- The Option Premium

- Posts

- March Madness and Options Trading: The Statistical Edge Every Trader Needs

March Madness and Options Trading: The Statistical Edge Every Trader Needs

Delta is your pre-game win probability. Theta is the clock that pays you. Gamma is the buzzer-beater risk. Learn the four Greeks through the March Madness framework with real SPY trade examples.

March Madness and Options Trading: The Statistical Edge That Separates Professionals from Gamblers

Every March, millions of fans fill out NCAA Tournament brackets hoping to predict the unpredictable. Some rely on team loyalty. Others go with gut feelings. But the people who consistently finish near the top of their bracket pools do something different: they analyze statistics, historical trends, and probabilities to tilt the odds in their favor before the first tip-off.

The parallels to options trading are almost too clean. Too many traders approach the market the way a casual fan fills out a bracket, making decisions based on hunches, headlines, and hope. The professionals, the traders who compound capital year after year, do the opposite. They understand that every option contract is a probability statement, that time decay is a structural advantage, and that the Greeks aren't abstract math. They're the playbook.

This article breaks down the core concepts that give professional premium sellers their edge, using the tournament framework to make each one concrete. If you've ever struggled to understand delta, gamma, theta, or why selling premium works, this is the piece that makes it click.

Delta: The Pre-Game Win Probability

Before every tournament game, analysts assign a win probability to each team. A No. 1 seed facing a No. 16 seed might be given a 97% chance of winning. A 5-vs-12 matchup might sit at 80/20. These probabilities aren't guarantees. They're the market's best estimate of the likely outcome given everything that's known.

Delta works the same way. It represents the approximate probability that an option will expire in-the-money. A call option with a 0.80 delta has roughly an 80% chance of finishing above its strike price at expiration. A put option with a 0.20 delta has roughly a 20% chance of finishing in-the-money, meaning there's an 80% probability it expires worthless, which is exactly what the seller wants.

Here's where the analogy gets practical. Consider a tournament matchup between the Oregon Ducks (No. 5 seed) and the Liberty Flames (No. 12 seed). Analysts give Oregon an 80% win probability, similar to a 0.80 delta option. Liberty's 20% chance mirrors a 0.20 delta. If you're a premium seller, you're not buying lottery tickets on the Flames. You're selling insurance to the people who are, collecting premium on the high-probability side of the trade.

The real-world application. When you sell a credit spread with a short strike at the 0.15 delta, you're placing a trade with roughly an 85% probability of profit. On a $5 wide SPY put spread with 35 DTE, that might look like selling the $540/$535 put spread for $0.85 credit. Your max risk is $4.15. Your probability of keeping that $0.85? Approximately 85%. Over 50 trades, the math works. Not on every individual trade, but across the full season, just like a bracketologist who picks the higher seed 85% of the time won't win every game but will finish well ahead of the field.

Delta also tells you how much an option's price moves relative to the underlying. A 0.80 delta call gains approximately $0.80 for every $1 the stock rises. A 0.20 delta call gains only $0.20. For premium sellers, lower-delta short strikes (0.10 to 0.20 range) provide the best combination of high probability and manageable directional exposure. You're selling the deep underdog tickets, collecting premium from the speculators who want them.

Delta translates directly to win probability. An 80% tournament favorite is a 0.80 delta option. A 20% underdog is 0.20. Premium sellers operate at 0.15-0.20 delta (85% probability of profit), selling insurance to speculators on the other side. The real trade: a $5 wide SPY put spread at the 0.15 delta short strike collects $0.85 on $4.15 max risk with roughly 85% POP. Over 50 trades, the math works. Not on every individual trade, but across the full season.

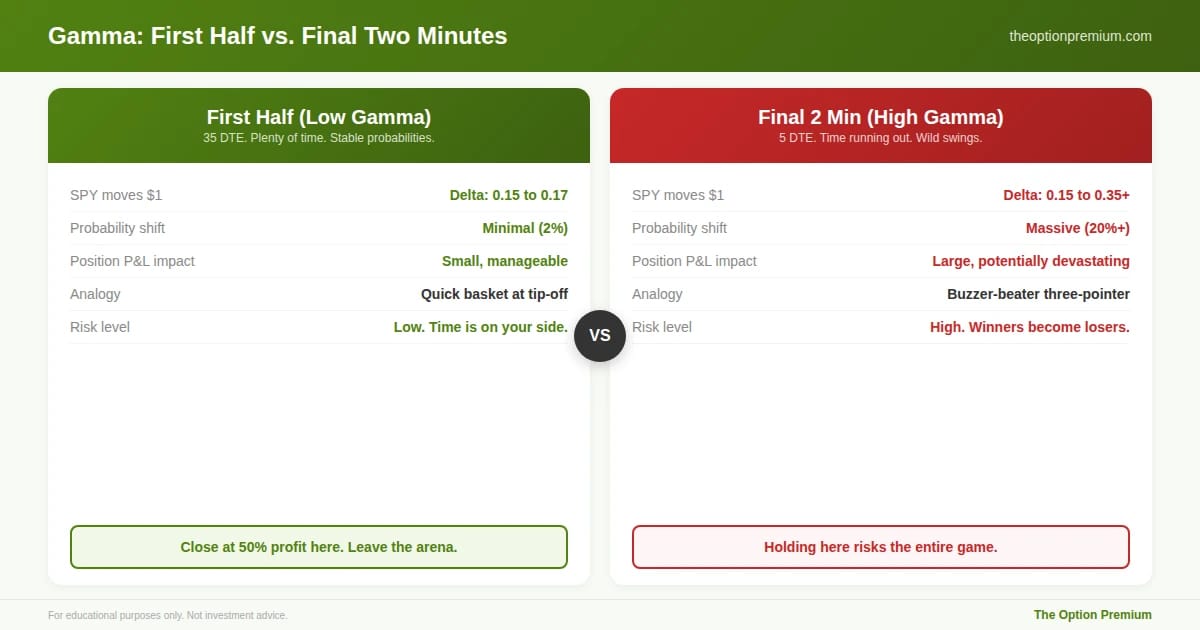

Gamma: The Momentum Shift

In basketball, momentum is real but fleeting. A team can start the second half on a 12-0 run and completely change the complexion of the game. What was an 80/20 probability at halftime becomes 60/40 or even 50/50. The speed of that probability change is what makes late-game basketball so intense.

Gamma is the options equivalent. It measures how quickly delta changes as the underlying stock moves. Early in a game (or early in an option's life), small events don't change the probabilities much. A quick basket at the opening tip barely moves the needle. But in the final two minutes, a single three-pointer can swing the win probability by 20 points.

Low gamma (early in the option's life). A stock moves $1, and the delta of your 0.15 delta option barely changes. Maybe it goes to 0.16 or 0.17. The probability shift is minimal. This is the equivalent of first-half basketball, where the score matters but the outcome is still distant.

High gamma (near expiration). The same $1 stock move might swing your delta from 0.15 to 0.35 or even higher. Suddenly your "safe" out-of-the-money option is being tested. This is the final two minutes of a close game, where every possession changes the probability dramatically.

Why gamma matters for premium sellers. If you sell options and hold them into the final week before expiration, you're playing in the high-gamma zone. Small moves in the stock create large swings in your position's value. This is why experienced premium sellers close trades at 50% of max profit well before expiration. You're leaving the arena before the final buzzer, locking in your win while the probability still favors you. Staying until the final seconds exposes you to the wild probability swings that gamma creates, the same way a tournament favorite can lose on a half-court buzzer beater despite dominating for 38 minutes.

A real example. You sell a $5 wide SPY iron condor at 35 DTE and collect $1.80. At 18 DTE, the position is worth $0.90 (50% of max profit). Gamma is still moderate. You close for $0.90 profit on $3.20 risk (28.1% ROC). If instead you hold to 5 DTE hoping to squeeze out the last $0.90, gamma has tripled. A single 1.5% SPY move could turn your winner into a loser overnight. The extra $0.90 in potential profit isn't worth the gamma risk. Close the trade, take the win, move to the next game.

Gamma is the speed of probability change. At 35 DTE (first half), a $1 SPY move barely shifts your delta from 0.15 to 0.17. Manageable, like a quick basket at the opening tip. At 5 DTE (final two minutes), the same $1 move can swing delta from 0.15 to 0.35 or higher, potentially turning a winner into a loser overnight. This is the buzzer-beater three-pointer. Close at 50% of max profit well before the high-gamma zone. Leave the arena with the win. Don't risk it in garbage time.

Theta: The Clock That Pays You

Every tournament game has a 40-minute clock. Once it starts, time only moves in one direction. The team that's winning benefits from every tick. The team that's losing watches its window for a comeback shrink with each passing second.

Theta is the options clock, and it pays the seller. Theta measures the rate at which an option loses value each day, all else being equal. When you sell an option, time decay works in your favor from the moment the trade is opened. Every day that passes, the option you sold becomes a little cheaper, which is profit for you.

The theta curve is not linear. In the first half of an option's life (say, 60 to 30 DTE), theta decay is gradual. The option loses value slowly. But as expiration approaches, theta accelerates dramatically. An option that decays $0.02 per day at 45 DTE might decay $0.08 per day at 10 DTE. This is why the 30-60 DTE entry window is the sweet spot for premium sellers. You're entering the trade just as theta begins to accelerate, capturing the steepest part of the decay curve without the gamma risks that come with holding too close to expiration.

Think of it this way. If you're the tournament favorite leading by 10 points, the clock is your best friend. Every minute that ticks off makes it harder for the underdog to come back. Theta works identically. Once you've sold premium and the stock stays within your expected range, time decay erodes the option's value day by day. You don't need the stock to move in your direction. You just need it to not move too far against you, and time does the rest.

A concrete example. You sell a bull put spread on SPY for $1.10 at 35 DTE. Over the first 15 days, the spread decays to $0.75 (a $0.35 gain). Over the next 10 days, it decays to $0.45 (another $0.30 gain). The acceleration is clear. By day 25, you've captured 59% of the max profit and can close the trade with 10 days still remaining. The clock paid you. Gamma never got the chance to hurt you.

Theta is the game clock, and it pays premium sellers every day. This real example shows a $1.10 SPY bull put spread decaying in three phases. Days 1-15: slow, steady decay earns $0.35 (like building a first-half lead). Days 15-25: theta accelerates, earning another $0.30 as the clock runs faster. Day 25: close with $0.65 of $1.10 captured (59% of max profit). You've won the game with 10 days still on the clock. The remaining $0.45 isn't worth the gamma risk of playing to the final buzzer.

Before a high-profile tournament matchup, there's uncertainty. Will the star player's ankle hold up? Will the zone defense work? That uncertainty drives interest, viewership, and in the options world, premium.

Vega measures an option's sensitivity to changes in implied volatility. When uncertainty is high (elevated IV), options are more expensive because the market is pricing in larger potential moves. When uncertainty is low, options are cheaper.

For premium sellers, elevated IV is the equivalent of rich tournament betting odds. When IV Percentile is above 50% (meaning current IV is higher than 50% of its historical readings), the premiums available on credit spreads and iron condors are meaningfully richer. You're collecting more income for the same probability trade. This is why premium sellers scan for elevated IV before entering trades. It's the equivalent of finding a tournament matchup where the point spread seems too generous.

A real comparison. SPY credit spread at 0.15 delta, 35 DTE, $5 wide. When VIX is at 14 (low IV): credit of $0.80, ROC of 19%. When VIX is at 28 (high IV): credit of $1.80, ROC of 56.3%. Same delta. Same strike width. Same DTE. The elevated uncertainty doubled the premium available. After the uncertainty resolves (earnings pass, the Fed speaks, the geopolitical headline fades), IV contracts and the option you sold loses value rapidly. This is the vega tailwind that premium sellers ride.

The Professional's Playbook: Putting the Greeks Together

A tournament coach doesn't rely on a single statistic. Points per game, defensive efficiency, turnover rate, and free throw percentage all factor into the game plan. The best options traders use the Greeks the same way, as an integrated system, not isolated numbers.

The entry checklist. Before every trade, check all four: delta (is the probability in my favor at 0.10-0.20 for short strikes?), theta (am I in the 30-60 DTE sweet spot where decay accelerates?), vega (is IV Percentile above 50% so premiums are rich?), and gamma (am I giving myself enough time before expiration to avoid the high-gamma danger zone?). When all four align, you have a trade with structural edge, the options equivalent of a No. 2 seed with elite defense, strong free-throw shooting, and a favorable matchup.

Position sizing is the roster depth. Even the best team loses games. The best strategy loses trades. The 2% rule (risking no more than 2-3% of your account per trade) ensures that a single loss is a footnote, not a season-ending injury. Over 50 trades at 80% win rate, the math works. But only if no single loss can take you out of the tournament.

Close winners early. Take profits at 50% of max profit. This is the equivalent of pulling your starters when you have a comfortable lead in the second half. You've won. The remaining minutes (remaining premium) aren't worth the injury risk (gamma risk). Reset and play the next game.

All four Greeks must align before entry. Delta (is probability in my favor?): short strikes at 0.10-0.20 for 80-90% POP, like picking the higher seed across 50 games. Theta (am I in the decay sweet spot?): 30-60 DTE entry, where every day that passes is like a minute ticking off the clock when you're ahead. Vega (are premiums rich enough?): IVP above 50% means the same trade pays 2x more, like finding a matchup where the point spread is too generous. Gamma (am I avoiding the danger zone?): close at 50% profit before the high-gamma final week, like pulling starters when the game is in hand. When all four align, you have structural edge.

Risk Reality Check

The March Madness analogy is useful, but it has a limit. In a bracket pool, a single upset costs you one pick. In options trading, a single oversized position that moves against you can cost real capital that takes months to recover.

The statistics favor premium sellers over hundreds of trades. A 70-85% win rate with proper position sizing, defined risk, and disciplined profit-taking is a genuinely positive expected value approach. But it requires treating every trade as one game in a long season, not as the championship. No single trade matters. The aggregate result across 50, 100, 200 trades is what builds the account. That's the statistical edge. Not any one trade, but the relentless application of probability over time.

Key Takeaways

Delta is your pre-game win probability. A 0.15 delta short strike has roughly an 85% chance of expiring worthless. Premium sellers operate in the 0.10-0.20 delta range, selling insurance to speculators while keeping the probability firmly in their favor. Over a full season of trades, the win rate compounds.

Gamma is the momentum shift that accelerates near expiration. Small stock moves create large delta changes in the final days, turning winners into losers overnight. Close trades at 50% of max profit well before expiration to avoid the high-gamma danger zone, just as a coach pulls starters when the game is in hand.

Theta is the clock that pays premium sellers every day. The 30-60 DTE entry window captures the steepest part of the decay curve. You don't need the stock to move in your direction. You need it to stay within range while time erodes the option's value.

Vega rewards patience during uncertainty. Elevated IV (IV Percentile above 50%) means richer premiums for the same probability trade. Enter when premiums are rich, and let the vega contraction after the uncertainty resolves accelerate your profits. The same delta and DTE can produce 2x the ROC in a high-IV environment.

The integrated approach is the real edge: check delta, theta, vega, and gamma before every entry. Size at 2-3% max risk. Close at 50% profit. Repeat across 50+ trades per year. No single trade is the championship. The aggregate result across the full season is what builds lasting wealth.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply