- The Option Premium

- Posts

- The Trillion Dollar Equation Behind Every Winning Trade

The Trillion Dollar Equation Behind Every Winning Trade

The Black-Scholes model prices options using one guess: future volatility. That guess is systematically too high. The 3-5 percentage point gap between implied and realized volatility is the premium seller's edge. Six steps to capture it.

Andrew Crowder

April 30, 2026

The Trillion Dollar Equation Behind Every Winning Trade

In 1973, two economists published a paper that changed finance permanently. Fischer Black and Myron Scholes, with critical contributions from Robert Merton, solved a problem that had defeated mathematicians for decades: how to price an option. Their solution, the Black-Scholes model, didn't just earn a Nobel Prize. It created the modern options market. Every option price you see on your screen, every credit you collect on a credit spread, every premium you sell on an iron condor, is derived from this equation or one of its descendants.

The options market now represents trillions of dollars in notional value. The equation that prices it all fits on a single line.

But here's what matters for you and me, the premium sellers who use this equation every single day without thinking about it: the Black-Scholes model contains a built-in assumption that is systematically wrong. Not occasionally wrong. Not randomly wrong. Systematically wrong in a direction that creates a persistent, measurable, and exploitable edge for anyone who sells options for a living.

That assumption is where your edge lives. Understanding it doesn't require a PhD in mathematics. It requires understanding one input, one gap, and one behavioral reality about how markets price fear. This article breaks down the equation, isolates the alpha, and shows you the exact steps to use it in your own trading.

The Equation in Plain English

The Black-Scholes formula looks intimidating on paper. It involves natural logarithms, cumulative distribution functions, and the kind of Greek letters that make most people's eyes glaze over. But the core logic is remarkably simple.

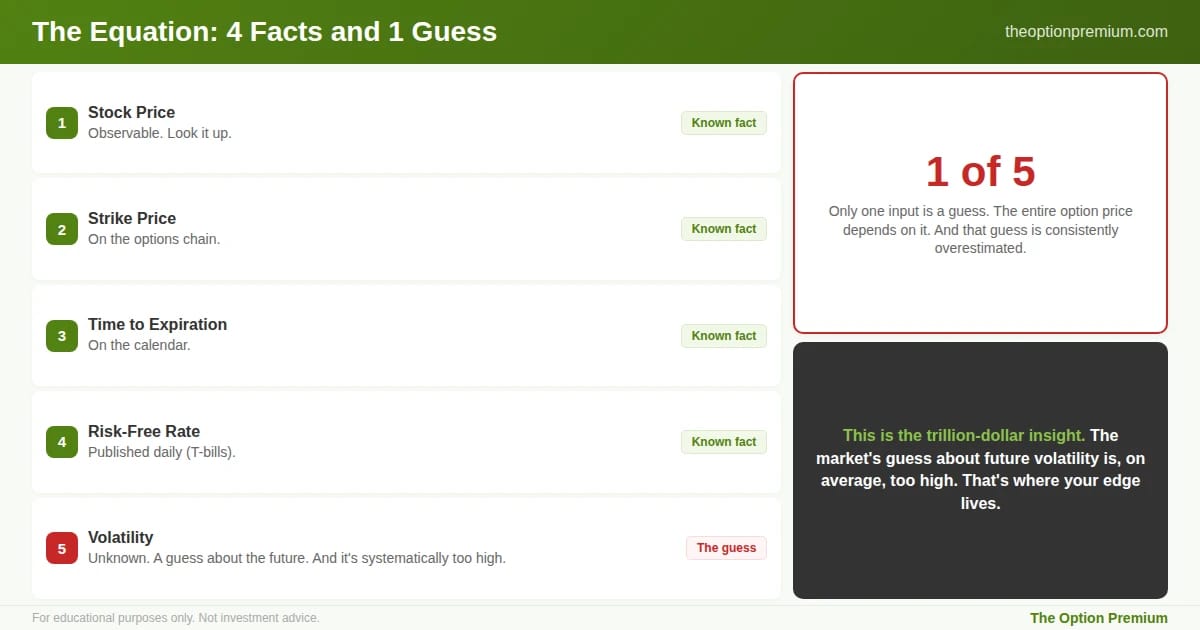

An option's price is determined by five inputs: the stock price, the strike price, the time to expiration, the risk-free interest rate, and the volatility of the underlying stock.

Four of those inputs are observable. You can look up the stock price. The strike price is on the chain. The time to expiration is on the calendar. The risk-free rate is published daily. You don't need a model to find them. They're facts.

The fifth input, volatility, is not observable. Nobody knows how volatile a stock will be over the next 30 or 45 days. The future hasn't happened yet. So the Black-Scholes model requires you to estimate future volatility and plug it in.

This is the single most important thing to understand about options pricing: four of the five inputs are known. The fifth is a guess. And the entire price of the option depends heavily on how good that guess is.

When you look at an option's price on your platform and back-solve for the volatility input that would produce that price, you get implied volatility. Implied volatility is the market's collective guess about how much the stock will move between now and expiration. It's not what the stock has done. It's not what any single analyst predicts. It's the consensus forecast embedded in the option's price by every buyer and seller in the market.

And here's the trillion-dollar insight: that consensus forecast is, on average, too high.

The equation has five inputs. Four are observable facts you can look up. The fifth, volatility, is a guess about the future. The entire option price depends heavily on this guess. And the market's guess is, on average, too high. Implied volatility consistently overestimates the actual movement of the underlying. This systematic overestimation is not a flaw in the market. It's a structural feature: option buyers are purchasing insurance and are willing to overpay. That overpayment is the premium seller's edge.

This is not theory. This is one of the most well-documented phenomena in financial markets.

Implied volatility consistently overestimates the actual movement of the underlying stock. Study after study, decade after decade, across equity indices, individual stocks, commodities, and currencies, the options market charges more for volatility than the underlying delivers. The difference between what the market charges (implied volatility) and what actually happens (realized volatility) is called the volatility risk premium, or VRP.

Why does this exist? Because of a fundamental asymmetry in the options market.

Option buyers are purchasing insurance. When a portfolio manager buys puts to protect a $500 million equity portfolio against a crash, they're not making a probabilistic bet. They're paying for peace of mind. They're paying to sleep at night. They're paying to keep their job if the market drops 20%. Insurance buyers are willing to overpay because the cost of being unprotected is catastrophic. The put premium is a line item in their risk budget, and they'll pay above fair value for it every single quarter.

Option sellers are providing that insurance. When you sell a credit spread or an iron condor, you're the underwriter. You're taking on the risk that the insurance buyer wants to offload. And because insurance buyers consistently overpay, insurance sellers consistently collect more premium than the risk justifies.

This is not a market inefficiency in the academic sense. It's a structural feature. The volatility risk premium exists because the buyers of options have a genuine, rational need to overpay. Their incentives are different from yours. A portfolio manager's career risk from being unhedged is not symmetric with the cost of the hedge. So they overpay. And that overpayment flows directly into the pockets of premium sellers who understand the equation well enough to stand on the other side.

The Numbers: How Big Is the Edge?

Let me put concrete numbers on this so you can see what the volatility risk premium actually looks like in practice.

Over the past two decades, the S&P 500's average implied volatility (as measured by the VIX) has been approximately 19-20%. The average realized volatility over the same period has been approximately 15-16%. That's a persistent gap of 3 to 5 percentage points.

In practical terms: the options market has been pricing in roughly 20-25% more movement than the stock market actually delivers. Year after year. Decade after decade. Through bull markets, bear markets, crashes, and recoveries. The gap narrows during extreme events (when realized volatility catches up to or briefly exceeds implied) and widens during calm periods. But the long-term average is clear and persistent.

This is your edge. When you sell a credit spread on SPY at 20% IV and the stock only delivers 16% realized volatility, the excess premium you collected, the 4 percentage points of volatility that never materialized, is profit. You sold volatility at $20 and it was worth $16. The $4 difference is the volatility risk premium captured.

Over hundreds of trades, across years of consistent selling, this gap compounds into the systematic edge that makes premium selling a viable long-term strategy. It's not about being right on direction. It's not about predicting where the stock will be. It's about selling something for more than it's worth, consistently, because the market structurally overprices it.

The volatility risk premium quantified. Over the past two decades, the S&P 500's average implied volatility (VIX) has been approximately 19-20%. Average realized volatility: 15-16%. The market consistently overprices volatility by 20-25%. This gap persists through bull markets, bear markets, crashes, and recoveries. It narrows during extreme events and widens during calm periods, but the long-term average is clear. You sold volatility at $20. It was worth $16. The $4 difference is profit. Repeat across hundreds of trades.

Why the Model Is "Wrong" in Your Favor

The Black-Scholes model makes several assumptions that don't perfectly match reality. Understanding these assumptions shows you exactly why the model creates opportunity for premium sellers.

The model assumes volatility is constant. In reality, volatility clusters. Quiet periods are followed by quiet periods. Volatile periods are followed by volatile periods. The model doesn't account for this clustering, which means it misprices options during transitions between regimes. When the market shifts from high vol to low vol, implied volatility drops slower than realized volatility, creating wider spreads for sellers. When the market shifts from low vol to high vol, implied spikes faster than realized, temporarily narrowing the edge but creating opportunities for sellers who enter after the spike and benefit from mean reversion.

The model assumes returns are normally distributed. In reality, stock returns have "fat tails," meaning extreme moves happen more often than a normal distribution predicts. This is why out-of-the-money puts are more expensive than the model's base case would suggest (a phenomenon called volatility skew). Traders who are aware of fat tails overpay for crash protection, which further inflates put premiums and increases the VRP for sellers.

The model assumes you can continuously hedge. In reality, you can't trade every microsecond. This "hedging gap" creates additional uncertainty that gets priced into options, again inflating premiums above their theoretical fair value.

Every one of these model limitations pushes option prices higher than they "should" be. And every one of them creates opportunity for the premium seller who understands that the option they're selling is priced using assumptions that systematically overstate the risk.

Every assumption the Black-Scholes model gets 'wrong' is wrong in a direction that benefits premium sellers. The model assumes constant volatility (reality: clustering), normal distributions (reality: fat tails that inflate put premiums via skew), continuous hedging (reality: hedging gaps add uncertainty), and frictionless markets (reality: friction inflates pricing). Each of these gaps between model and reality pushes option prices higher than theoretical fair value. Selling overpriced instruments is how you build a career.

The Exact Steps to Use This Edge

Understanding the volatility risk premium is academic. Exploiting it is practical. Here are the specific steps I use to translate the equation's built-in alpha into actual trading profits.

Step 1: Measure the current VRP. Compare implied volatility to recent realized volatility. You can do this on individual stocks using ATR-annualized as a proxy for realized vol (ATR% x sqrt(252)) and comparing it to the stock's current IV. When IV is 10+ percentage points above realized vol, the VRP is wide and the environment strongly favors selling. When the gap is narrow (under 3-4 points) or negative, the edge is thin and patience is required.

Step 2: Confirm with IV Percentile. IVP above 50 means current IV is higher than it's been more than half the time over the past year. This confirms that you're selling at an elevated level, not at the bottom of the IV range. IVP is the signal that the VRP is likely wide enough to justify entry. IVR above 35 provides a secondary confirmation.

Step 3: Sell at the right delta. The VRP exists across the entire options chain, but it's most reliably captured at 0.15 to 0.20 delta, where the premium collected represents a high-probability bet that the stock won't reach your strike. At this delta, your probability of profit is 80-85%, which means the VRP is working in your favor on the vast majority of trades. The rare losses are absorbed by the cumulative gains from the 80% winners.

Step 4: Enter at 30-60 DTE. The volatility risk premium is largest in the 30-60 day window because this is where the uncertainty about future volatility is greatest. Shorter-dated options have less time for the VRP to manifest. Longer-dated options have more exposure to regime changes that could shift the IV-RV relationship. The 30-60 DTE sweet spot captures accelerating theta decay while the VRP is at its widest.

Step 5: Close at 50% of max profit. This is where the VRP meets practical management. By closing at 50% of max profit, you're capturing the majority of the VRP in the first half of the trade's life (when theta decay is predictable and IV mean reversion is working in your favor) while avoiding the second half (when gamma risk increases and the probability of a late move rises). The VRP doesn't require you to hold to expiration. It requires you to be in the trade long enough for the overpriced volatility to not materialize, which typically happens in 15-25 days on a 45 DTE trade.

Step 6: Size for survival, not for maximization. The VRP is a long-term edge. It works across hundreds of trades. It does not work on every single trade. Position sizing at 2-5% max loss per trade ensures that the occasional trade where realized volatility exceeds implied (and it will happen) doesn't destroy the account that's compounding the VRP gains from the other 80% of trades.

Six steps to translate the equation's built-in alpha into actual profits. Measure the IV-to-RV gap (wider = richer VRP). Confirm with IVP above 50 (selling at elevated levels). Sell at 0.15-0.20 delta (80-85% probability). Enter at 30-60 DTE (VRP widest here). Close at 50% of max profit (harvest before gamma risk). Size at 2-5% max loss (survive the losses, let the math work). Each step captures the VRP at its widest while managing the risk that realized vol occasionally exceeds implied.

The Edge Is Real, But It's Not Free

The volatility risk premium is not a free lunch. It's a risk premium, and the word "risk" is doing real work in that phrase.

The VRP exists because option sellers are taking on genuine risk. When the market crashes, when a stock gaps 15% on earnings, when a geopolitical shock sends the VIX from 15 to 40 in a week, realized volatility temporarily exceeds implied, and premium sellers take losses. These are the events that the insurance buyers were paying to protect against, and they're the events that justify the premium they overpaid during the 90% of the time when nothing dramatic happened.

The professional premium seller's advantage is not that they avoid these events. It's that they survive them. Position sizing, cash reserves, diversification across uncorrelated underlyings, and a written drawdown plan ensure that the occasional spike in realized volatility is a temporary setback, not a permanent impairment. The VRP then resumes, the edge reasserts itself, and the compounding continues.

This is why the equation works for professional premium sellers over decades and destroys amateur option sellers in months. The equation's edge is real and persistent. But it requires the discipline to size correctly, the patience to let the law of large numbers work, and the structural protections to survive the inevitable periods when the market's "guess" about volatility turns out to be right, or even conservative.

The Equation and Your Process

Every element of the premium-selling process I teach at The Option Premium is designed to capture the volatility risk premium systematically.

Selling at elevated IV Percentile ensures you're entering when the VRP is wide. Placing strikes at 0.15-0.20 delta ensures you're selling premium that's priced for movement the stock probably won't deliver. The 30-60 DTE entry captures the VRP at its widest point. The 50% profit target harvests the VRP before gamma risk erodes it. The 2-5% position sizing survives the events when the VRP temporarily inverts. The uncorrelated portfolio diversification ensures no single VRP failure endangers the account.

You don't need to calculate the Black-Scholes equation by hand. Your platform does it for you. But understanding what the equation is doing, and specifically where its assumptions create a systematic gap between price and reality, is what transforms mechanical rule-following into conviction-based trading. When you know why the edge exists, you hold through the drawdowns that make amateurs quit. When you know the VRP is structural, not accidental, you keep selling premium after a loss instead of switching strategies out of fear.

The trillion-dollar equation didn't just create the options market. It created the systematic, measurable, repeatable edge that funds every premium seller's career.

Risk Reality Check

The volatility risk premium has been persistent over the past several decades, but it is not guaranteed to persist forever. Market structure changes, algorithmic trading, and the proliferation of options-selling strategies could theoretically compress the VRP over time. Academic research suggests the VRP has narrowed somewhat since the 2000s compared to earlier decades, though it remains positive and meaningful.

Additionally, the VRP is an average over many trades. Any individual trade can lose regardless of the VRP's existence. A stock can realize more volatility than implied on any specific expiration cycle. The edge is statistical, not deterministic, and it requires the law of large numbers (many trades over many months) to manifest reliably.

Key Takeaways

The Black-Scholes model prices options using five inputs: stock price, strike price, time to expiration, risk-free rate, and volatility. Four are observable facts. The fifth, volatility, is a guess about the future. The entire option price depends heavily on this guess, and the guess is systematically too high. This is the foundation of the premium seller's edge.

The volatility risk premium (VRP) is the persistent gap between implied volatility (what the market charges) and realized volatility (what actually happens). Over the past two decades, the S&P 500's average IV has been 19-20% while realized volatility has averaged 15-16%. The market consistently overprices volatility by 20-25% because option buyers are purchasing insurance and are willing to overpay for it.

Six steps to exploit the VRP: measure the current IV-to-RV gap (wider = better), confirm with IVP above 50, sell at 0.15-0.20 delta, enter at 30-60 DTE, close at 50% of max profit, and size at 2-5% max loss per trade. Each step is designed to capture the VRP at its widest point while managing the risk that realized vol occasionally exceeds implied.

The VRP is not free. When markets crash, realized volatility catches up to implied, and premium sellers take losses. The professional's advantage is not avoiding these events. It's surviving them through position sizing, cash reserves, diversification, and a drawdown plan. The VRP then resumes, the edge reasserts, and the compounding continues.

The Black-Scholes model's assumptions (constant volatility, normal distributions, continuous hedging) all push option prices higher than they should be. Every assumption that's "wrong" is wrong in a direction that benefits the premium seller. The model systematically overprices options, and selling overpriced instruments is how you build a career.

Fischer Black and Myron Scholes didn't set out to create an edge for premium sellers. They set out to solve an equation. But the equation they solved revealed a truth about markets that has persisted for over fifty years: the price of an option reflects fear, and fear is expensive. The premium seller's job is simple. Measure that fear. Confirm it's overpriced. Sell it at the right delta, at the right time, at the right size. And let the equation do the rest.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply