- The Option Premium

- Posts

- PMCC 101: Income Overlay with LEAPS

PMCC 101: Income Overlay with LEAPS

Build a PMCC: long LEAPS + short calls for steady income and basis reduction.

PMCC 101: Income Overlay with LEAPS

The covered call strategy works. You own 100 shares, sell a call against them, collect premium, repeat monthly. Simple, proven, profitable, until you run the numbers on capital deployment.

A $100 stock position requires $10,000 per 100 shares. Selling a 30-delta call might generate $150 monthly. That's a 1.5% return on deployed capital, 18% annualized if you could maintain that pace perfectly. Not bad, except you've locked up $10,000 to generate $150.

The Poor Man's Covered Call, PMCC for short, solves this capital efficiency problem. Instead of owning shares, you own a deep-ITM LEAPS call and sell shorter-term calls against it. You're running the exact same income strategy with 65 to 85% less capital.

This isn't theory. I've run PMCC positions across multiple portfolios for years, documenting every trade, every roll, every adjustment. The strategy works when you understand the mechanics, respect the risks, and manage positions systematically. Let me walk you through how to build and maintain a PMCC that generates consistent income without tying up stock-level capital.

Understanding the PMCC Structure

A PMCC consists of two option positions working together:

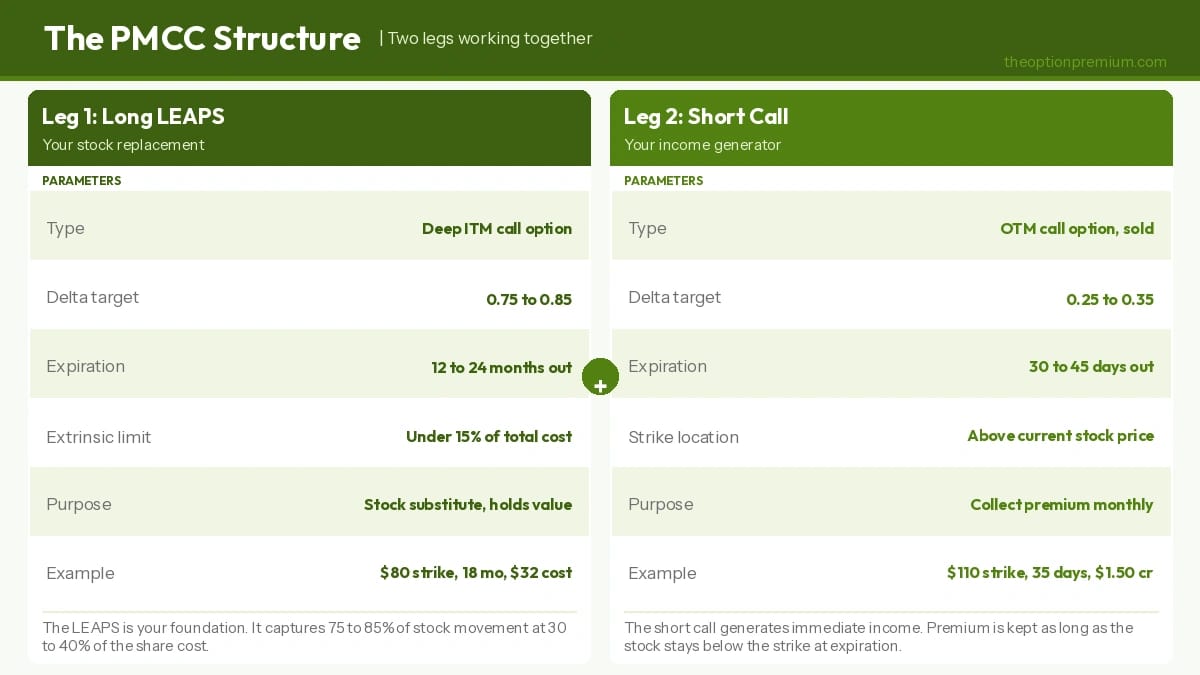

The Long LEAPS (Your Stock Replacement)

You buy a deep in-the-money call option, typically 12-24 months to expiration with a delta between 0.75 and 0.85. This LEAPS call acts as your stock substitute, it moves nearly dollar-for-dollar with the underlying while costing a fraction of shares.

On a $100 stock, you might buy an $80 strike LEAPS 18 months out for $32 ($3,200 per contract). That's your long position, your foundation, your synthetic stock ownership.

The Short Call (Your Income Generator)

Against that LEAPS, you sell a shorter-term call option, typically 30-60 days to expiration with a delta between 0.25 and 0.35. This generates immediate income through premium collection.

You might sell a $110 strike call 35 days out for $1.50 ($150 per contract). That premium is yours to keep as long as the stock stays below $110 at expiration.

Together, these positions replicate a traditional covered call but with dramatically less capital deployed. You're running the same income strategy that works for shares, just more efficiently.

PMCC structure breakdown: Leg 1 long LEAPS parameters and Leg 2 short call parameters side by side with examples.

The Capital Efficiency Advantage

Let's make this concrete with side-by-side numbers.

Traditional Covered Call:

Buy 100 shares at $100 = $10,000

Sell $110 call for $1.50 = $150 income

Capital deployed: $10,000

Income return: 1.5% monthly

Poor Man's Covered Call:

Buy $80 strike LEAPS (0.82 delta) for $32 = $3,200

Sell $110 call for $1.50 = $150 income

Capital deployed: $3,200

Income return: 4.7% monthly

You're generating the same $150 income while deploying $6,800 less capital. That's a 68% reduction in capital requirements for identical premium collection.

This efficiency compounds across multiple positions. Instead of running two covered calls requiring $20,000, you can run five or six PMCCs with the same capital. You're diversifying across more underlyings, reducing single-name concentration risk, and maintaining the same total income generation.

The freed capital doesn't disappear. You can hold it in Treasury bills earning 4-5% annually. You can deploy it toward other strategies. You can keep it as dry powder for market opportunities. That optionality has value beyond just the individual PMCC position.

PMCC vs covered call comparison: same $150 income, $3,200 deployed vs $10,000, 4.7% vs 1.5% monthly return on capital.

Selecting Your LEAPS Foundation

The PMCC lives or dies based on your LEAPS selection. Choose poorly here and everything downstream suffers.

Delta Range: 0.75 to 0.85

Your LEAPS needs to behave like stock. Too low a delta and you're introducing directional risk that undermines the entire strategy. You want the LEAPS to capture 75-85% of the underlying's movement, high enough to replicate stock behavior, low enough to maintain meaningful capital efficiency.

I typically target 0.78-0.82 delta for PMCC positions. This gives me strong directional exposure without paying near-stock prices for the LEAPS.

Time Frame: 12 to 24 Months

Longer duration means slower time decay on your long position. You want that LEAPS to hold value steadily while you're selling multiple rounds of short calls against it.

With 18 months to expiration, you can comfortably sell 4-6+ monthly calls before needing to roll the LEAPS forward. The extrinsic premium decays slowly, your delta stays stable, and you're not constantly managing LEAPS replacement.

Avoid going shorter than 12 months on initial LEAPS purchases. Once you're inside that 12-month window, time decay accelerates and delta stability decreases. You want to roll to a new LEAPS before entering that zone.

Extrinsic Premium: Keep It Low

Your LEAPS premium consists of intrinsic value (how far ITM it is) and extrinsic value (time premium). You want extrinsic premium below 15% of the total LEAPS cost.

A $32 LEAPS should carry no more than $4 to 5 in extrinsic value. The rest should be intrinsic value, real, tangible equity in the underlying's price. High extrinsic premium means you're paying too much for time that will decay away regardless of what you collect from short calls.

Liquidity: Non-Negotiable

Your LEAPS needs tight bid-ask spreads and robust open interest. Wide spreads eat into your capital efficiency through poor fills on entries and exits.

Look for LEAPS with average daily volume above 500 contracts and open interest above 2,000 contracts. Bid-ask spreads should stay under $0.30-0.40. If you're seeing $0.80-1.00 spreads, the underlying probably doesn't have sufficient options liquidity for comfortable PMCC management.

Choosing Your Short Call Strikes

The short call selection determines your income generation and position management workload.

Delta Sweet Spot: 0.25 to 0.35

This delta range balances income collection with assignment risk. A 0.30 delta call has roughly a 30% chance of finishing in-the-money at expiration. That's a 70% probability of keeping the full premium without adjustment.

Go too low, say 0.15 delta, and premium collection drops substantially. You might collect $75 instead of $150. You've reduced your income by 50% to avoid assignment risk that wasn't that high to begin with.

Go too high, say 0.45 delta, and you're accepting near-coinflip odds of assignment or forced adjustment. The extra premium doesn't justify the increased management burden and directional risk.

I typically sell calls between 0.28 and 0.32 delta. This generates meaningful premium while maintaining high probability of success.

Strike Selection: Above Current Price

Sell calls out-of-the-money, above the current stock price. This gives you participation in upside movement up to the short strike while collecting premium.

If the stock trades at $100, I'm selling calls between $105 and $112, depending on days to expiration and implied volatility. The exact strike matters less than maintaining that OTM cushion and targeting appropriate delta.

Never sell at-the-money or in-the-money calls unless you're specifically trying to exit the position. You'll cap gains immediately and create unnecessary assignment risk.

Time Frame: 30-45 Days

This expiration window optimizes time decay collection. Options decay accelerates as you approach the final 30 days, but the sweet spot for consistent income collection sits between 30-45 days out.

You're capturing meaningful premium without taking on weekly expiration management burden. You're selling during the highest decay period without entering the chaotic final week where assignment risk spikes and gamma accelerates.

I typically sell 35-40 day calls. This gives me flexibility on timing, I can let them expire worthless or close early if they've decayed 50-75% of maximum profit.

PMCC short call selection guide: 8-parameter table plus three delta zone cards showing too conservative, sweet spot, and too aggressive.

Managing the Position Through Time

PMCCs require active management. You can't set and forget these positions like shares with dividends.

When Everything Goes Right

The stock stays below your short call strike. Time passes, premium decays, your short call approaches worthless. At 5-7 days to expiration, if the call is trading under $0.10, close it for the remaining pennies. Don't wait for expiration to squeeze out the last $0.05.

Immediately sell a new call 30-45 days out, targeting the same 0.28-0.32 delta range. You've collected nearly full premium on the expired call and established a new income position. Rinse and repeat monthly.

Your LEAPS sits in the background, holding value, maintaining high delta. As long as the stock doesn't crash, your foundation stays solid and you keep collecting premium.

When the Stock Rallies Into Your Short Call

The stock moves from $100 to $108, approaching your $110 short call strike. This is success, not failure, you're making money on the LEAPS as the stock rises.

But you need to manage assignment risk. Around 7-14 days before expiration, if the stock is threatening your strike, you roll the short call. Buy back the $110 call, simultaneously sell a new call 30-45 days out at a higher strike, perhaps $115 or $118.

This roll typically costs a small debit or generates a small credit, depending on implied volatility and how far you move the strike. You're giving the position more room to run while maintaining income generation.

The key: don't wait until the last minute. Roll with enough time remaining that you're not fighting gamma and rapidly decaying options. Give yourself breathing room.

When the Stock Drops Significantly

The stock falls from $100 to $88. Your short call expires worthless, great for that position. But your LEAPS has lost value. An 0.82 delta LEAPS losing $12 in underlying value means the LEAPS dropped roughly $9.84 ($984 per contract).

You collected $150 from the short call. That's partial basis reduction, but you're still down overall on the combined position.

Here's where PMCC discipline matters: you keep selling calls. The stock at $88 still supports selling calls for premium. You might sell a $95 or $98 call, collecting another $150-200. Over subsequent months, you continue collecting premium, gradually reducing your LEAPS basis.

The LEAPS still has 12+ months to expiration. Time is on your side. The stock doesn't need to recover to $100 for you to profit, it just needs to stabilize or grind higher slowly while you collect monthly premium.

Don't panic out of PMCCs during temporary drawdowns. The strategy is designed to work through volatility via consistent income collection. Trust the process unless your underlying thesis has fundamentally changed.

PMCC management scenarios: stock stays below strike, stock rallies into strike, and stock drops significantly with playbook for each.

The Real Risks Nobody Mentions

PMCCs aren't risk-free covered calls. They carry distinct risks that traditional covered calls don't face.

Early Assignment Risk

Your short call can be assigned early if it goes deep in-the-money, especially before ex-dividend dates or during low time-premium environments. When assignment happens, you're forced to sell shares you don't own, creating a short stock position.

You immediately exercise your LEAPS to cover that short stock, closing the position. This isn't catastrophic, but it forces position closure potentially before you wanted to exit and might trigger wash sale issues if you're not careful.

Prevention: monitor short calls approaching deep ITM status. If assignment risk looks high, roll the call forward and up before assignment occurs. Don't let calls sit deep ITM into expiration week.

LEAPS Decay Acceleration

As your LEAPS approaches 6-9 months to expiration, time decay accelerates. You're collecting $150 monthly from short calls, but the LEAPS might be decaying $200-300 monthly in extrinsic premium.

This creates negative carry, you're losing more on the LEAPS than you're collecting from short calls. The strategy stops working efficiently.

Prevention: roll your LEAPS to a new 18-month contract before you enter the acceleration zone. This keeps you in the favorable part of the time decay curve where extrinsic premium decay runs minimal.

Dividend Capture Risk

If the underlying pays significant dividends and your short call is in-the-money near ex-dividend date, early assignment probability spikes. The call holder can exercise to capture the dividend, forcing your position closed.

This risk escalates with high-dividend stocks. A 4% yielder paying quarterly dividends creates four annual windows where ITM short calls face elevated assignment risk.

Prevention: either avoid PMCCs on high-dividend stocks or manage short calls extra carefully around ex-dividend dates, rolling well before the date if strikes are threatened.

Liquidity Crunches

In both 2020 and during volatility spikes, options bid-ask spreads can widen dramatically. Your $0.30 spread might become $1.50 overnight. Rolling positions suddenly costs significantly more, eating into months of collected premium.

You can't eliminate this risk, but you can minimize it by selecting highly liquid underlyings with consistent options volume. Stick with major stocks and ETFs that maintain reasonable spreads even during stress.

PMCC risk guide and pre-entry checklist: five key risks on the left, ten-item trade entry checklist on the right.

When PMCCs Work Best

This strategy thrives in specific market environments and underlying characteristics.

Sideways to Moderately Bullish Markets

PMCCs love range-bound markets where stocks grind higher slowly or chop sideways. You're collecting premium consistently, your LEAPS maintains stable value, and assignment risk stays manageable.

In strongly bullish markets, you make money but face constant rolling decisions as strikes get challenged. In bearish markets, premium collection helps but doesn't fully offset underlying decline.

The sweet spot: markets making incremental higher highs and higher lows without explosive moves in either direction.

High Implied Volatility Environments

When implied volatility runs elevated, the short calls you sell generate more premium for the same delta. A 0.30 delta call might collect $200 instead of $150 during volatility expansion.

Your LEAPS does carry some vega exposure, but being deep ITM minimizes this. The net effect: you collect significantly more income during high-IV periods while your long position stays relatively stable.

This is why many PMCC traders increase position count during volatility spikes, the income generation improves dramatically.

Liquid, Large-Cap Underlyings

PMCCs work best on stocks and ETFs with robust options markets. Think SPY, QQQ, AAPL, MSFT, NVDA, names with thousands of contracts traded daily and tight spreads.

Smaller stocks with illiquid options create problems. Wide spreads on both the LEAPS and short calls eat into profitability. Poor fills compound into significant cost over multiple roll cycles.

Match the strategy to appropriate underlyings. Not every stock deserves a PMCC just because it has options.

Building Your PMCC System

Implementing PMCCs requires systematic process, not ad-hoc position selection.

Step 1: Screen for Candidates

Start with liquid underlyings you'd actually want to own. This isn't about finding the highest premium, it's about finding quality names with favorable options markets.

Check average daily options volume (target 10,000+ contracts), bid-ask spreads on LEAPS (under $0.40), and bid-ask spreads on monthly options (under $0.15). If the options market doesn't meet these liquidity thresholds, move on regardless of how attractive the stock looks.

Step 2: Calculate Maximum Risk

Before entering any PMCC, know your maximum risk. It's the LEAPS cost minus any collected premium. If you're buying a $32 LEAPS and selling a $1.50 call, your initial risk is $30.50 ($3,050 per contract).

Can you afford to lose that amount if the underlying collapses? If not, reduce position size or skip the trade. Maximum risk isn't theoretical, stocks can and do gap down 20-30% on earnings disasters or major news.

Step 3: Document Your Management Rules

Decide before entering the position: When will I roll short calls? (I roll at 50-75% profit or when challenged 10-14 days before expiration.) When will I roll the LEAPS? (When time remaining drops below 9 months.) When will I exit completely? (If underlying thesis breaks or position loses more than X amount.)

These rules prevent emotional decisions during market stress. You're following a playbook, not making it up as markets move against you.

Step 4: Track Performance Properly

PMCCs have two distinct P&L components, the LEAPS value change and cumulative premium collected. Track both separately.

Over a 6-month period, your LEAPS might be down $400 while you've collected $900 in short call premium. Your net P&L is +$500, but looking only at the LEAPS shows a loss. Proper accounting captures the full strategy performance.

I maintain a simple spreadsheet tracking: LEAPS purchase price, current LEAPS value, total premium collected, net P&L, and return on deployed capital. This takes five minutes monthly and prevents misunderstanding position profitability.

Position Sizing Reality Check

The capital efficiency of PMCCs creates a dangerous temptation: overleverage.

You can run three PMCCs for the same capital as one covered call. But should you? Usually not.

Position sizing should remain constant whether you're using shares or PMCCs. If you'd normally allocate $10,000 to a stock position (one covered call), deploy that same $10,000 across 2-3 PMCCs on different underlyings, not 5-6 PMCCs on the same underlying.

The freed capital should create diversification, not concentration. You're spreading risk across more positions while maintaining similar total exposure to any single name.

Think of PMCC capital efficiency as a risk reduction tool, not a leverage amplifier. Your total portfolio Greek exposure, delta, theta, vega, should stay consistent whether you're running covered calls or PMCCs. The mechanics change, the risk profile shouldn't.

What Success Actually Looks Like

PMCCs don't generate explosive returns. They generate consistent, moderate returns with less capital deployment.

A well-managed PMCC might return 3-5% monthly on deployed capital during favorable conditions. That's 36-60% annualized, though you won't maintain peak performance every month. Realistically, expect 20-30% annual returns on deployed capital with proper position selection and management.

Compare this to covered calls generating 12-18% annually on significantly more capital. The absolute dollars might look similar, but the PMCC freed up capital for other uses.

Or compare to shares alone, which historically return 8-10% annually. The PMCC amplifies returns through premium collection, but you're accepting time decay risk and more active management requirements.

Success isn't measured by individual position returns. It's measured by portfolio-level capital efficiency, how much return you generate per dollar of deployed capital across all positions.

Building This Into Your Income Strategy

PMCCs work best as one component of a diversified income approach, not as your entire portfolio strategy.

I run PMCCs alongside traditional covered calls, cash-secured puts, and credit spreads. Each strategy serves different market conditions and capital efficiency goals. PMCCs dominate when I want equity exposure with income overlay using minimal capital.

The income generated from PMCCs provides portfolio cash flow for living expenses, position adjustments, or reinvestment into new opportunities. But I'm not dependent on any single strategy performing perfectly every month.

Think of PMCCs as a tool in your options income toolbox. Sometimes it's the perfect tool for the job. Sometimes a different approach, shares, covered calls, vertical spreads, makes more sense for specific underlyings or market conditions.

The flexibility to choose the right structure for each position matters more than forcing everything into PMCC format just because the capital efficiency looks attractive.

If you want to see how this works in practice, I run five distinct portfolios in my Wealth Without Shares service, tracking real PMCC and LEAPS positions with full transparency on entries, exits, rolls, and management decisions. No hypotheticals, just systematic execution of these strategies with real capital. Check out Wealth Without Shares if you want to see the frameworks in action.

The Honest Assessment

PMCCs aren't magic. They're a capital-efficient way to run a proven income strategy using less capital than traditional covered calls.

You'll spend more time managing positions than with simple share ownership. You'll face roll decisions, strike selection choices, and early assignment risks that don't exist with covered calls. You'll need to understand options mechanics beyond basic call buying.

But in exchange, you free up 60-70% of capital requirements while maintaining similar income generation. You diversify across more positions, reduce concentration risk, and maintain flexibility to deploy capital opportunistically.

For traders willing to invest the time learning proper management and executing systematically, PMCCs deliver meaningful capital efficiency advantages. For those wanting passive income with minimal attention, traditional covered calls or dividend stocks make more sense.

Know which trader you are before committing capital to Poor Man's Covered Calls. The strategy rewards active management and systematic discipline, qualities that not every investor possesses or wants to develop.

But if you're willing to put in the work, PMCCs offer one of the most practical applications of options for income generation with improved capital efficiency. Master the mechanics, respect the risks, and execute with discipline. That's how you turn capital efficiency into consistent portfolio returns.

Probabilities over predictions,

Andy Crowder

🎯 Ready to Elevate Your Options Trading?

Subscribe to The Option Premium, a free weekly newsletter delivering:

✅ Actionable strategies.

✅ Step-by-step trade breakdowns.

✅ Market insights for all conditions (bullish, bearish, or neutral).

📩 Get smarter, more confident trading insights delivered to your inbox every week.

📺 Follow Me on YouTube:

🎥 Explore in-depth tutorials, trade setups, and exclusive content to sharpen your skills.

📘 Join the conversation on Facebook.

Disclaimer: This is educational content only. Not investment, tax, or legal advice. Options involve risk and aren't suitable for all investors. Examples are illustrative. Real results will vary. Talk to professionals before you risk real money.

Reply