- The Option Premium

- Posts

- Put-Call Parity in Plain English

Put-Call Parity in Plain English

Put-call parity is the single equation under every synthetic options position. Taught without academic notation, with worked examples for premium sellers.

Andrew Crowder

May 19, 2026

Put-Call Parity in Plain English

Most options books introduce put-call parity with a wall of Greek letters and arbitrage equations that turn off the reader before they get to the point. That is a shame, because this single relationship is the most important piece of theory you will ever need. It governs every synthetic position, every covered call equivalence, every cash-secured put you ever construct.

If you understand put-call parity, you understand options. Everything else is detail.

The Equation, Translated

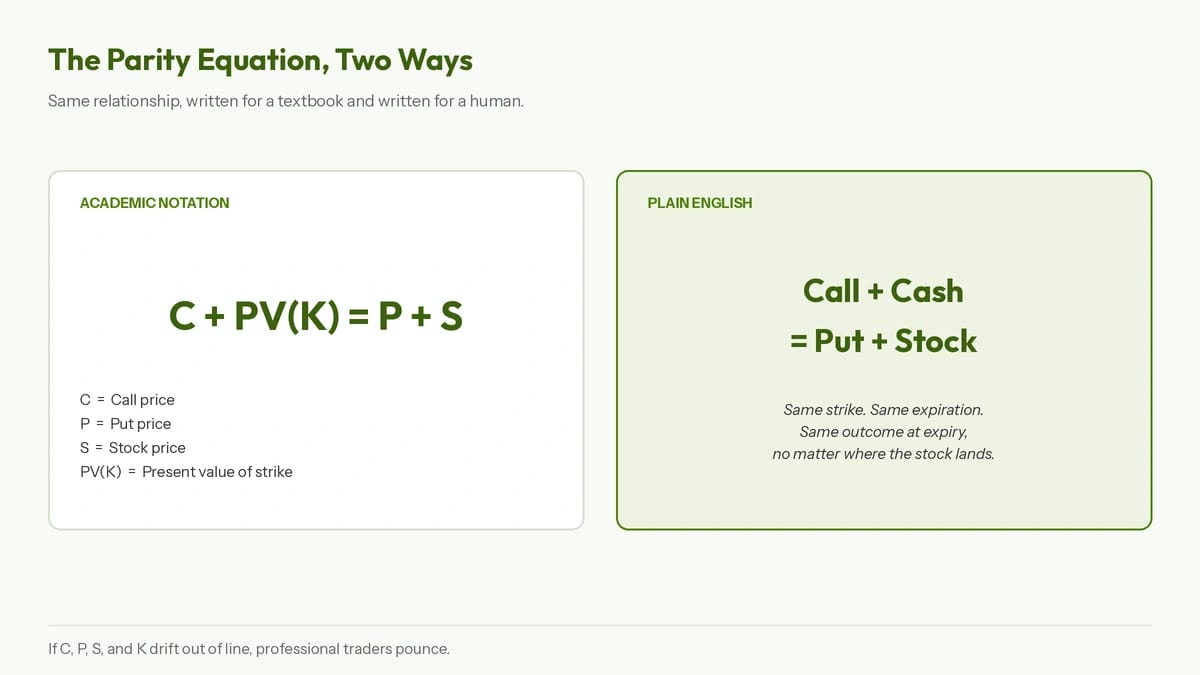

Here is the relationship, stripped of academic notation. A call plus enough cash to buy the stock at the strike has the exact same payoff as a put plus the stock itself.

Same strike. Same expiration. Same outcome at expiry, no matter where the stock lands.

That is the entire idea. The call, the put, the stock, and the strike price are locked together by arbitrage. If any of these drift out of line, professional traders pounce and pull them back. Which means you can confidently substitute one position for another and know they will behave the same way at expiration.

Why It Has to Be True

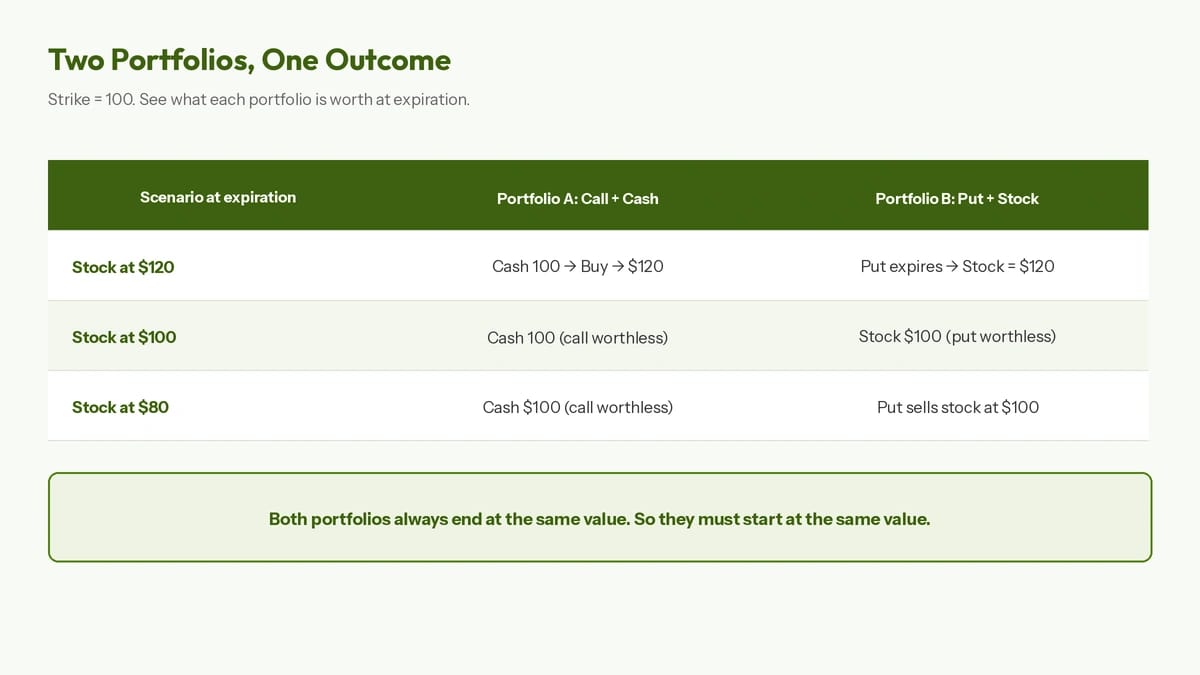

Imagine two portfolios. Portfolio A holds one call at the 100 strike and enough cash to pay 100. Portfolio B holds one put at the 100 strike and one share of stock.

At expiration, if the stock is at 120, Portfolio A exercises the call (paying 100 from cash) and ends up with stock worth 120. Portfolio B's put expires worthless and the stock is worth 120. Both portfolios end at 120.

If the stock is at 80, Portfolio A's call expires worthless and the cash is worth 100. Portfolio B sells the stock at 100 via the put. Both portfolios end at 100.

No matter where the stock lands, the two portfolios end up at the same value. If they end up at the same value, they must start at the same value. Otherwise somebody is selling free money, and free money in options markets gets vacuumed up in milliseconds.

What This Means for Synthetics

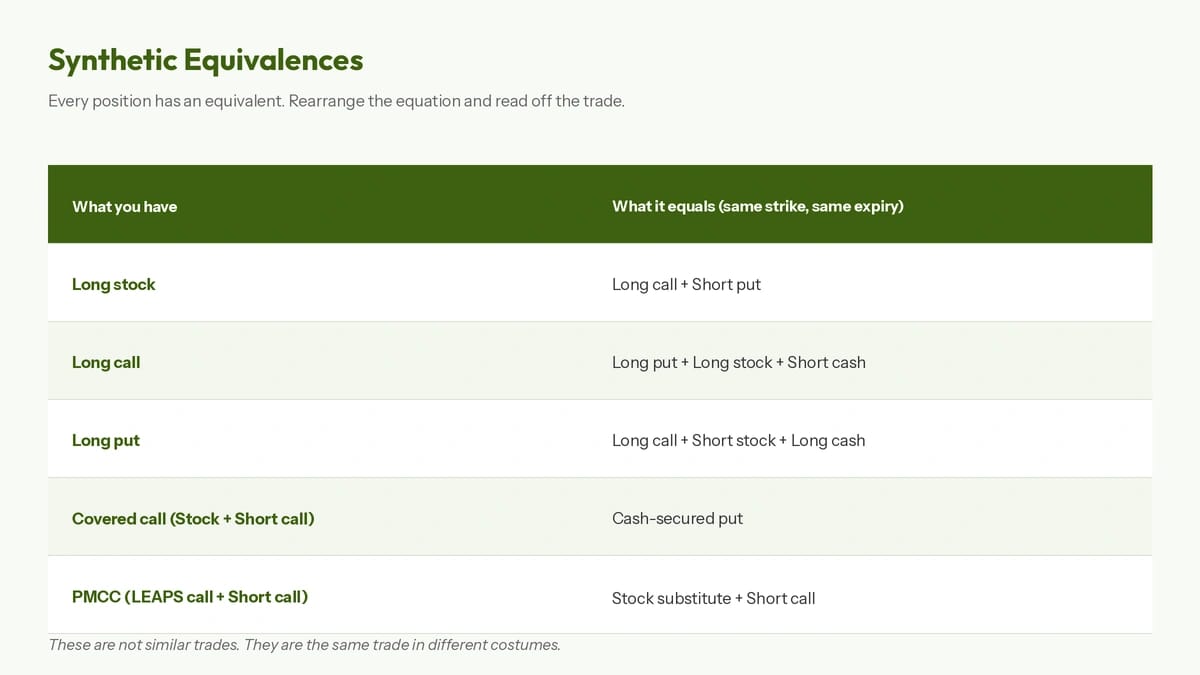

This is where parity stops being theory and starts being useful, because the equation rearranges any way you like.

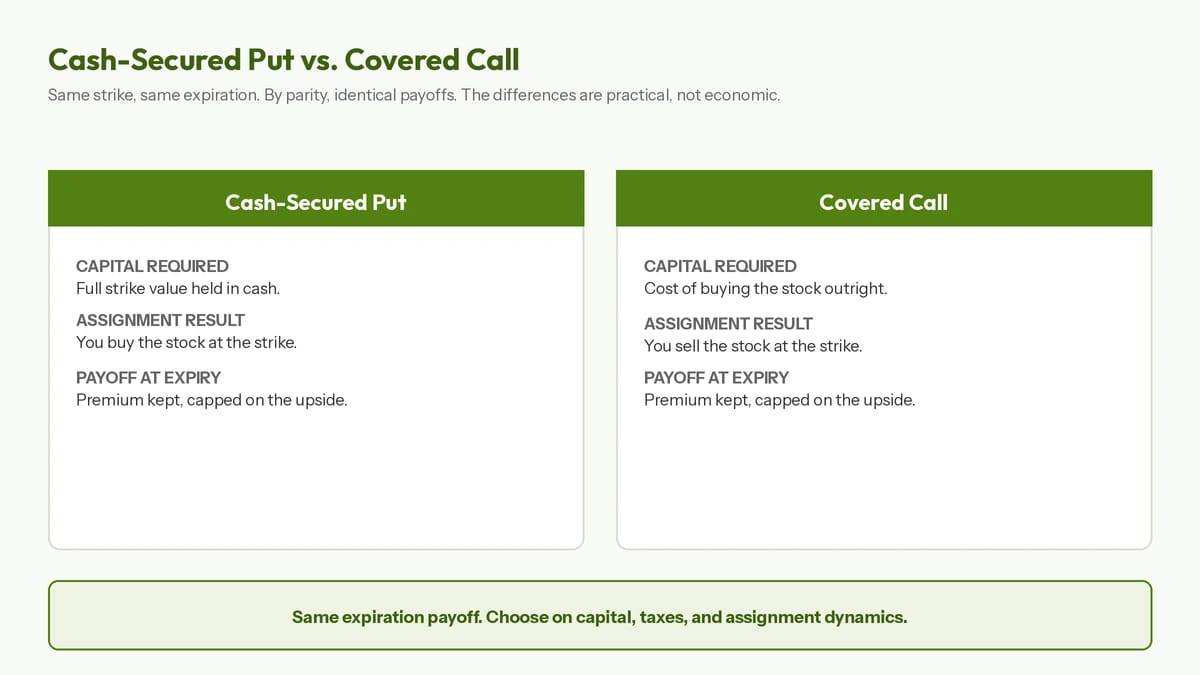

A long stock position is equivalent to a long call plus a short put at the same strike. That is the synthetic long stock you have probably heard about, and it is parity at work. A covered call (long stock plus a short call) is mathematically equivalent to a cash-secured put at the same strike and expiration. Same payoff diagram, same profit, same loss. The only differences are capital requirements, assignment mechanics, and tax treatment.

If you have ever wondered why I treat the cash-secured put and the covered call as two sides of the same coin in the Wheel Strategy, this is why. They are not similar. They are identical at expiration.

The PMCC Connection

Parity also explains why a deep in-the-money LEAPS call can stand in for stock in a Poor Man's Covered Call. Once a call is deep enough in the money and far enough out in time, its behavior tracks the stock almost perfectly. You are paying for the stock-equivalent exposure with less capital, which is the whole point of the PMCC structure.

The parity equation tells you something else too. The "almost perfectly" matters. A long call is not exactly the same as long stock, because parity also includes the value of the put at that strike and the present value of the cash. The put has time value as long as the option has time on it. That residual is what separates a synthetic from the real thing.

What Parity Does Not Say

Here is what tends to get lost in the textbook treatment. Parity tells you the economics are equivalent. It does not tell you the practicalities are equivalent.

Cash-secured puts and covered calls have the same expiration payoff, but they tie up capital differently, get taxed differently in some accounts, and carry different assignment dynamics around dividends. Synthetic long stock has the same payoff as actual stock, but you do not collect dividends, and you have option-specific mechanics to manage. When you choose between equivalent structures, the economics are not the deciding factor. The deciding factors are capital, taxes, assignment timing, and what fits your account structure.

Practitioner Edge

When I am choosing between a cash-secured put and a covered call at the same strike and expiration, I am not asking which one will make more money. Parity already answered that question. I am asking which one fits my capital structure better, which one fits my tax situation better, and which one I would rather manage if it goes against me. That is a very different question, and parity is what lets you ask it cleanly.

Risk Reality Check

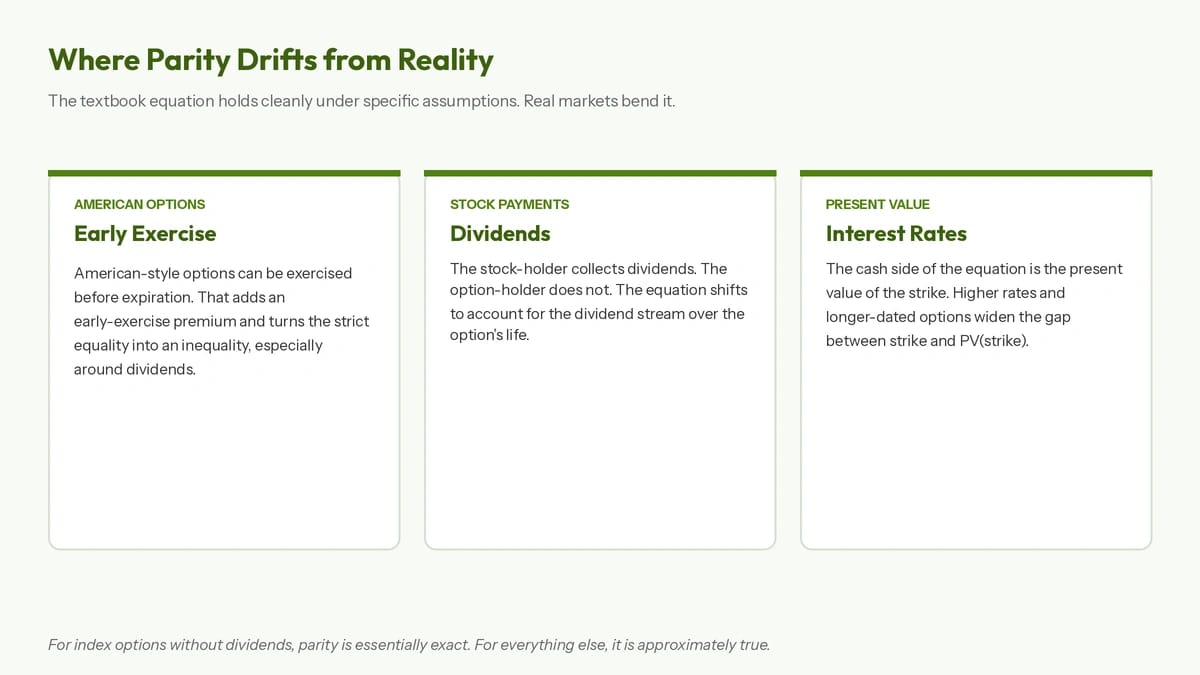

Parity holds cleanly for European-style options without dividends. American options can be exercised early, which breaks the equivalence in specific situations, particularly around ex-dividend dates for deep in-the-money calls. Dividends shift the equation because the stock-holder gets paid and the option-holder does not. Interest rates affect the cash component, which is why the formula technically uses the present value of the strike rather than the strike itself.

In practice, the relationship still holds approximately for most index and large-cap equity options that retail traders deal with. But "approximately" is doing real work in that sentence. Pin risk, early exercise on dividend-paying stocks, and interest rate sensitivity in long-dated options are all places where the textbook equation and the trading desk reality drift apart.

Key Takeaways

Put-call parity is the single equation that ties calls, puts, stock, and strike prices together. Understanding it means you can recognize when two seemingly different positions are actually the same trade dressed differently, and when two seemingly similar positions have a hidden gap.

Synthetics are not magic. They are parity in different costumes. The traders who internalize this stop chasing strategies and start choosing structures based on what actually matters: capital efficiency, tax treatment, and assignment mechanics. The payoff is settled by the equation. The rest is craftsmanship.

FAQ

Is put-call parity always exact in real markets?

For European-style index options without dividends, it is remarkably close to exact. Market makers enforce it through conversion and reversal arbitrage, which means any meaningful drift gets traded back into line within seconds. For American options on dividend-paying stocks, the relationship is approximate rather than exact, with the gap widening around ex-dividend dates and in deep in-the-money calls where early exercise becomes attractive. For most retail strategies, you can treat the relationship as reliable.

How do I actually use put-call parity in my trading?

The most practical use is recognizing equivalences. If you know a covered call and a cash-secured put at the same strike are mathematically identical at expiration, you can choose between them based on capital, taxes, and account structure rather than imagined profit differences. If you understand that a deep in-the-money LEAPS call behaves close to stock, you can use it as a stock substitute in a PMCC without confusion. Parity gives you the map of which positions are actually the same trade in disguise.

Does put-call parity work the same for American and European options?

The basic relationship holds for both, but the equality is strictly exact only for European-style options. American options can be exercised early, which adds an early-exercise premium to puts and (in dividend-paying stocks) to calls. The result is that American option prices satisfy a parity inequality rather than a strict equality. For most retail trading purposes, the difference is small enough to ignore. For dividend-sensitive strategies, it matters.

Closing

Put-call parity is not trivia for the CFA exam. It is the equation under the floor of every options position you will ever take, and once you see it, you cannot unsee it. Every synthetic, every conversion, every wheel rotation runs on the same simple machinery. The traders who quietly compound for decades are the ones who learned to look at the equation first and the marketing copy last.

Probabilities over predictions,

Andy

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply