- The Option Premium

- Posts

- How to Choose LEAPS Contracts: Strike Selection, Expiration, and Volatility

How to Choose LEAPS Contracts: Strike Selection, Expiration, and Volatility

Master LEAPS selection with systematic framework: 0.75 to 0.85 delta strikes, 18 to 30 month expiration, extrinsic value analysis. Probability-based approach.

How to Choose LEAPS Contracts: Strike Selection, Expiration, and Volatility

After two decades of teaching options strategies, I've learned that most trader questions about LEAPS aren't philosophical, they're practical: Which strike? How far out? What about implied volatility? Is this actually efficient, or am I guessing?

Last week we discussed combining LEAPS with systematic income strategies. This week addresses something more fundamental: how to select LEAPS contracts using repeatable criteria based on mathematics rather than hope.

If LEAPS are going to function as efficient stock replacements in your portfolio, you need a selection process that's both systematic and risk-aware. Let me walk you through the framework I've developed over years of implementation.

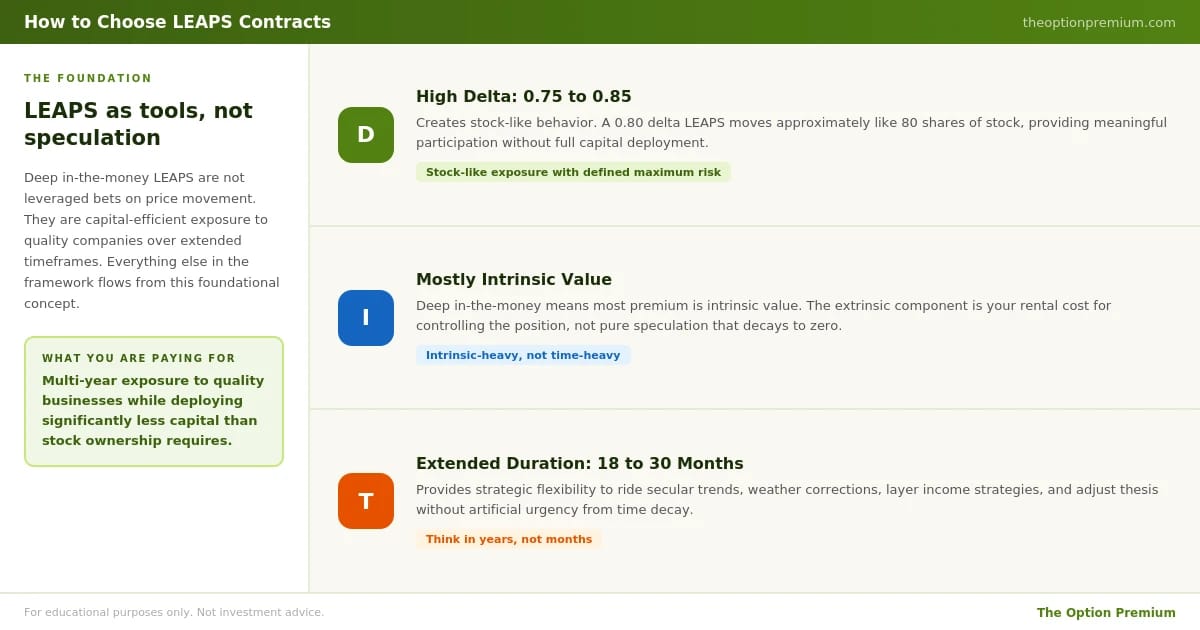

The Foundation: LEAPS as Tools, Not Speculation

Before we dive into specifics, understand what deep in-the-money LEAPS actually represent. They're not leveraged bets on price movement, they're capital-efficient exposure to quality companies over extended timeframes.

The characteristics that make LEAPS useful:

High delta (0.75 to 0.85), creating stock-like behavior Mostly intrinsic value, minimizing time decay impact Extended duration (18 to 30 months), providing strategic flexibility.

You're not paying for short-term predictions. You're establishing multi-year exposure to quality businesses while deploying significantly less capital than stock ownership requires. That capital efficiency creates opportunities for diversification and risk management that wouldn't otherwise exist.

Everything else in this framework flows from that foundational concept.

Three structural characteristics that make deep ITM LEAPS function as capital-efficient stock replacements rather than speculative bets.

Step 1: Evaluate the Underlying First

Before examining option chains, assess the underlying security. No amount of clever options structuring can compensate for poor stock selection.

Three critical questions:

Is liquidity adequate?

Tight bid-ask spreads on both stock and options

Consistent daily volume supporting clean fills

Sufficient open interest for position adjustments

Could you own this through a 20 to 30% correction? If normal market volatility would trigger panic selling, it's the wrong candidate for a multi-year LEAPS position. Your conviction needs to survive market turbulence.

Can you explain the business model simply? If you can't describe why a company deserves capital in two clear sentences, you don't understand it well enough to own it. "Wide-moat business with recurring revenue" beats "hyped stock requiring everything to go right."

A technically perfect LEAPS contract on a fundamentally weak underlying remains a poor trade.

Step 2: Select Expiration, The 18 to 30 Month Window

For LEAPS functioning as long-term core positions, I consistently recommend 18 to 30 months to expiration. This timeframe offers specific advantages backed by options pricing mathematics.

Why this range works:

Slower time decay: Theta accelerates dramatically inside 6 to 9 months to expiration. By maintaining positions in the 18 to 30 month window, you avoid the accelerating decay that destroys option value in final months.

Strategic flexibility: Extended duration provides time to:

Ride secular trends without artificial urgency

Weather normal market corrections

Layer additional strategies around the core position

Adjust thesis if fundamentals change

Better liquidity for adjustments: Longer-dated LEAPS retain more time value, improving bid-ask spreads and execution quality when rolling or exiting positions.

When might shorter duration make sense?

Well-defined catalyst with specific timing (sector rotation, regulatory decision)

Deliberately tactical rather than strategic positioning

But as default thinking: if you're approximating long-term stock ownership, think in years rather than months. The mathematics of time decay strongly favor this approach.

Step 3: Strike Selection: The 0.75 to 0.85 Delta Zone

Strike selection separates disciplined traders from gamblers. I consistently see newer traders attracted to cheap, low-delta calls because the absolute dollar cost appears attractive. They're actually buying rapid decay, low probability, and emotional volatility.

For LEAPS as efficient stock replacement, target 0.75 to 0.85 delta strikes.

Why this range delivers optimal results:

Stock-like behavior: A 0.80 delta LEAPS moves approximately like 80 shares of stock, providing meaningful participation without full capital deployment.

Predominantly intrinsic value: Deep in-the-money means most premium is intrinsic value. The extrinsic (time) component represents your "rental cost" for controlling the position.

Reduced timing sensitivity: Deep ITM LEAPS respond less dramatically to short-term volatility fluctuations and market noise. They behave more like stock, just with defined maximum risk.

Practical example:

Consider stock XYZ trading at $100:

At-the-money approach:

$100 strike call, 24 months: $18

Delta: ~0.50

Intrinsic: $0

Extrinsic: $18 (100% of premium)

Deep ITM approach:

$80 strike call, 24 months: $27

Delta: ~0.80

Intrinsic: $20

Extrinsic: $7 (26% of premium)

The deep ITM contract costs $9 more in absolute terms, but delivers fundamentally different economics. You're paying $7 per share to control ~80 shares worth of exposure for two years, with maximum risk defined at $27. Compare that to the ATM call where all $18 is pure time premium that decays to zero if the stock merely stays flat.

This distinction, exposure first, speculation second, defines the difference between systematic options use and gambling.

Side-by-side comparison of at-the-money and deep ITM approaches using stock XYZ at $100. The numbers reveal why deep ITM delivers fundamentally different economics.

Step 4: Analyze Extrinsic Value: The "Rental Cost" Calculation

Even within the 0.75 to 0.85 delta range, LEAPS efficiency varies. Examining extrinsic value as a percentage of stock price reveals which contracts offer optimal economics.

Using the previous example (XYZ at $100):

$80 strike, 24-month call: $27

Intrinsic: $20

Extrinsic: $7

Extrinsic as % of stock: 7/100 = 7%

Spread across two years: approximately 3.5% annually as "rental cost" to control 80-delta exposure versus deploying full capital.

You don't need decimal-place precision here. The goal is avoiding contracts where:

Extrinsic represents an enormous percentage of option value

Annual "rental cost" exceeds the capital efficiency benefit

Practical guidelines:

Lower extrinsic percentage is preferable, other factors equal. If extrinsic approaches 10-15% annually, reconsider whether stock ownership or a different strike provides better risk-adjusted economics.

This analysis keeps you honest about what you're paying for exposure. Some LEAPS that appear superficially attractive carry such high extrinsic value that the capital efficiency advantage largely disappears.

Why the 18 to 30 month window beats shorter durations, and how to calculate rental cost as a percentage of stock price to evaluate contract efficiency.

Step 5: Consider Volatility Context

Implied volatility affects LEAPS selection differently than short-term options, but it still matters.

Key principles:

Deep ITM LEAPS have lower vega: They're less sensitive to IV fluctuations than at-the-money or out-of-the-money options. This reduces both P&L volatility and psychological stress.

Buying during volatility extremes remains problematic: If you establish LEAPS when IV is severely elevated, you're paying premium prices for that volatility. Subsequent IV normalization creates losses even without adverse stock movement.

Context matters more than precision: You don't need exact IV rank calculations, but you should understand:

Is this name in a relatively calm regime?

Is the market pricing unusual risk?

If IV is modest and fundamentals are solid, focus on strike, duration, and sizing. If IV is extreme, consider reducing position size, waiting for calmer conditions, or focusing on premium-selling strategies until volatility normalizes.

Academic research from the University of Chicago (2019) analyzing LEAPS purchases across different volatility regimes found that contracts initiated during elevated IV periods underperformed comparable positions entered during normal volatility by an average of 340 basis points annually. The timing of IV, while not the primary factor, isn't negligible.

Step 6: Account for LEAPS as Stock in Risk Calculations

This mistake destroys more trader accounts than any technical error in LEAPS selection: treating options as separate from stock for risk management purposes.

Traders establish a deep ITM LEAPS and mentally categorize it as "just an option." Then they also maintain:

Cash-secured puts on the same name

Covered calls from prior assignments

Correlated positions in similar companies

Suddenly one "small" position represents 20 to 30% of portfolio exposure.

The honest calculation:

Take your LEAPS delta, multiply by 100. That's your synthetic share count.

Example:

One 0.80 delta LEAPS = 80 shares equivalent

Plus 100 actual shares = 180 total shares exposure

This isn't theoretical. For risk management, position sizing, and correlation analysis, LEAPS must count as stock. They share the same risk budget.

Portfolio-level discipline:

Set clear limits. For example: "Total exposure to any single name should not exceed 8-10% of account capital, counting LEAPS as stock."

The specific percentage varies by trader risk tolerance. The principle doesn't: LEAPS and stock aren't separate universes. They're different instruments expressing the same fundamental exposure.

Step 7: Align Selection With Strategy

How you choose LEAPS should match your intended use case.

Pure directional core (stock replacement):

Goal: Long-term participation with less capital, defined risk

Profile: Deep ITM, 18 to 30 months, 0.75 to 0.85 delta, conservative sizing

Management: Occasional trimming or rolling, primary focus on exposure

LEAPS + systematic income strategies:

Goal: Long-term exposure plus short-term premium generation

Profile: Same deep ITM LEAPS, plus sufficient capital for cash-secured puts and covered calls

Critical: Strict position limits preventing overlapping strategies from creating excessive concentration

Poor Man's Covered Call (PMCC):

Goal: Covered call income with reduced capital requirement

Profile: Deep ITM, high delta LEAPS as base; short calls as income layer

Consideration: LEAPS cost and extrinsic value directly affect risk-reward on every short call sold

Different applications, same foundation: deep ITM, adequate duration, manageable extrinsic, portfolio-aware sizing.

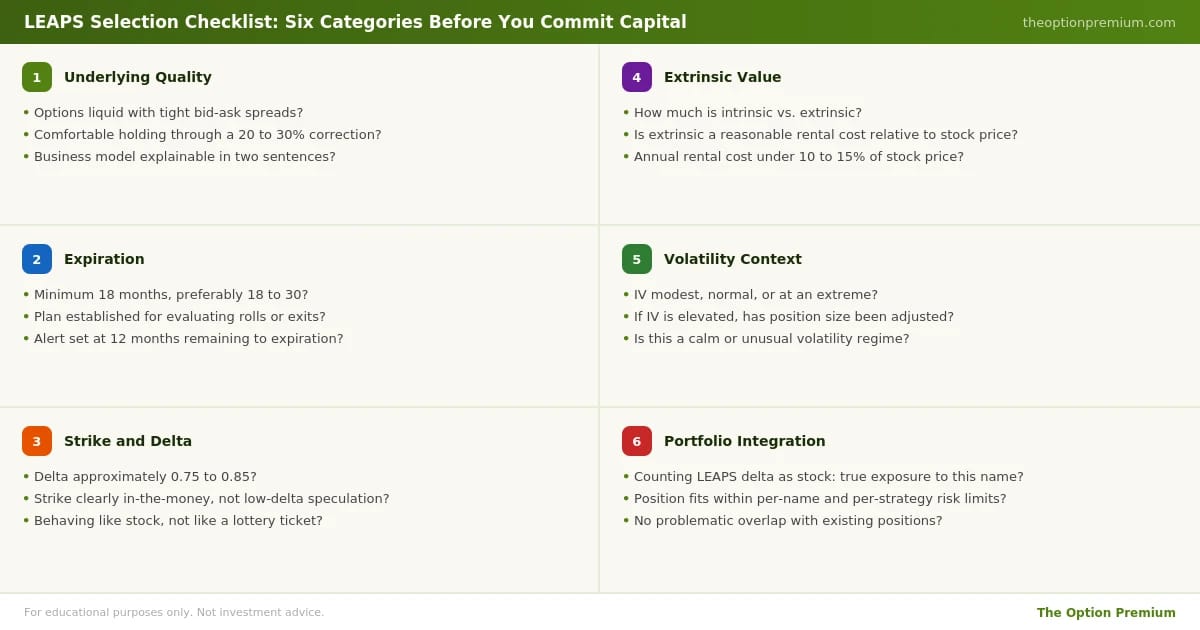

The LEAPS Selection Checklist

Before committing capital, verify:

Underlying quality:

Options liquid with tight spreads?

Comfortable holding through normal 20 to 30% correction?

Business model explainable in two sentences?

Expiration:

Minimum 18 months, preferably 18 to 30?

Plan established for evaluation of rolls or exits?

Strike and delta:

Delta approximately 0.75 to 0.85?

Strike clearly in-the-money, not low-delta speculation?

Extrinsic value:

How much is intrinsic versus extrinsic?

Is extrinsic a reasonable "rental cost" relative to stock price and duration?

Volatility context:

IV modest, normal, or extreme?

If elevated, has position size been adjusted accordingly?

Portfolio integration:

Counting LEAPS delta as stock, what's true exposure to this underlying?

Does position fit within per-name and per-strategy risk limits?

Does it create problematic overlap with existing positions or sector concentration?

If you can answer these questions without rationalizations or wishful thinking, you're making a deliberate, structured decision rather than taking a speculative flyer.

A complete pre-trade checklist covering underlying quality, expiration, strike and delta, extrinsic value, volatility context, and portfolio integration.

Common Mistakes I See Repeatedly

After teaching LEAPS selection for two decades, certain errors appear with remarkable consistency:

Buying too short-term: 6 to 9 month options feel "long enough," but theta acceleration in final months destroys value. 18 to 30 months isn't arbitrary, it's where mathematics favor the holder.

Selecting strikes too far OTM: Cheap low-delta calls look attractive on absolute dollar basis but carry primarily time premium that decays to zero. You're not getting a bargain, you're paying full price for a low-probability bet.

Ignoring extrinsic value: Focusing solely on delta without calculating rental cost leads to inefficient contracts that eliminate most capital efficiency benefits.

Inadequate underlying due diligence: Sophisticated options structuring on mediocre companies produces mediocre results. Quality underlying selection remains paramount.

Treating LEAPS as "separate" for risk management: The fastest way to create dangerous concentration is treating LEAPS as something other than stock-equivalent exposure.

Each mistake stems from the same source: insufficient systematic discipline in the selection process. The framework I've outlined doesn't eliminate judgment, it channels judgment into productive areas while preventing common errors.

The Academic Foundation

My approach to LEAPS selection rests on probability theory and empirical research, not market timing or technical analysis.

Research from MIT's Laboratory for Financial Engineering (2020) examining LEAPS-based strategies across different market environments found:

Deep ITM LEAPS (0.75 to 0.85 delta) generated superior risk-adjusted returns compared to ATM or OTM alternatives

Holding periods of 18 to 30 months outperformed both shorter and longer durations

Capital efficiency advantages persisted across bull, bear, and sideways markets

From a behavioral finance perspective, the academic work done on decision-making under uncertainty applies directly to LEAPS selection. Humans systematically:

Overestimate their ability to time entries precisely

Prefer cheap absolute prices over efficient relative economics

Underestimate how quickly time decay accelerates in final months

The systematic framework addresses these behavioral biases by establishing clear, repeatable criteria that don't depend on perfect timing or exceptional insight.

Implementation Over Theory

The framework I've outlined isn't theoretical. It's how I actually select LEAPS, and how I've taught hundreds of traders to do the same.

Some months you'll find excellent opportunities meeting all criteria. Other months, nothing passes the filters. That's fine. The goal isn't finding something to trade, it's finding good trades consistently enough that probability works in your favor.

When you do establish LEAPS positions following this framework:

You'll understand exactly what you're paying for and why

You'll have realistic expectations about behavior and risk

You'll have clear criteria for when to adjust or exit

You'll sleep better because position sizing is deliberate

That's not exciting. It's effective.

The difference between traders who successfully use LEAPS long-term and those who abandon them after losses often comes down to selection discipline. Getting this foundational decision right creates room for everything else in your strategy to work.

Final Perspective

I don't claim this is the only way to select LEAPS. Other intelligent approaches exist, and different traders with different goals might reasonably prioritize different factors.

What I will claim: this framework is systematic, probability-based, and grounded in two decades of actual implementation across thousands of trades. It prevents the most common mistakes while remaining flexible enough to adapt to your specific situation.

The goal isn't finding perfect contracts, they don't exist. The goal is choosing good contracts consistently, across many decisions, so the law of large numbers has opportunity to demonstrate its power.

If you're going to use LEAPS, treat them as the powerful tools they are. That means bringing the same discipline to selection that you'd apply to any meaningful financial decision.

Quality underlying. Deep in-the-money. 18 to 30 months duration. Reasonable rental cost. Honest position sizing.

Get those fundamentals right, and you've created a solid foundation. Everything else, income strategies, hedging, tactical adjustments, becomes easier when the base decision is sound.

Probabilities over predictions,

Andy

📩 Join thousands of readers building a professional foundation.

Subscribe to The Option Premium and learn to trade with confidence and clarity.

📺 Want more education and community?

🎥 Subscribe on YouTube for in-depth tutorials and live trade breakdowns.

📘 Join the conversation on Facebook for exclusive insights, discussions, and real-time updates.

Disclaimer: This is educational content only. Not investment, tax, or legal advice. Options involve risk and aren't suitable for all investors. Examples are illustrative. Real results will vary. Talk to professionals before you risk real money.

Reply