- The Option Premium

- Posts

- Put Options Explained: Downside Protection and Income Generation

Put Options Explained: Downside Protection and Income Generation

Learn both sides of put options: buying puts for portfolio protection and bearish leverage, and selling puts to generate income on stocks you want to own. Step-by-step examples for both strategies.

Andrew Crowder

March 07, 2026

Put Options Explained: Downside Protection and Income Generation

Put options are the most misunderstood contract in options trading. Most beginners encounter puts as a bearish bet, a way to profit when stocks fall. That's true, but it's only half the story. On the other side of every put purchase is a seller collecting premium, and it's that selling side where puts become one of the most powerful income-generating tools available to retail traders.

This guide covers both sides of the put option because understanding both is essential. Whether you're buying puts to protect a portfolio or selling them to generate income on stocks you want to own, knowing when each approach fits will shape your entire options trading framework.

What Is a Put Option?

A put option is a contract that gives the buyer the right to sell 100 shares of a stock at a specific price before a specific date. The buyer pays a premium for that right. The seller collects the premium and takes on the obligation to buy 100 shares at the strike price if the buyer exercises.

Four components define every put. The underlying stock is what the contract is based on. The strike price is the price at which the buyer can sell shares. The expiration date is when the contract expires. And the premium is the price of the contract, driven by intrinsic value, time value, and implied volatility.

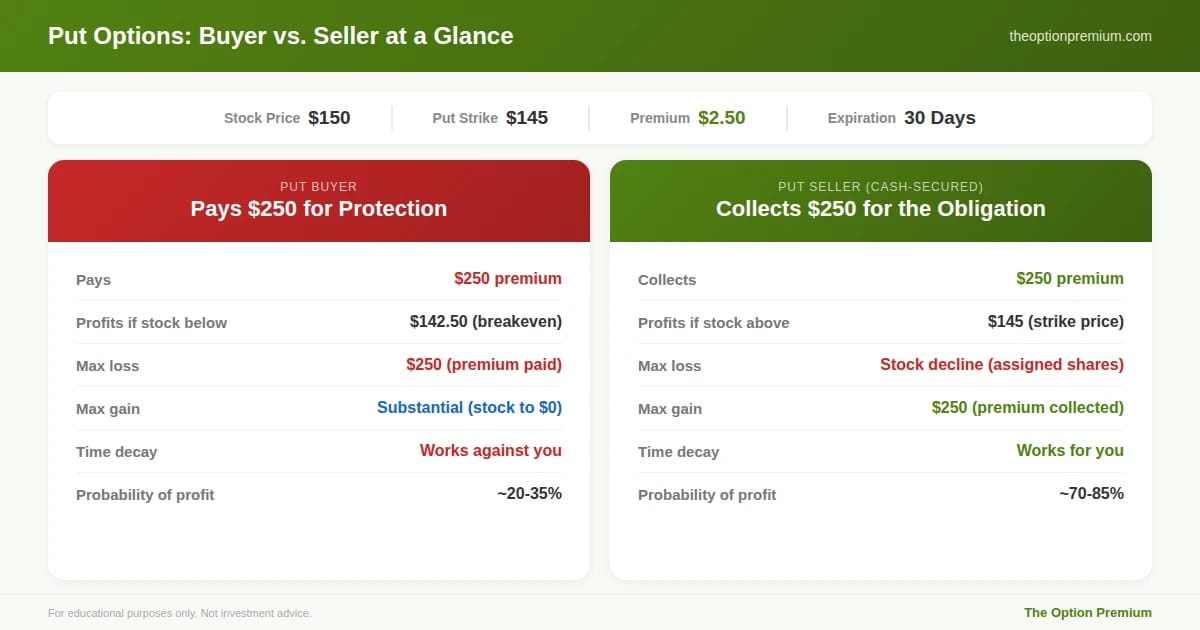

Here's a grounding example. A stock trades at $150. You're looking at a $145 put expiring in 30 days, priced at $2.50. The buyer pays $250 for the right to sell 100 shares at $145 anytime before expiration. The seller collects $250 and agrees to buy 100 shares at $145 if assigned.

If the stock drops to $130, that $145 put is now worth at least $15 in intrinsic value. The buyer profits significantly. If the stock stays above $145, the put expires worthless. The buyer loses the $250 premium. The seller keeps it.

Same contract. One side is paying for protection. The other side is getting paid to provide it.

Same contract, two completely different strategies. The put buyer pays $250 for protection or bearish leverage (20-35% probability of profit). The put seller collects $250 for taking on the obligation (70-85% probability of profit). Time decay works against the buyer and for the seller every day.

Buying Puts: Portfolio Insurance

When you buy a put, you're either making a directional bet that the stock will fall or purchasing insurance against a decline in shares you already own. Your risk is limited to the premium paid. Your profit potential is substantial (the stock can fall all the way to zero, though that's the theoretical extreme).

How buying puts works in practice. You buy the $145 put for $2.50. Your total cost is $250. Your breakeven at expiration is $142.50 (the $145 strike minus the $2.50 premium). Below $142.50, every dollar the stock drops adds $100 to your profit. At $130, your profit is $1,250. At $120, it's $2,250.

The protective put (married put). This is the most practical use of buying puts for most investors. You own 100 shares at $150 and buy a $145 put for $2.50. Your maximum loss is now capped at $7.50 per share ($5 to the strike plus the $2.50 premium cost), or $750 total, regardless of how far the stock falls. You've bought a floor under your position. The trade-off is the $250 cost, which is essentially an insurance premium.

When buying puts makes sense:

Portfolio protection during uncertainty. Major market events, geopolitical risk, or periods where you want to stay invested but limit your downside. A put on SPY or QQQ can hedge an entire equity portfolio.

Protecting gains on a winning position. You own a stock that's run up significantly. Instead of selling and triggering capital gains, you buy a put to lock in a minimum exit price. If the stock keeps rising, you participate. If it reverses, your put limits the damage.

Bearish conviction with defined risk. You believe a specific stock will decline, but you don't want to short shares (which carries unlimited risk). Buying a put limits your loss to the premium paid while giving you substantial downside profit potential.

Earnings or event protection. You hold a stock through earnings and want to protect against a gap down. A put expiring just after the earnings date acts as a temporary insurance policy.

Selling Puts: The Income Engine

Selling puts is where the equation flips entirely. Instead of paying for protection, you become the one providing it, and you get paid for that service. This is the foundation of premium selling and the entry point of the Wheel Strategy.

A cash-secured put means you sell a put option while holding enough cash to buy 100 shares if assigned. You collect premium upfront in exchange for agreeing to purchase the stock at the strike price if it falls below that level.

How selling puts works in practice. You like a stock trading at $150 and would be comfortable buying it at $140. You sell the $140 put expiring in 30 days for $2.00. You collect $200 immediately and set aside $14,000 in cash as collateral.

Three outcomes play out. Stock stays above $140: the put expires worthless, you keep $200, and your $14,000 is released. That's 1.43% in 30 days on committed capital. Stock drops to $137: you're assigned 100 shares at $140, but your effective cost basis is $138 ($140 minus the $2 premium). You own a stock you wanted at a discount. Stock drops to $120: you're assigned at $140 with a $138 cost basis while the stock trades at $120. The premium helped, but a significant decline still hurts. This is why stock selection is the most important variable.

Two sides of the same contract. The protective put buyer creates a floor under an existing position, capping max loss at $7.50 per share ($750 total) regardless of how far the stock falls, for a $250 insurance cost. The cash-secured put seller collects $200 with roughly an 80% chance of keeping the full premium. If assigned, the effective cost basis is $138.

When selling puts makes sense:

You want to own the stock at a lower price. Think of it as getting paid to place a limit order. If the stock drops to your price, you buy at a discount. If it doesn't, you keep the income and try again.

Income generation on idle cash. Cash sitting in your account earns minimal interest. Selling puts against stocks you'd be willing to own puts that capital to work. The premiums you collect often exceed money market or bond yields significantly.

Elevated implied volatility. When IV Rank is above 30, put premiums are richer because the market is pricing in larger expected moves. Selling into elevated IV means more income for the same probability profile.

Probability-driven income. A 0.20 delta put has roughly an 80% chance of expiring worthless. Over time, selling puts at this delta range produces consistent income. You won't win every trade, but the probability math favors the seller across dozens of occurrences.

As the first phase of the Wheel. Selling puts is how you enter the Wheel Strategy . If assigned, you transition to selling covered calls against the shares, creating a continuous income cycle.

Buy puts when you need protection on existing positions, want to lock in gains without selling, have bearish conviction with defined risk, or need event hedging. Sell puts when you want to own a stock at a lower price, generate income on idle cash, IV is elevated (IVR above 30), or as the entry phase of the Wheel Strategy.

The Side-by-Side Comparison

The differences between buying and selling puts come down to what you're paying for versus what you're being paid for.

Who pays and who collects. The buyer pays premium for protection or bearish exposure. The seller collects premium for taking on the obligation to buy shares. Every dollar the buyer spends is a dollar the seller earns.

Time decay. Theta erodes the buyer's position every day. A $2.50 put today might be worth $2.00 in a week even if the stock hasn't moved. For the seller, that same erosion is income. Time is the buyer's cost of insurance and the seller's source of profit.

Probability profile. Buying an OTM put has a low probability of profit, often 20-35%, because you need the stock to drop significantly. Selling an OTM put has a high probability of profit, typically 70-85%, because you only need the stock to stay above the strike. The buyer bets on the unlikely. The seller bets on the likely.

Risk and reward. The buyer's maximum loss is the premium paid. The potential gain is substantial (stock can drop to zero). The seller's maximum gain is the premium collected. The risk is being assigned shares at the strike price during a decline, potentially a meaningful loss if the stock drops sharply.

Role in a portfolio. Buying puts serves a defensive role, protecting capital during downturns. Selling puts serves an offensive role, generating income and acquiring shares at favorable prices. Both are legitimate, but they serve fundamentally different purposes.

The Practitioner Edge: How I Use Puts

My approach to puts mirrors the broader premium selling philosophy that drives everything I do.

90% of my put activity is selling. Cash-secured puts on stocks I'd be happy to own, put spreads as the lower half of iron condors, and credit spreads for defined-risk income. The probability edge, combined with the volatility risk premium (implied volatility overestimates actual moves 80-85% of the time), makes selling the more consistent long-term approach.

The other 10% is buying. Protective puts on concentrated stock positions during periods of elevated risk, and long puts as the protective wings in credit spreads. I view these as insurance costs, a necessary expense to cap worst-case scenarios, not as profit centers.

My standard put-selling setup. I target 0.15-0.25 delta strikes at 30-45 DTE on stocks that pass my ownership test (would I hold 100 shares for three to six months at this price?). I close at 50-75% of maximum profit and evaluate at 200% of premium collected on the loss side. Position sizing: no single position over 25% of account capital, always maintaining a 20% cash reserve.

Common Mistakes With Put Options

Buying puts as a directional gamble. Buying puts on a stock just because it "feels expensive" is speculation, not strategy. Stocks can stay overvalued for months or years. Without a specific catalyst and timeframe, bought puts bleed value through theta decay until they expire worthless.

Selling puts on stocks you wouldn't own. The biggest mistake in put selling. High premium on a weak stock isn't income. It's compensation for risk the market is telling you is real. If you wouldn't hold 100 shares at the strike price for three to six months, don't sell the put. Period.

Buying too little time. Protective puts with 7-14 days to expiration are cheap for a reason. They expire before most risks materialize. For portfolio protection, buy puts with at least 45-90 DTE to give the insurance time to work.

Selling puts with no exit plan. "I'll just take assignment" is not a management plan. Know your profit target (50-75% of max profit), your loss evaluation point (200% of premium collected), and when you'll roll versus accept assignment. Define these before entry, not during a drawdown.

Over-hedging with protective puts. Buying puts on every position in your portfolio turns insurance into an expense that drags performance. Hedge selectively: protect your largest or most concentrated positions, or use a single broad-market put (SPY, QQQ) to hedge the overall portfolio rather than individual names.

Risk Reality Check

Buying puts: your maximum loss is 100% of the premium. Protective puts that expire worthless are not wasted money any more than car insurance you never used was wasted. The cost is the price of certainty. But buying puts consistently as directional bets without a disciplined framework will drain your account through theta decay.

Selling puts: the stock can drop significantly below your strike. Your maximum loss on a cash-secured put is the strike price times 100 minus the premium collected. In a severe market selloff, multiple puts can be tested simultaneously, which is why position sizing and cash reserves matter more than any individual trade's probability.

The responsible approach: size positions so that no single trade can materially damage your account. Buying puts for protection? Allocate 1-3% of your portfolio annually to hedging costs. Selling puts for income? Max 25% of account per position, 20% cash reserve, and never more positions than you can handle being assigned on simultaneously.

Key Takeaways

A put option gives the buyer the right to sell 100 shares at the strike price. Buyers pay premium for downside protection or bearish leverage. Sellers collect premium by taking on the obligation to buy shares. Same contract, two fundamentally different uses.

Buy puts for portfolio protection (protective puts on existing shares), bearish conviction with defined risk, or event hedging. Give yourself at least 45-90 DTE for protective puts and hedge selectively rather than everything.

Sell puts when you want to own the stock at a lower price, generate income on idle cash, and IV is elevated. Target 0.15-0.25 delta, 30-45 DTE, and only sell on stocks you'd be happy to own for three to six months.

Time decay is the dividing line. It costs the buyer money every day and pays the seller every day. This is why the selling side produces more consistent long-term results, and why 90% of my put activity is selling.

Stock selection is the most important variable in put selling. High premium on a bad stock isn't income. It's the market warning you that risk is real. Pass the ownership test first, then sell the put.

Protection and income aren't opposites. They're two sides of the same contract. Knowing which side to be on, and when, is what turns puts from a confusing concept into your most versatile tool.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply