- The Option Premium

- Posts

- The JPM Collar: What It Is, How It Works, and Why Every Options Trader Should Understand It

The JPM Collar: What It Is, How It Works, and Why Every Options Trader Should Understand It

The JPMorgan Hedged Equity Fund runs a $21 billion put-spread collar on the SPX, resetting quarterly with ~45,000 contracts per leg. Learn the three-leg structure, the roll mechanics, and why it shapes pricing for every options trader.

Andrew Crowder

April 07, 2026

The JPM Collar: What It Is, How It Works, and Why Every Options Trader Should Understand It

If you spend any time in options trading circles, you've heard the phrase "the JPM Collar resets today" whispered like a weather warning before a storm. Every quarter, on the last business day, one of the largest single options trades in the world rolls over, and the ripple effects touch everything from SPX futures to VIX pricing to how your own credit spreads behave during expiration week.

The trade belongs to the JPMorgan Hedged Equity Fund (ticker: JHEQX), a roughly $21 billion fund that holds a portfolio of S&P 500 stocks and hedges the entire position using a massive options collar on the SPX index. It's not a secret trade. It's filed with the SEC. JP Morgan publishes the strategy in the fund's prospectus. But understanding what it actually is, how the mechanics work, and why a single fund's quarterly options roll can move the entire market is something most traders never take the time to learn.

This article breaks down the structure, the mechanics, and why it matters for your trading.

What the JPM Collar Actually Is

The JPMorgan Hedged Equity Fund uses a strategy called a put-spread collar. The fund holds a portfolio of large-cap U.S. stocks that closely mirrors the S&P 500 (about 155 holdings as of early 2026). On top of that equity portfolio, they layer an options overlay designed to protect the downside while still allowing for moderate upside participation.

The options overlay has three legs, all on the SPX index with quarterly expirations.

Leg 1: Buy an out-of-the-money put (approximately 5% below current SPX). This is the downside protection. If the S&P 500 drops more than 5% during the quarter, this put starts gaining value, offsetting losses in the equity portfolio.

Leg 2: Sell a further out-of-the-money put (approximately 20% below current SPX). This is the floor of the protection. By selling this put, the fund gives up protection below the 20% decline level and collects premium that helps pay for the closer put. The net effect: the fund is protected between a 5% and 20% decline in the S&P 500. Below 20%, the fund is exposed again.

Leg 3: Sell an out-of-the-money call (approximately 3-5% above current SPX). This is the cap on upside. By selling this call, the fund collects premium that (combined with the sold put premium) pays for most or all of the purchased put, making the entire collar structure roughly "zero cost." The trade-off: the fund's upside is capped at roughly 3.5-5.5% per quarter.

The net result, as JP Morgan describes it: "This downside hedge is in place from the S&P 500 Index falling down 5% to 20%, while allowing for upside participation in the average range of 3.5-5.5%."

The entire structure resets every quarter on the last business day. The old collar expires, and a new one is established with fresh strikes based on the current SPX level.

The three-leg structure of the JPM Collar. Leg 1: buy a put ~5% below current SPX for downside protection (this is the expensive piece). Leg 2: sell a put ~20% below to give up protection past -20% and collect premium that helps fund Leg 1. Leg 3: sell a call ~3-5% above current SPX to cap upside at 3.5-5.5% per quarter and generate the remaining premium needed to make the entire structure roughly zero cost. The net result: the fund is protected between a 5% and 20% decline, upside is capped, and the collar costs nearly nothing to maintain.

Why the Size Matters

This isn't a retail trader putting on 10 contracts. The JHEQX fund manages approximately $21 billion in assets. JP Morgan also runs two additional series of the same fund (Hedged Equity Fund 2 and 3), which follow the same strategy but reset on different quarterly months, adding to the total notional.

When the flagship JHEQX collar rolls, it typically involves roughly 40,000-45,000 contracts per leg on the SPX. At the current SPX level around 5,600-5,700, each SPX contract represents roughly $560,000-$570,000 of notional exposure. Multiply that by 45,000 contracts and you're looking at billions of dollars in notional options exposure being established in a single trading session.

This scale means the trade doesn't just participate in the market. It influences the market. The sheer volume of options being bought and sold on a single day creates flows that dealers must hedge, and those hedging flows ripple through SPX futures, the VIX, and the broader options market.

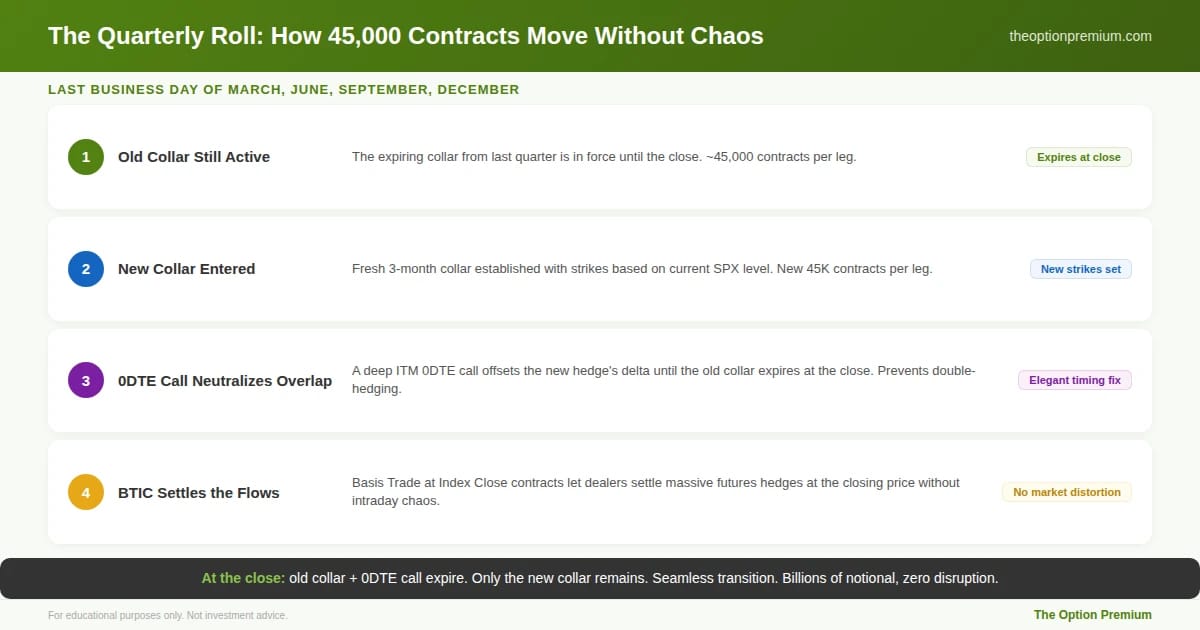

How the Quarterly Roll Works (and the 0DTE Call Trick)

The quarterly roll is where it gets mechanically interesting. On the last business day of the quarter, the old collar is expiring and the new collar needs to be established. But there's an overlap problem.

The overlap. For a few hours on roll day, the fund would theoretically have two collars in place: the old one (still active until the close) and the new one (just established). This would make the fund "double-hedged," distorting its intended exposure.

The solution: the 0DTE call. To neutralize the overlap, the fund pairs the new collar entry with a deep in-the-money 0DTE (zero days to expiration) call option that expires at the close that same day. This call offsets the new hedge's delta until the old collar expires. At the close, both the old collar and the 0DTE call expire, leaving only the new collar in place. It's an elegant mechanical solution to a complex timing problem.

The BTIC mechanism. Rather than dumping massive futures orders into the live market during the final minutes (which would cause extreme price distortion), the fund and its dealers use BTIC (Basis Trade at Index Close) contracts. These are essentially agreements to trade futures at the closing price, allowing the enormous hedging flows to settle without creating intraday chaos.

How 45,000 contracts per leg roll without causing market chaos. Step 1: the old collar is still active until the close. Step 2: the new collar is entered with fresh strikes based on the current SPX level. Step 3: a deep ITM 0DTE call offsets the new hedge's delta until the old collar expires, preventing a brief period of double-hedging. Step 4: BTIC (Basis Trade at Index Close) contracts let dealers settle massive futures positions at the closing price. At the close, both the old collar and the 0DTE call expire, leaving only the new collar in place.

What Happens to the Market on Roll Day

The quarterly roll creates predictable market effects that every options trader should be aware of.

Gamma pinning near expiration. In the days leading up to the quarterly roll, the enormous size of the expiring collar can cause the SPX to "pin" near the strike prices of the collar's legs. When tens of thousands of contracts exist at a specific strike, the delta hedging activity of dealers creates buying pressure below the strike and selling pressure above it, effectively magnetizing the index toward that level.

Volatility suppression. The continuous sale of call premium (selling vega to the market) structurally suppresses implied volatility at the 3-month tenor. When JHEQX sells 45,000 OTM calls every quarter, that's a massive supply of vega hitting the market. This is one reason why quarterly IV Percentile readings can be lower than you'd expect based on actual market uncertainty.

Skew flattening. The collar trade provides supply in both wings of the options market (selling calls and selling far OTM puts), which tends to flatten the volatility skew. For premium sellers running iron condors, this means the put-call skew you're selling into may be partially shaped by the JPM collar's structural flows, not purely by genuine market sentiment.

Massive delta hedging. Every time the SPX moves, the dealers who are on the other side of the JPM collar must adjust their hedges. With 45,000 contracts per leg, even a minimal delta change of 0.01 can require dealers to buy or sell hundreds of ES (S&P 500 E-mini futures) contracts. These hedging flows can amplify intraday moves, particularly during the final week before expiration.

The collar's $21 billion notional creates four structural effects on the SPX options market. Gamma pinning: 45,000 contracts at a single strike create a magnetic effect, with dealer hedging pushing SPX toward the strike near expiration. Volatility suppression: continuous call premium sales (selling vega) structurally compress 3-month implied volatility. Skew flattening: selling both OTM calls and far OTM puts flattens the standard vol smirk, affecting iron condor pricing. Delta hedging: a 0.01 delta change across 45,000 contracts forces hundreds of ES futures to be bought or sold, amplifying intraday moves.

How the Fund Has Actually Performed

The fund's track record demonstrates exactly what the collar is designed to do: reduce drawdowns at the expense of some upside.

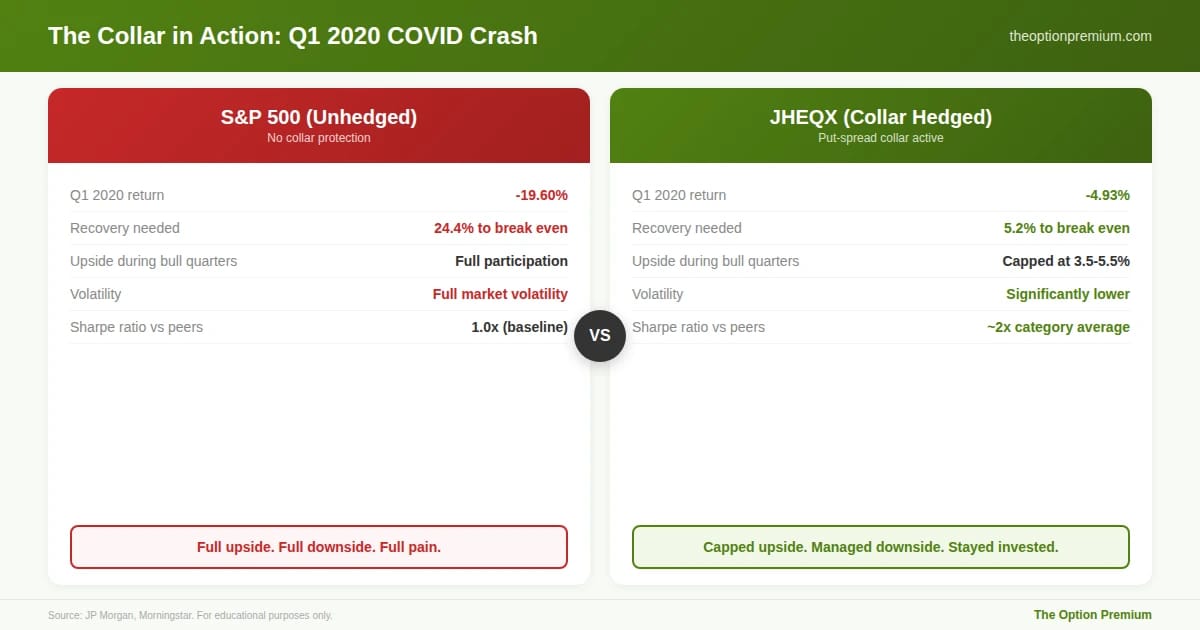

COVID crash (Q1 2020). The S&P 500 fell 19.6% in the first quarter. The fund was down only 4.93%. The put spread kicked in as the market crossed the 5% decline threshold, and the protection between 5% and 20% absorbed most of the loss. This is the scenario the collar is built for.

Bull market periods. During strong quarters where the S&P 500 returns 8-12%, the fund typically captures 3-5% because the short call caps the upside. Over multi-year periods, the fund has delivered lower absolute returns than the S&P 500 but with meaningfully lower volatility and significantly smaller drawdowns.

The Sharpe ratio tells the story. According to Morningstar, JHEQX's risk-adjusted return (Sharpe ratio) has nearly doubled its average category peer over extended periods. The fund doesn't beat the market. It beats the market on a risk-adjusted basis, which is what the collar is designed to accomplish.

The collar in action during its designed scenario. Q1 2020 (COVID crash): the S&P 500 fell 19.60%, requiring a 24.4% gain to recover. JHEQX, protected by the put-spread collar, fell only 4.93%, needing just 5.2% to get back to even. The trade-off is visible in bull quarters: the fund's upside is capped at 3.5-5.5% while the S&P 500 participates fully. Over time, the Sharpe ratio (risk-adjusted return) has nearly doubled the category average. The fund doesn't beat the market. It beats the market on a risk-adjusted basis.

Why Individual Options Traders Should Care

Even if you'd never invest in JHEQX, the collar's existence affects your trades in several concrete ways.

Strike-level support and resistance. The collar strikes on the SPX often act as magnets for price, especially as expiration approaches. If you trade SPY credit spreads or iron condors, knowing where the JPM collar strikes are gives you additional context for where the market is likely to find support (the long put strike) or resistance (the short call strike).

Quarterly expiration week behavior. The last week of each quarter can exhibit unusual price behavior as the collar's gamma and delta effects intensify. If your credit spreads expire during the same week as the JPM collar, you may see more "pinning" action than usual, where the SPX gravitates toward a specific level and stays there.

Volatility surface distortions. The collar's continuous vega supply at the 3-month point means that quarterly-expiry SPX options may be priced differently than they would be without the collar's influence. If you're selling 3-month options on the SPX, part of the IV you're selling is shaped by JPM's structural flow, not just by market expectations.

Roll day awareness. On the last business day of each quarter, the options market sees unusual flow. Spreads may widen. Implied volatility may shift. Price may exhibit unusual intraday behavior as the old collar expires and the new one is established. Knowing this date in advance (it's always predictable) lets you avoid entering new positions during the most distorted hours.

The Broader Lesson: Mechanical Flow Moves Markets

The JPM Collar is the clearest example of a structural, mechanical options flow that moves the market independently of fundamentals, sentiment, or economic data. The fund doesn't change its strategy based on whether it thinks the market will go up or down. It resets the collar every quarter, mechanically, regardless of market conditions.

This is important because it reminds us that the options market isn't purely driven by directional views. A significant portion of the flow, especially in SPX and VIX options, comes from systematic hedging programs like JHEQX. These flows are predictable, repeatable, and massive. Understanding them gives you context that most traders lack.

For premium sellers specifically, the JPM collar reinforces a principle we return to constantly: the market for options is influenced by supply and demand dynamics that go far beyond the question of "will the stock go up or down?" When $21 billion in equity is being hedged by a single collar structure, the pricing, the skew, and the behavior of SPX options are all shaped by that flow. Trading with awareness of these structural forces is a meaningful edge.

The Practitioner Edge: How I Use JPM Collar Awareness

Know the roll dates. Last business day of March, June, September, and December. I avoid entering new quarterly-expiry SPX positions on these days because the flow distortion can create unfavorable fills.

Track the collar strikes. Multiple sources publish the estimated strike levels after each quarterly roll. The short call acts as a resistance level for the quarter. The long put strike acts as a support level. These aren't hard ceilings and floors, but they provide an additional data point for where the market may gravitate.

Adjust for volatility suppression. If 3-month SPX implied volatility seems "too low" given the macro environment, part of the explanation may be the JPM collar's structural vega supply. This doesn't mean IV is "wrong." It means there's a non-fundamental reason for the pricing.

Recognize the pinning effect during the final week. If SPX is trading near one of the collar strikes in the last 5-7 days of the quarter, expect it to oscillate around that level more than usual. This is the gamma effect of tens of thousands of contracts at a single strike.

Risk Reality Check

The JPM Collar is not a magic indicator. The strikes don't always hold. In Q1 2020, the market blew through the put strike as the COVID crash accelerated. In strong bull quarters, the market can rally past the short call strike and keep going. The collar is a structural force, not an impenetrable barrier.

It's also worth noting that as the fund has grown from roughly $2 billion at inception to over $21 billion today, its market impact has increased proportionally. The effects described here are stronger now than they were five years ago, and they'll evolve as the fund's AUM changes.

Key Takeaways

The JPM Collar is a put-spread collar operated by the JPMorgan Hedged Equity Fund (JHEQX), which manages roughly $21 billion. The structure: buy a 5% OTM SPX put, sell a 20% OTM put, and sell a 3-5% OTM call. Net cost is roughly zero. Protection kicks in between a 5% and 20% decline, and upside is capped at 3.5-5.5% per quarter.

The collar resets every quarter on the last business day, involving approximately 40,000-45,000 SPX contracts per leg. The roll uses a 0DTE call to neutralize the overlap between the old and new collars, and BTIC contracts to prevent intraday price distortion from massive hedging flows.

The collar's size creates predictable market effects: gamma pinning near strike prices as expiration approaches, volatility suppression at the 3-month tenor from continuous call premium supply, skew flattening from vega supply in both wings, and massive dealer delta hedging that can amplify intraday moves.

For individual traders, the collar matters because its strikes often act as support/resistance levels, quarterly expiration weeks show unusual pinning behavior, the 3-month vol surface is structurally influenced by the collar's flows, and roll days (last business day of each quarter) create temporary market distortions.

The fund's performance proves the collar works as designed: during the Q1 2020 COVID crash, JHEQX was down only 4.93% versus the S&P 500's 19.6% decline. The trade-off is capped upside during bull quarters. The Sharpe ratio has nearly doubled its category peer average.

The JPM Collar isn't just a hedge fund's quarterly options trade. It's a structural force in the S&P 500 options market that shapes pricing, behavior, and opportunities for every trader who operates in that space. Understanding it is an edge. Ignoring it is a blind spot.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply