied Truth Table

Symbol: ETF ticker (e.g., SPY, QQQ, IWM).

Last: Latest closing price.

P/C Ratio: Put/Call ratio—>1 = bearish, <1 = bullish; extremes can signal contrarian setups.

Impl Vol: Implied Volatility—higher IV = richer premiums, more expected movement.

IV Rank: IV vs. past year’s range—0% = lowest, 100% = highest; >35% favors premium-selling.

IV Percentile: % of time IV was below current level—adds context to IV Rank for volatility shifts.

RSI (2/7/14): Momentum indicator—>80 = overbought, <20 = oversold; shorter RSIs react faster.

High/Low Graph: Shows price vs. 52-week range—+% = near highs, -% = near lows.

Use this to spot volatility trends, premium opportunities, and momentum shifts at a glance. 🚀

📚 Educational Corner: Options Deep Dive

🎓 Topic of the Week: Why Most Options Traders Lose: The Discipline Gap, Not the Strategy

It’s not the strategy. It rarely is.

The majority of options traders don’t underperform because their system lacks edge — they underperform because they lack executional consistency. They abandon trades mid-flight, override their own rules, change sizing without logic, or stop trading entirely after a string of losses. Over time, this behavioral noise erodes what could have been a perfectly valid statistical edge.

Let’s be brutally honest: the options market is an unforgiving machine that rewards repetition and punishes emotional improvisation.

The Real Reason: Discipline Deviation

If you’re selling premium with defined-risk trades like iron condors or vertical spreads, you’re not trying to be “right” — you’re trying to stay within a probabilistic framework. Your setup might have a 70%+ chance of success, based on 15-20 delta short strikes, appropriate IV conditions, and a 45-day time frame. If executed consistently, it’s a strategy designed to grind out small wins and controlled losses across hundreds of occurrences.

But this edge lives only in the aggregate.

And yet, this is where most traders derail: they don’t place enough occurrences to let probabilities materialize. Or they selectively trade the setup only when it “feels safe.” Or worse, they override rules after a win or loss, introducing subjective noise into what should be a systematic process.

This is the discipline gap — the chasm between what traders say they do, and what they actually do.

They’ll claim to run a 45 DTE system with disciplined exits and fixed 2% allocation, but under the hood, the process looks more like this:

Skip trades when the market is choppy (missing the edge)

Exit early due to fear (cutting profits short)

Hold losers into expiration hoping for a miracle (amplifying drawdowns)

Increase size after wins, decrease after losses (breaking risk symmetry)

Constantly tweak setups without enough data to justify changes

None of these behaviors are part of the strategy. But they become the strategy — one rooted in randomness rather than discipline. And randomness doesn’t compound.

What Discipline Really Means in Options Trading

Discipline in trading isn’t about rigidity or moral superiority. It’s about removing unnecessary variance from your execution. When you sell options, you're playing the role of the house — and the house doesn’t win by changing rules mid-hand. It wins by letting edge play out over time.

Let’s go deeper.

Discipline means trading when you don’t feel like it.

Not every day. Not compulsively. But when your system gives a signal — even if the headlines are loud, even if volatility spiked yesterday — you take the trade. Otherwise, you introduce selective bias into a non-directional framework that depends on statistical consistency.

Discipline means holding when it’s uncomfortable.

This doesn’t mean holding through major breaches in your plan. It means holding when a trade is simply noisy or hasn’t moved yet. Most traders exit early out of fear, robbing the strategy of its expected value. A disciplined exit requires time — it can’t be forced. You must trust the math, not your pulse.

Discipline means adjusting when you don’t want to.

It’s easy to ignore a position that’s gone against you. It’s harder to act — to roll, to hedge, or to take a loss as defined. But discipline demands action before pain becomes catastrophic. Adjustment isn’t rescue; it’s risk control. And control must be executed unemotionally.

Discipline means keeping size constant.

The moment you change trade size based on emotional outcomes (revenge trading after a loss, pressing after a win), you destroy your expectancy. Every edge is tied to size symmetry — trade small, trade often. Stay within your capacity to be indifferent to outcomes.

The Anatomy of Consistent Execution

What separates professionals from hobbyists is consistency of process. Here’s what world-class discipline actually looks like in the trenches:

Pre-trade rules are checklist-based, not intuitive. (Example: “I only sell premium in underlyings with IV Rank > 30 and open interest > 500 at both strikes.”)

Sizing is fixed as a % of capital — never based on feel. (Example: “No more than 2% to 5% of portfolio notional per position.”)

Exits are mechanical, not mood-based. (Example: “I exit at 50% of max profit or 2x credit loss.”)

Adjustments are pre-defined, not improvisational. (Example: “If tested side breaches short strike, roll entire position out in time and widen wings.”)

Reviews are objective, not emotional. (Weekly trade journal review of what rules were followed or broken — with corrective notes.)

This isn’t perfection. This is process. And process, when repeated consistently, is what gives traders an edge over time.

Why Strategy Alone Is Not Enough

You can backtest a strategy to the moon. You can optimize the Greeks, fine-tune your deltas, and map the perfect volatility surface. But the reality is this:

Any statistically sound options strategy is only as effective as the trader’s ability to execute it without deviation.

You don’t need to reinvent your strategy every few weeks. You need to execute one high-probability system with unwavering consistency across hundreds of trades. That’s where the edge lives. Not in discovering the next hot setup — but in refusing to sabotage the one you already have.

The Fix: Create a Process That Shields You From Yourself

To close the discipline gap, you must remove discretion wherever possible. You don’t fix inconsistency by becoming smarter or more “tactical.” You fix it by creating friction between you and your impulses.

Here’s a simple but powerful framework:

Build a written strategy doc. Define entry criteria, preferred underlyings, IV conditions, delta ranges, time frames, max number of trades, sizing rules, exits, and adjustments.

Turn that document into a checklist. Don’t just write it — use it every time before placing a trade.

Use automation or alerts for rebalancing and exits. Don’t rely on memory. Set reminders or conditional orders when possible.

Journal trades weekly with a binary “Did I follow plan?” question. If the answer is no, make a note. If the answer is repeatedly no, reduce size or stop trading until corrected.

Measure performance only after 50+ trades. Don’t evaluate based on a week or a month. Options trading edge only reveals itself over large sample sizes.

Final Thought: It’s Not the Setup — It’s You

The market doesn’t punish you for having a mediocre strategy. It punishes you for having an inconsistent one.

So before you throw out your system, switch from condors to butterflies, or abandon premium selling altogether — ask yourself: have I truly executed the process, every time, without deviation?

If the answer is no, don’t scrap the strategy. Scrap the inconsistency.

The discipline gap is where most traders fail.

It’s also where you gain the most edge.

🔗 Let’s Stay Connected

Have questions, feedback, or just want to say hello? I’d love to hear from you.

📩 Email me anytime at [email protected]

Thanks again for reading. I hope you found today’s insights valuable and worth your time.

Trade Smart. Trade Thoughtfully.

Andy Crowder

Founder | Editor-in-Chief | Chief Options Strategist

The Option Premium

Reply