- The Option Premium

- Posts

- The Jade Lizard: How to Sell Premium With No Upside Risk

The Jade Lizard: How to Sell Premium With No Upside Risk

A jade lizard combines a short put with a bear call spread. When the total credit exceeds the call spread width, upside risk is zero. 20-30% more premium than a cash-secured put with the same downside exposure. Setup, construction, and management.

Andrew Crowder

April 18, 2026

There's a structure in options trading that most retail traders have never heard of, and the ones who have heard of it often misunderstand what makes it genuinely useful. It's called the jade lizard, and it solves a problem that every premium seller eventually encounters: how do you collect premium on both sides of a stock without taking unlimited risk in either direction?

A short strangle does this, but the naked call side carries theoretically unlimited risk. An iron condor defines risk on both sides, but you're buying protection on the call side that you might not need, and that protection costs premium you'd rather keep. The jade lizard sits between these two structures. It gives you the rich credit of a strangle-like position on the upside, with defined risk that's structured so cleverly that, when done correctly, you have zero risk to the upside. The only risk is on the downside, just like owning stock.

That's worth understanding in detail.

What a Jade Lizard Actually Is

A jade lizard is three legs:

You sell an out-of-the-money put. You sell an out-of-the-money call. And you buy a further out-of-the-money call.

The short put is a standalone naked put. The short call and the long call together form a bear call spread (a credit spread on the call side). You're combining a naked short put with a bear call spread in the same expiration.

The combined credit from all three legs is the key to the entire structure. If the total credit received is greater than the width of the call spread, you have eliminated upside risk entirely. The worst thing that can happen on the upside is that the stock rallies through both call strikes, and you're assigned on the call spread for a loss. But because the total credit exceeds the width of that spread, the call spread loss is fully offset by the premium collected. The net result on an upside move: break even or a small profit. Not a loss.

All of your risk is on the downside. If the stock drops significantly below the short put strike, you lose money, just as you would with a naked put or a cash-secured put. But the premium collected from the call spread side reduces your effective cost basis on the downside. You're getting paid more than a standalone put seller, which gives you a wider cushion before the position becomes unprofitable.

The Construction: Real Numbers

Stock XYZ is trading at $150. IV Percentile is at 68 (elevated, good for selling). You want neutral-to-bullish exposure with premium collection on both sides.

Sell the $140 put (0.20 delta, 45 DTE): collect $2.10

Sell the $157.50 call (0.25 delta, 45 DTE): collect $1.80

Buy the $162.50 call (0.15 delta, 45 DTE): pay $0.90

Total credit: $3.00 ($300 per jade lizard)

Call spread width: $5.00 ($162.50 minus $157.50)

The critical test: Is the total credit ($3.00) greater than the call spread width ($5.00)? No. $3.00 is less than $5.00. This means there IS upside risk. If the stock rallies above $162.50, you'd lose $5.00 on the call spread minus the $3.00 credit = $2.00 loss.

This is not a proper jade lizard. Let me adjust.

Revised construction with tighter call spread:

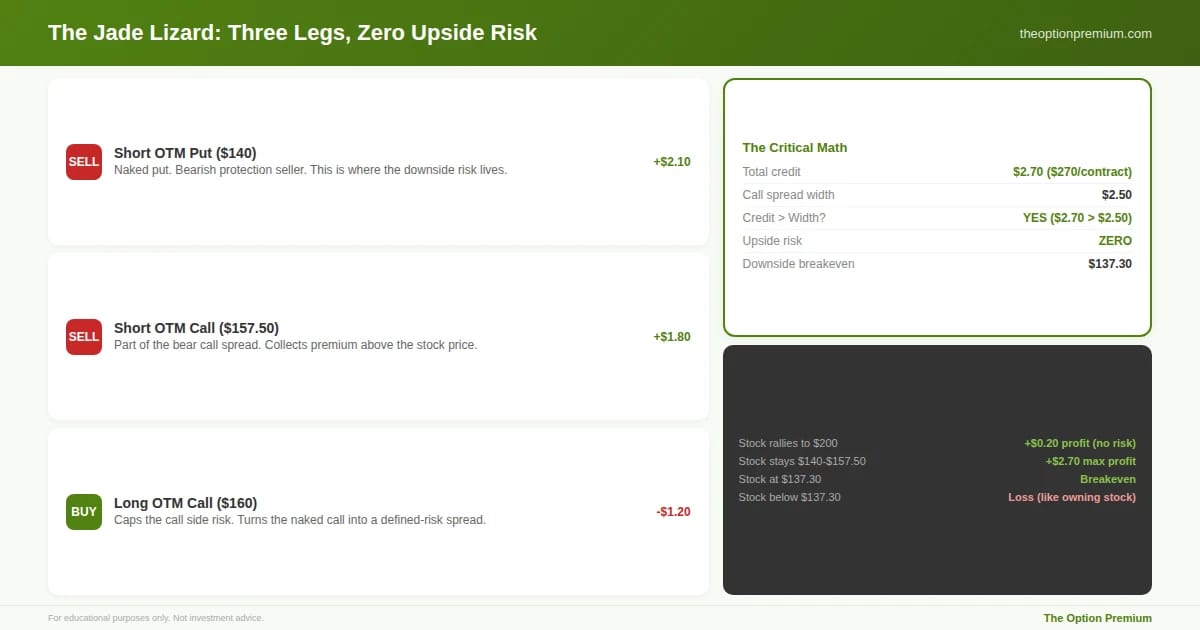

Sell the $140 put: collect $2.10

Sell the $157.50 call: collect $1.80

Buy the $160 call: pay $1.20

Total credit: $2.70 ($270 per jade lizard)

Call spread width: $2.50 ($160 minus $157.50)

The critical test: Is the total credit ($2.70) greater than the call spread width ($2.50)? Yes. $2.70 exceeds $2.50 by $0.20. This means there is no upside risk. Even if the stock rallies to $500, the maximum loss on the call spread ($2.50) is fully covered by the total credit ($2.70). You'd still net $0.20 profit on an unlimited upside move.

Your risk profile:

Upside: no risk. Maximum outcome is break even to $0.20 profit regardless of how high the stock goes.

Between the strikes ($140 to $157.50): maximum profit of $2.70 ($270 per jade lizard). Both the put and call expire worthless, and you keep the entire credit.

Downside: risk begins below $140 minus $2.70 = $137.30 breakeven. Below $137.30, you lose dollar-for-dollar, just like a stock owner who bought at $137.30. The $2.70 credit acts as a buffer.

The jade lizard's three legs and the critical math that makes it work. Sell an OTM put (the downside risk leg, collects $2.10). Sell an OTM call (part of the bear call spread, collects $1.80). Buy a further OTM call (caps the call side, costs $1.20). Total credit: $2.70. Call spread width: $2.50. Because $2.70 exceeds $2.50, there is zero upside risk. If the stock rallies to any price, you net at least $0.20 profit. All risk is on the downside, with a breakeven at $137.30. Between the strikes ($140-$157.50), you keep the full $2.70.

Why the "Credit Greater Than Width" Rule Is Everything

This is the engineering principle that makes the jade lizard work. If you violate it, you've built a different structure with a fundamentally different risk profile.

When the total credit exceeds the call spread width, the call side is self-funding. The premium collected from all three legs is enough to cover the worst-case scenario on the call spread. This means the only direction that can hurt you is down. You've created a position that behaves like a cash-secured put on the downside but collects significantly more premium because of the additional credit from the call spread.

When the total credit does NOT exceed the call spread width, you have risk on both sides: downside from the naked put, and upside from the call spread. This is an entirely different risk profile. It's closer to an unbalanced iron condor than a jade lizard, and it should be sized and managed differently.

Before placing any jade lizard, do the math. Total credit minus call spread width. If the result is positive, you have no upside risk. If it's negative, adjust the strikes until it's positive, or don't place the trade.

When to Use a Jade Lizard

The jade lizard fits specific market conditions and portfolio contexts. It's not a replacement for credit spreads or iron condors. It's an additional tool for situations where those structures don't quite fit.

Neutral to moderately bullish outlook. You don't expect the stock to drop significantly, and you're comfortable with assignment on the put side if it does. You also don't expect a massive rally, but you want to eliminate upside risk entirely so you don't have to worry about a runaway move higher.

Elevated IV environment. Like all premium-selling strategies, the jade lizard works best when IV Percentile is above 50 and ideally above 65. Elevated IV produces richer credits on all three legs, making it easier to satisfy the "credit greater than width" rule. In low IV environments, the put premium and call spread premium may not be sufficient to exceed the call spread width, and forcing the structure by tightening the call spread creates a position with poor risk-reward.

Stocks you'd be willing to own. Because all the risk is on the downside, a jade lizard should only be placed on underlyings you'd be comfortable owning at the breakeven price. If the stock drops through your short put and you're assigned, your effective cost basis is the put strike minus the total credit received. Ask yourself: would I buy this stock at $137.30 (in our example)? If the answer is no, the jade lizard isn't the right structure.

When you want more premium than a cash-secured put but don't want strangle risk. A standalone cash-secured put on the $140 strike collects $2.10. The jade lizard on the same put strike collects $2.70. That's 29% more premium for the same downside risk profile, with no upside risk. The extra $0.60 comes from the call spread, and because the total credit exceeds the call spread width, that extra premium is free money on the upside.

The Management Playbook

Managing a jade lizard is simpler than managing an iron condor because you only have risk in one direction. But it still requires discipline.

Profit target: close at 50% of credit. Collected $2.70? Close the entire position when you can buy it back for $1.35 or less. This typically happens in 15 to 25 days on a 45 DTE trade in elevated IV. Closing early locks in profit and eliminates the remaining probability of touch risk on the put side.

Stop loss: 2x the total credit on the put side. Since the call side has no risk (assuming proper construction), the management focus is entirely on the put. If the short put's value increases to the point where the total position is showing a loss equal to 2x the original credit, close the position. In our example: if the jade lizard that was entered for a $2.70 credit now costs $5.40 to close, exit.

21 DTE review. At 21 days to expiration, evaluate the put side. If the stock is well above the put strike and the position is profitable, close it. If the stock has moved toward the put strike, decide whether to close, roll the put out in time for additional credit, or hold with a tighter mental stop.

10 DTE exit. Same rule as credit spreads. Gamma accelerates in the final two weeks. In most cases, close the position regardless of P&L at 10 DTE. The gamma risk on the naked put is not worth the remaining premium.

If the stock rallies hard. Do nothing. This is the beauty of a properly constructed jade lizard. If the stock rockets higher, the call spread reaches max loss, but the total credit covers it. You might see the call spread showing a large unrealized loss on your screen, but your net position is still break even or slightly profitable. Don't panic. Don't adjust. The structure is working as designed.

If the stock drops toward the put strike. This is where active management is required. You have three options: close the put for a loss (and keep the call spread profit, since it's now worthless), roll the put down and out in time for a credit (extending duration but improving the strike), or accept assignment if you're genuinely willing to own the stock at the effective cost basis.

Sizing a Jade Lizard

Because the downside risk is equivalent to a naked put (or cash-secured put), size the jade lizard based on the put side's risk, not the total credit.

If the short put is at the $140 strike on a stock at $150, your maximum risk on the downside is $140 per share (the stock goes to zero) minus the $2.70 credit = $137.30 per share, or $13,730 per jade lizard. That's the theoretical max. In practice, the position sizing question is: what's 2-5% of your account?

On a $50,000 account at 3% risk, you'd allocate $1,500 of risk. If you're using a stop loss at 2x credit ($540 loss per jade lizard), that means you can run approximately 2-3 jade lizards within your risk budget. Size based on the stop loss amount, not the theoretical maximum, because you should be closing before max loss is reached.

The margin requirement on a jade lizard is typically the greater of the naked put margin or the call spread margin, minus the credit received. This varies by broker, but it's generally more capital-intensive than a credit spread and less than a naked strangle. Check your specific broker's requirements before placing the trade.

The Jade Lizard vs. Other Structures

vs. Cash-secured put. The jade lizard collects more premium (put credit + net call spread credit) for the same downside risk. The extra premium widens your breakeven and provides a larger buffer. The trade-off is that the call spread limits your profit if the stock rallies beyond the short call strike, whereas a cash-secured put has unlimited upside participation if assigned.

vs. Short strangle. The jade lizard eliminates the unlimited upside risk of the naked call by capping it with the long call. You collect slightly less than a strangle (you're buying the long call), but you sleep better knowing a 30% overnight gap higher won't blow up the position.

vs. Iron condor. The jade lizard doesn't buy protection on the put side, so it collects more premium than an iron condor but carries more downside risk. The iron condor has defined risk on both sides. The jade lizard has defined risk only on the call side and undefined (but manageable with stops) risk on the put side.

The jade lizard is the right structure when you want more premium than a cash-secured put, less risk than a strangle, and you're comfortable with naked put exposure on a stock you'd be willing to own.

Where the jade lizard fits among premium-selling structures. It collects 20-30% more premium than a cash-secured put with the same downside exposure and zero upside risk. It eliminates the unlimited upside risk of a short strangle by capping the call side. It collects more premium than an iron condor because it doesn't buy put-side protection. The jade lizard is the right choice when you want more premium than a CSP, less risk than a strangle, and you're comfortable with naked put exposure on a stock you'd willingly own.

Risk Reality Check

The jade lizard's downside risk is real and substantial. A naked short put can produce large losses if the stock drops sharply. The 2x credit stop loss limits the damage in normal conditions, but overnight gaps (earnings announcements, geopolitical events, sector-wide selloffs) can push the loss beyond your stop before you can execute the exit.

Never place a jade lizard on a stock with earnings inside the expiration window unless you have specific experience trading earnings with this structure. Never place a jade lizard on a stock you wouldn't be comfortable owning at the effective breakeven price. And always verify that the total credit exceeds the call spread width before submitting the order. A jade lizard that violates this rule is a different animal entirely.

Key Takeaways

A jade lizard combines a short out-of-the-money put with a bear call spread (short call + long call) in the same expiration. When the total credit received exceeds the width of the call spread, there is zero upside risk. All risk is on the downside, similar to a cash-secured put but with significantly more premium collected.

The "credit greater than width" rule is the engineering principle that makes the structure work. If total credit is $2.70 and the call spread is $2.50 wide, you net $0.20 profit even if the stock rallies to infinity. If the credit doesn't exceed the width, you have upside risk and a fundamentally different position. Always do the math before entry.

The jade lizard fits neutral-to-bullish outlooks on stocks you'd be willing to own, in elevated IV environments (IVP above 50), when you want more premium than a cash-secured put but less risk than a short strangle. It collects 20-30% more premium than a standalone put for the same downside exposure.

Management focuses entirely on the put side since the call side has no risk. Close at 50% of credit. Stop at 2x credit on the put side. Review at 21 DTE. Hard exit at 10 DTE. If the stock rallies hard, do nothing. The structure handles it. If the stock drops toward the put, close, roll, or accept assignment.

Size based on the put side's risk using 2-5% of account equity, calculated against your stop loss amount (2x credit), not the theoretical maximum loss. The margin requirement is typically greater than a credit spread but less than a naked strangle. Verify with your broker before trading.

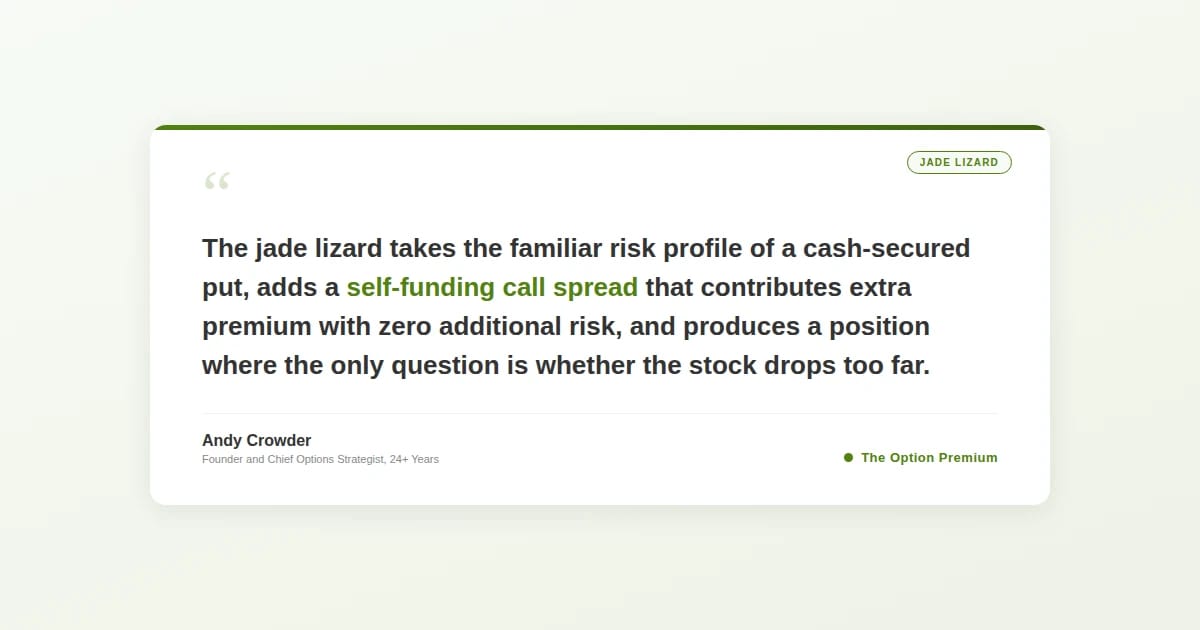

The jade lizard is one of the most capital-efficient premium-selling structures available when constructed properly. It takes the familiar risk profile of a cash-secured put, adds a self-funding call spread that contributes extra premium with zero additional risk, and produces a position where the only question is whether the stock drops too far. For a premium seller who has mastered credit spreads and is comfortable with short put exposure, the jade lizard is the natural next step.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply