- The Option Premium

- Posts

- 📩 The Option Premium Weekly Newsletter - January 4, 2026

📩 The Option Premium Weekly Newsletter - January 4, 2026

How I'm Preparing for Next Week and the Year Ahead

Before We Get Started…

As we turn the page on the year, I want to thank you again for being here. I'm genuinely grateful for the trust, the attention, and the thoughtful questions you've brought to The Option Premium. I've worked hard to build something that's honest, transparent, practical, realistic, and repeatable, and your engagement is the reason it's grown into what it is.

An important note on this week's format: This week’s issue breaks from our typical structure, which we'll return to next week. This week, I'm keeping the focus purely on what I'm preparing for the week and year ahead as we launch the expanded 2026 framework/portfolios for Wealth Without Shares.

In Wealth Without Shares, I'll be introducing five distinct PMCC portfolios and establishing many of those initial positions throughout the week. This includes the Small Dogs and All-Weather portfolios, notably, the Small Dogs strategy delivered over 65% returns in 2025.

Each portfolio is designed with a specific objective and risk profile: from conservative capital preservation to aggressive growth, from dividend-focused strategies to volatility-harvesting approaches. By running these five portfolios in parallel, you'll see how the same core PMCC mechanics adapt to different market environments, different underlying securities, and different return objectives.

This week marks the formal launch of this expanded framework, meaning you'll witness the initial position selection, the entry criteria I'm using, the specific strikes and expirations I'm choosing, and the reasoning behind each trade. You'll see the portfolios built from the ground up, not just the results after the fact.

If you've been considering Wealth Without Shares or want to deepen your understanding of how PMCCs work across multiple strategies simultaneously, this week offers the best opportunity to join and build these positions. You'll have the complete context from day one, rather than joining mid-stream and trying to piece together the rationale behind existing positions.

Here's to a happy, healthy, and prosperous 2026!

📺 Subscribe to the YouTube channel so you’re first in line when the initial videos go live.

👥 Join the private Facebook group or connect with me over on X.

💌 Email me anytime with topics you’d like to see covered in the newsletter, on YouTube, or in future webinars.

📰 Market Commentary & Snapshot

The Buy and Hold Myth: Why Options Matter in Today's Market

For the better part of fifteen years, a generation of investors operated under a dangerous assumption: markets only go up. The concept of sustained downturns seemed like ancient history, something their parents experienced but they never would. While seasoned traders understand market cycles intimately, countless investors who've never weathered a genuine bear market with real money at stake have recently discovered a harsh reality.

What strikes me most isn't the surprise at falling markets, it's the blind faith that passive buy-and-hold automatically equals long-term success. I maintain core positions for the long haul, absolutely. But I do it in a far more capital efficient manner using LEAPS, mostly coupled with short calls. I also systematically trade options around those holdings. Without a crystal ball to predict the future, options provide something more valuable: the power to select my market stance (bullish, bearish, or neutral), quantify my probability of profit on every position, and, critically, define my risk parameters precisely. These principles form the foundation of intelligent capital management and what I focus on at The Option Premium.

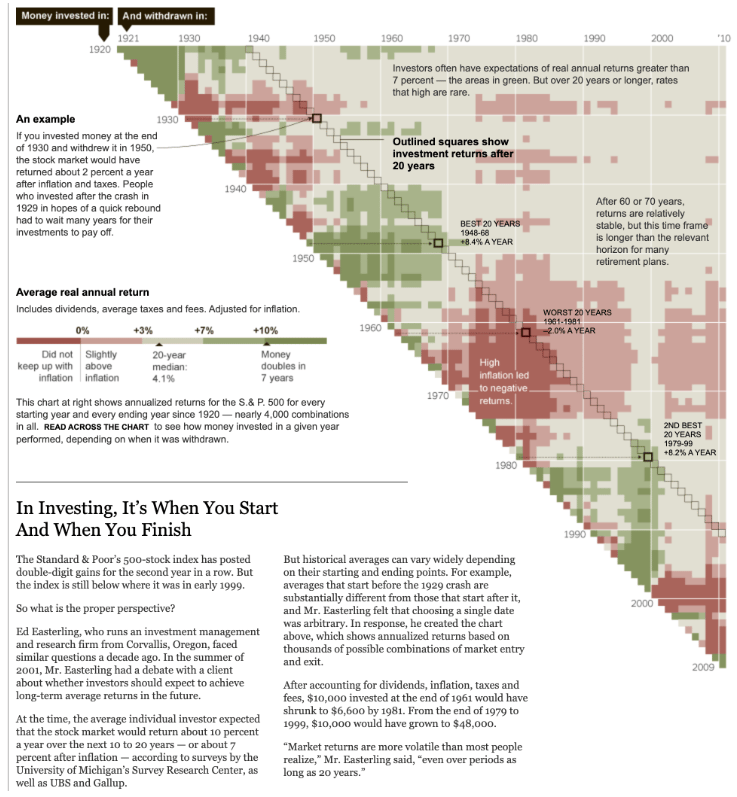

Source: Crestmont Research via The New York Times

The Data That Changes Everything

Years ago, I encountered research that fundamentally altered my investment perspective. Every serious investor should examine this data before committing another dollar to the markets. Once you see it, your entire approach to capital allocation will shift.

Ed Easterling of Crestmont Research published analysis that exposes an uncomfortable truth about market returns. The research is dated, but still holds true today.

The data reveals something conventional wisdom ignores: the traditional buy-and-hold approach contains significant vulnerabilities. Time in the market doesn't guarantee returns, your entry point and exit point determine everything.

Consider this: accounting for dividends, inflation, taxes, and fees, $10,000 invested at the close of 1961 would have declined to $6,600 by 1981. Yet that same $10,000 invested at the end of 1979 would have grown to $48,000 by 1999.

Simple table, profound implications.

Markets Are Cyclical. Your Strategy Shouldn't Be Passive.

Markets move unpredictably. With passive strategies, your results depend entirely on when you happen to start and finish investing. Extreme volatility remains normal across timeframes spanning two decades or more. We can't predict future returns, but we don't have to surrender control and hope for favorable timing.

We can implement systematic, probability-based strategies with clearly defined risk parameters.

I'm not dismissing buy-and-hold. Dollar-cost averaging and long-term position building serve legitimate purposes in portfolio construction.

However, today's individual investors access the same institutional strategies once reserved for professional trading floors. These approaches enable consistent returns across all market environments, rising, falling, or sideways. They're built on mathematics, statistics, and probability, not speculation or market timing.

The barriers that once separated retail traders from professional strategies have essentially disappeared.

Rethinking Modern Portfolio Construction

Successful investing isn't about accumulating shares and crossing your fingers. It's not about naive diversification. Real investing means reducing volatility, creating smoother equity curves, and generating returns independent of market direction.

This is why options anchor my approach.

Options enable returns across any market environment while establishing precise risk boundaries. As someone who prioritizes statistical edges over speculation, I can select my probability of success for every single trade. Even when my directional thesis proves incorrect, proper options structure can still produce positive outcomes.

This is why you're reading The Option Premium. You want the same advantages.

📊 Weekly Market Stats

Market | Last (Jan 2) | Week | YTD |

|---|

S&P 500 | 6,858.47 | -1.0% | +0.2% |

Dow Jones | 48,382.39 | -0.7% | +0.7% |

Nasdaq Composite | 23,235.63 | -1.5% | -0.0% |

Russell 2000 | 2,508.22 | -1.0% | +1.1% |

VIX (spot) | 14.51 | +6.7% | -2.9% |

10Y Treasury | 4.19% | +6 bps | +4 bps |

Gold | $4,345.50 | -4.6% | -0.3% |

Bitcoin | 89,982.7 | +3.0% | +2.7% |

Building a Diversified PMCC Portfolio: The All-Weather Approach

One of the most powerful aspects of the Poor Man's Covered Call (PMCC) strategy is its capital efficiency. This efficiency doesn't just save you money, it opens the door to true portfolio diversification in ways that traditional stock ownership simply can't match.

Think about it: if you're tying up $39,800 to own 100 shares of a single stock, you're severely limited in how many positions you can hold. But when you can control those same 100 shares for $8,900 using LEAPS options, you've freed up $30,900 to deploy elsewhere. Suddenly, running five or six different portfolio strategies simultaneously becomes not just possible, but practical.

This is exactly how I approach Wealth Without Shares, our flagship PMCC service that proves you don't need to own stock to generate consistent returns from the equity markets.

Why the All-Weather Portfolio Makes Sense

The All-Weather portfolio concept, originally developed by Ray Dalio at Bridgewater Associates, represents one of the most elegant solutions to the fundamental problem every investor faces: we don't know what the future holds.

Will we face inflation or deflation? Economic growth or recession? Rising rates or falling rates? The All-Weather portfolio doesn't try to predict these outcomes. Instead, it allocates capital across assets that perform well in different economic environments, creating a portfolio designed to weather any storm.

The traditional All-Weather allocation looks like this:

40% long-term Treasury bonds

30% intermediate-term Treasury bonds

15% U.S. stocks

7.5% gold

7.5% commodities

But here's where things get interesting for Wealth Without Shares subscribers: I'm putting a twist on the typical All-Weather portfolio to better align with PMCC implementation and current market realities.

My All-Weather Twist for Wealth Without Shares

While Dalio's original framework is brilliant, I'm adapting it specifically for PMCC strategies in 2026. This isn't just about finding ETFs with liquid options, it's about creating an All-Weather approach optimized for premium collection, capital efficiency, and the current economic environment.

The traditional All-Weather portfolio was designed for buy-and-hold investors. But we're not buy-and-hold investors. We're active premium sellers using LEAPS options to gain leveraged exposure while simultaneously generating income. This fundamental difference demands a different approach.

Here's what I'm considering for the new Wealth Without Shares All-Weather portfolios:

First, we need liquid options markets with available LEAPS contracts, that's non-negotiable.

Second, we need to recognize that the economic environment has changed dramatically since Dalio created this model. Interest rates, inflation dynamics, and market structure all look different today than they did when the All-Weather portfolio was designed.

Third, we need to optimize for premium collection potential. Not all assets generate the same level of option premium, and that matters tremendously when you're selling calls monthly.

I'll be revealing the exact positions and allocation in the coming week as I finalize the new Wealth Without Shares All-Weather portfolio. The goal is to maintain the core philosophy, diversified exposure across multiple economic scenarios, while optimizing specifically for LEAPS-based premium collection.

Today, let me show you exactly how the PMCC approach works using one example that will likely be part of the All-Weather portfolio.

The PMCC Framework: Wealth Without Shares in Action

Let me walk you through exactly how we set up a PMCC position using current market prices. This is the same systematic approach we use in Wealth Without Shares.

As of today, GLD is trading at $398 per share.

Gold represents an essential component of any All-Weather portfolio. It tends to perform well during inflationary periods, acts as a safe haven during market turmoil, and provides diversification benefits due to its low correlation with stocks and bonds. But buying gold outright, or even gold ETFs, ties up significant capital.

That's where the PMCC strategy transforms the equation.

Step 1: Select the LEAPS Contract

We're looking for our long LEAPS contract with approximately two years until expiration. The key metric here is delta, we want a delta around 0.75 to 0.85, which gives us strong directional exposure while maintaining some buffer against the strike price.

Looking at the January 21, 2028 expiration (approximately 747 days out), we can find a strike with a delta of 0.80 trading for approximately $89.00 per contract.

Capital comparison:

Buying 100 shares of GLD: $39,800

Buying one LEAPS contract: $8,900

Capital savings: $30,900 (77.6%)

That $30,900 isn't just sitting idle, it's available to deploy across other positions in our All-Weather portfolio or to maintain as dry powder for future opportunities. This is the essence of capital efficiency that makes diversified PMCC portfolios possible.

Think about what this means practically: instead of tying up nearly $40,000 in a single gold position, we're accomplishing the same exposure for under $9,000. That difference, more than three times our position cost, can be deployed across bonds, international stocks, domestic equities, and other asset classes that complete the All-Weather framework.

Step 2: Sell the Short-Term Call

Now we implement the "covered call" portion of the strategy. We're looking for 30 to 50 days to expiration, targeting a delta between 0.20 to 0.35 (representing roughly 65 to 80% probability of success).

The February 20, 2026 expiration with 47 days until expiration offers calls with a delta of 0.30 trading for approximately $6.00.

Selling this call generates $600 in premium, which represents:

6.7% return on our LEAPS cost over 47 days

Approximately 52% annualized (premium only, not including LEAPS appreciation)

Compare this to a traditional covered call on 100 shares:

Premium collected: $600

Return on capital: 1.5% over 47 days

Annualized: roughly 11.6%

The PMCC strategy generates 4.5x the return on capital compared to the traditional covered call, using the exact same underlying asset and short call strike.

But here's what makes this even more powerful: after collecting that first $600 in premium, our effective LEAPS cost is now $8,300. We'll do this again in 47 days, and again 47 days after that. Over the course of a year, we're targeting 8 to 12 premium collection cycles, potentially generating $4,200 to $4,800 in total premium, roughly 47 to 54% return on our initial LEAPS investment.

And that's before accounting for any appreciation in the LEAPS contract itself if gold trends higher.

Step 3: Understand Your Position Delta

This is crucial and often overlooked: our net delta position is:

Long LEAPS delta: 0.80

Short call delta: -0.30

Net position delta: 0.50

This means for every $1 move in GLD, our position will gain or lose approximately $50. We have bullish exposure, but it's muted compared to owning shares outright (which would have a delta of 1.00).

As GLD potentially rises toward our short call strike, that 0.30 delta on the short call will increase, reducing our net position delta. If GLD pushes significantly higher, our position might approach delta-neutral. At that point, we evaluate: buy back the short call to restore directional exposure, or let it expire and sell a new call at a higher strike.

This delta management is critical. We're not passive investors hoping for the best. We're active managers making systematic decisions based on quantifiable metrics.

Managing the Position Over Time

The beauty of this approach is that we're not making a one-time trade, we're building a system for continuous premium collection.

Every 30-50 days, we:

Evaluate the short call position

Either let it expire worthless or buy it back early if it's lost most of its value

Sell a new call against our LEAPS, adjusting strike and expiration based on current market conditions and implied volatility

Each premium collection event:

Lowers our effective cost basis on the LEAPS

Generates cash flow that can be redeployed or withdrawn

Reduces overall position risk by creating a larger buffer

When our LEAPS reaches 8 to 12 months until expiration, we evaluate rolling it out to a new 2-year contract, effectively resetting the position while locking in any gains and continuing the premium collection cycle.

Let's project this forward to see the full picture:

Month 1-2 (47 days): Collect $600 premium

Effective cost basis: $8,300

Month 3 (next 45 days): Collect another $600 premium

Effective cost basis: $7,700

Month 4-5 (next 45 days): Collect another $600 premium

Effective cost basis: $7,100

After just three premium cycles over roughly 4.5 months, we've reduced our LEAPS cost by 20%. We continue this process month after month, systematically lowering our risk and generating cash flow.

If GLD rallies significantly, our LEAPS contract appreciates in value. If GLD trades sideways or modestly higher, we collect premium repeatedly. If GLD declines modestly, our premium collections cushion the loss. Only in a severe gold selloff do we face meaningful losses, and even then, we've risked $8,900, not $39,800.

The Real Power: Portfolio-Level Thinking

Here's where the All-Weather concept truly shines with PMCCs.

This GLD position uses $8,900 in capital and generates roughly $4,500 annually in premium (based on continuing to collect $600 every 45-50 days). That's a single component of a diversified portfolio.

Early next week, I'll be adding the remaining positions to complete the All-Weather portfolio framework.

These positions will span different asset classes, long-term bonds, domestic equities, and international stocks, each selected for both its role in the All-Weather strategy and its suitability for PMCC implementation. Each will follow the same systematic approach: purchase LEAPS contracts with strong deltas, sell premium consistently against those positions, and manage based on quantifiable metrics rather than emotions or predictions.

The capital efficiency we're seeing with GLD, controlling $39,800 worth of exposure for $8,900, multiplies across every position. A complete All-Weather PMCC portfolio might require $18,000 to 25,000 in total capital while providing exposure equivalent to a $175,000 to 225,000 traditional stock and ETF portfolio.

Leverage ratio: 4 to 5x or more

More importantly, each position generates premium monthly, creating multiple income streams while maintaining the diversification that makes the All-Weather concept so robust. When one asset class struggles, others typically perform, that's the entire point of the framework.

This is what Wealth Without Shares is all about: proving that stock ownership is optional, not mandatory, for equity market participation.

Through PMCC strategies, we:

Reduce capital requirements by 75 to 85% compared to stock ownership

Generate consistent premium income regardless of market direction

Maintain positive delta exposure to capture upside moves in the underlying assets

Diversify efficiently across multiple strategies and asset classes

Manage risk systematically through defined position sizing and delta management

We're not trying to hit home runs. We're not chasing the next meme stock or predicting which sector will outperform. We're not gambling on earnings reports or hoping management delivers on ambitious promises.

We're simply using the probability-based, time-decay mechanics of options to generate consistent returns while risking far less capital than traditional stock ownership requires.

The All-Weather PMCC portfolio, represents this philosophy at its finest: systematic, diversified, capital-efficient exposure across multiple asset classes, generating premium income month after month, regardless of which way the economic winds blow.

What's Coming for Wealth Without Shares

The new All-Weather portfolios represent an exciting expansion of the Wealth Without Shares service. Rather than focusing solely on individual stock opportunities, we're building complete, diversified portfolio strategies that subscribers can implement alongside their existing positions.

This isn't about abandoning what works, our core PMCC approach on quality stocks remains as strong as ever. Companies like Microsoft, Costco, and Visa continue to offer excellent PMCC opportunities with strong premium collection potential and solid underlying fundamentals.

This is about giving you additional tools: proven portfolio frameworks optimized for LEAPS-based premium collection. Think of it as a complete toolkit for building wealth through options.

You might run:

An All-Weather PMCC portfolio for broad market exposure and stability

A Growth-focused PMCC portfolio for higher premium potential with increased volatility

A Dividend Aristocrat PMCC portfolio for combining income strategies

Individual stock PMCCs on specific opportunities you've identified

The capital efficiency of the PMCC approach makes all of this possible simultaneously, something that would be financially impossible with traditional stock ownership.

The Bottom Line

Consider this: you don't need $200,000 to build a diversified, all-weather portfolio. You need $18,000 to 25,000, the right strategy, and a willingness to think differently about how wealth is built.

That $8,900 GLD position we discussed? It's generating the same premium as $39,800 worth of stock. The difference, that $30,900, is capital you can deploy elsewhere or keep as safety margin.

Multiply that efficiency across four or five positions, and you're controlling a six-figure portfolio with a fraction of the typical capital requirement. You're generating meaningful monthly income through systematic premium collection. And you're diversified across asset classes that perform differently in various economic environments.

That's not theory. That's not hopium. That's the mathematical reality of how PMCC strategies work when implemented systematically across a diversified portfolio framework.

That's the power of Wealth Without Shares.

The Implied Truth: Weekly Table Overview

Unlock the Full Picture - Upgrade to access the complete table, including all 100 equities (AAPL, META, AMZN, NVDA and more)

Every number tells a story. Each week, we decode the landscape across the most liquid ETFs, because this is where retail traders get the cleanest signals and the least slippage. But the power isn’t in the data, it’s in how you interpret it.

Below is your edge: a strategic overview that reveals where the premium is overpriced, where price action is exhausted, and where the highest-probability setups exist for the coming week.

This section is here to help you choose what works for your strategy. The numbers are facts, not opinions. Whether you sell premium, buy directional spreads, or trade reversals, the edge begins with understanding volatility and momentum. Let’s dig in.

What This Table Tells Us

Use this weekly to guide your trade ideas, not predict outcomes.

The data is factual. There’s no opinion in this grid, only opportunity.

Choose what aligns with your timeframe, risk appetite, and edge.

Week Ending January 2, 2026

If you're only watching SPY, you're missing where the actual premium lives this week.

The indexes are sleepy. The "stuff trade", metals, materials, energy—, s where volatility is actually paying you to play.

Here's what matters for options sellers right now.

The numbers tell the story:

DIA: 12.1% IV (6% IV Rank)

SPY: 12.9% IV (6% IV Rank)

QQQ: 18.1% IV (10% IV Rank)

Translation: the market is yawning.

When index volatility is this thin, the amateur move is selling tighter strikes to "make the math work." That's how you end up with a portfolio full of mosquito-bite credits and oversized risk.

If you're selling index premium anyway: Go farther out in strike (15 to 25 delta), stick to 30 to 45 DTE, and take profits faster than usual. You're not being paid to be stubborn here.

The Real Action: Metals Are Trending and Paying

This is the clearest signal on the board:

SLV: 80% IV Rank, 98% IV Percentile, ADX running 45 to 51

GDX: 63% IV Rank, 94% IV Percentile, ADX 25 to 31

GLD: 52% IV Rank, 88% IV Percentile, ADX 29 to 36

When you see elevated IV and strong directional momentum (ADX), you're not just collecting random premium, you're getting paid in a market that's actually moving with purpose.

The playbook:

Sell bullish, defined-risk premium (put spreads work beautifully here)

Trade with the trend, not against it

Keep management mechanical: take 50 to 70% of max profit and move on

If you're selling calls, do it professionally: small size, far OTM, and assume the trend can stay irrational longer than your patience

Rotation Is Real: Materials and Energy Over Tech

What's working:

XLB (Materials): 83% IV Percentile with strong relative strength across timeframes

XLE (Energy): Constructive setup with mid-level volatility and solid momentum

What's not:

QQQ shows weak 2-day relative strength and below-50 RSI rank

This isn't a broad rally, it's rotational. And rotational markets reward selection over enthusiasm.

The smarter approach: Sell premium where you're actually getting paid to wait (materials, metals, energy). Use QQQ for risk control and position sizing, not as your main income engine.

Financials: Trending, But Don't Overpay Yourself

KRE and XLF both show strong ADX readings (39/31 and 34/27), but IV is only mid-range. They're moving cleanly, but you're not being wildly compensated.

The takeaway: These are "good structure, not hero trade" setups. Defined-risk credit spreads on pullbacks beat chasing momentum here.

👉 For a deeper dive each week, including a full breakdown of the most liquid optionable ETFs and an in-depth analysis of 100+ highly liquid equities, check out The Implied Perspective, our paid service that turns this data into structured, high-probability premium ideas.

As always, this section is meant to be an educational lens on the current landscape, not personal advice. The edge comes from matching the strategy to the regime, keeping position sizes small, and letting a large sample of disciplined trades do the heavy lifting over time.

Quick Reference

Field | Meaning / How to Use It |

|---|---|

Imp. Vol (IV) | Implied volatility. Higher IV = richer option premiums and wider expected moves. |

IV Rank (IVR) | Where today’s IV sits vs. the past year (0–100%). Rule of thumb: >35% favors premium-selling strategies. |

IV Percentile (IVP) | % of the past year that IV was below today’s level. Confirms whether elevated IV is persistent (not a one-off spike). |

RSI (2/5/9/14) | Momentum gauge. >80 = overbought, <20 = oversold. Shorter lookbacks (2/5/9) react faster; 14 is steadier. |

ADX (9/14) | Trend strength (0–100). <20 range-bound, 20 to 25 forming, 25 to 35 established, >35 strong trend. |

🔗 Let’s Stay Connected

Have questions, feedback, or just want to say hello? I’d love to hear from you.

📩 Email me anytime at [email protected]

📺 Subscribe on YouTube so you’ll be notified when the first videos are released.

👥 Join the private Facebook group or connect with me on X.

💌 Send me your topic requests, whether for the newsletter, YouTube, or webinars. Seriously, send them. 🙂

Thanks again for reading. I hope you found today’s insights valuable and worth your time.

Trade Smart. Trade Thoughtfully.

Andy Crowder

Founder | Editor-in-Chief | Chief Options Strategist

The Option Premium

Educational use only. The Option Premium is a publication for educational purposes and does not provide personalized investment advice. Options involve risk and are not suitable for all investors. Always confirm details and manage risk prudently.

Reply