- The Option Premium

- Posts

- How to Create "Synthetic Dividends" with LEAPS

How to Create "Synthetic Dividends" with LEAPS

Use LEAPS as capital-efficient "stock" and sell short calls for steady cash flow. A complete, rules-based framework for building synthetic dividends with deep-ITM LEAPS, ratio overlays, and mechanical risk management.

How to Create "Synthetic Dividends" with LEAPS

Here's something most dividend investors don't realize: you're waiting around for someone else's schedule.

Quarterly. Maybe monthly if you're lucky. The company decides when you get paid, how much, and whether they'll cut it when times get rough.

But what if you could create your own dividend schedule? What if you could generate monthly cash flow from stocks that don't pay dividends at all, Tesla, Amazon, Google, while using a fraction of the capital you'd need to own shares outright?

That's exactly what we're going to build today.

The big idea (and why it works)

We're going to use LEAPS, long-dated call options, as a capital-efficient stock replacement. Then we'll layer on short-term calls that we sell every month to create income. Think of it as building your own dividend-paying machine.

The LEAPS give you the stock exposure. The short calls give you the monthly paycheck. And you control everything: the timing, the amount of income, how much upside you keep.

Is this strategy right for you?

Let me be straight with you. This isn't for everyone.

This works best if you're tired of tying up massive amounts of capital just to get stock exposure. If you'd rather use $3,300 instead of $10,000 to control the same upside, you're in the right place.

It's also for traders who want a process, something repeatable and mechanical, instead of constantly trying to predict which way the market will move tomorrow.

And yes, you need to be comfortable with a few moving parts. We're talking about managing entries, rolling positions, and understanding what happens if you get assigned. If that sounds intimidating, spend some time with basic covered calls first. Then come back here.

But if you're nodding along thinking "this sounds exactly like what I've been looking for," then keep reading. We're about to build something powerful.

The foundation: how we're building this income machine

Alright, let's get into the mechanics. This is a variation of the Poor Man's Covered Call (PMCC), but we're optimizing it specifically for income generation. Here's the three-step framework:

Step 1: Buy your "stock replacement"

Instead of buying 100 shares, you're buying a LEAPS call option, one that expires 12 to 24 months out and sits deep in-the-money with a delta around 0.75 to 0.85.

Why deep in-the-money? Because you're paying mostly for intrinsic value (the real, stock-like value) and very little for time premium. You want this LEAPS to act like stock, not like a lottery ticket.

Step 2: Sell short-term calls against it

Every 30 to 45 days, you're going to sell an out-of-the-money call with a delta around 0.20 to 0.35. This is your monthly "dividend." You're harvesting theta, that time decay working in your favor.

Step 3: Rinse and repeat

When that short call expires worthless or you close it at 50% profit, you sell another one. The LEAPS just sits there acting like your shares. Month after month, you're pulling in premium.

LEAPS synthetic dividends three-step framework: buy deep ITM calls, sell short-term calls monthly, repeat for income.

Why deep in-the-money LEAPS change everything

Here's what most people get wrong: they buy at-the-money or slightly in-the-money LEAPS and wonder why the position feels so unpredictable.

When you go deep in-the-money, you're essentially buying synthetic stock. Higher delta means it moves more like shares. Lower vega means it doesn't swing wildly when volatility spikes. And you're not paying much time premium, so theta decay isn't quietly eating your lunch while you sleep.

That stability in your "core" position? That's what lets you confidently sell income month after month.

Choosing your strikes: where the magic happens

This is where strategy turns into execution. Get these selections right and you've got a smooth-running income engine. Get them wrong and you're fighting your position every month.

Picking your LEAPS (your synthetic shares)

Expiration: Look 12 to 24 months out. You want time on your side, not running out in six months.

Delta: Target 0.75 to 0.85. This is your "stock efficiency" zone. Too low and you're not getting enough exposure. Too high and you're overpaying for a tiny bit more delta.

The intrinsic/extrinsic split: Here's the key test, extrinsic value should be a small slice of what you're paying, typically under 10 to 15% of the total premium. If you're paying $10 for a LEAPS and $3 of that is time value? Pass. You want most of your cost to be intrinsic (real value), not hope.

Liquidity matters: Tight bid-ask spreads and real open interest. If the market's a penny wide, you're good. If it's fifty cents wide? You're donating money every time you trade.

Selecting your short calls (your monthly paychecks)

Time frame: 30 to 45 days to expiration. This is theta's sweet spot—not so short that gamma risk gets wild, not so long that you're waiting forever to collect.

Delta: 0.20 to 0.35. Think of delta as rough probability here. A 0.30 delta call has maybe a 30% chance of finishing in-the-money. That's your balance between meaningful premium and reasonable safety.

Placement strategy: Aim near or just outside the expected move for that cycle. You want premium that matters, but you're not trying to get run over either.

Exit rule: When you've captured 50% of max profit, close it. Don't wait for perfection. Take your win, redeploy into the next cycle, and let compounding work.

LEAPS options strike selection guide showing delta targets, extrinsic value limits, and short call parameters side by side.

The ratio dial: your upside versus income control

Here's where this strategy gets interesting. You don't have to run a one-to-one ratio between your LEAPS and your short calls. In fact, you shouldn't.

Think of this as a dial you can turn based on your market outlook and income goals.

Want more upside? Dial it light.

Run something like 5 LEAPS with only 2 or 3 short calls against them. You're keeping more net delta (more bullish exposure), collecting less premium, but leaving more room to profit if the stock rips higher.

This is your "I think we're going up, but I still want some monthly cash flow" setting.

Want more income and downside cushion? Dial it up.

Run 5 LEAPS with 4 or 5 short calls. Now you've got lower net delta (less bullish), you're collecting more premium each month, and you've got a bigger income cushion if things pull back.

This is your "I want steady cash flow and I'm willing to cap more upside to get it" setting.

The beautiful part? You can adjust this ratio cycle by cycle. Feeling bullish after a pullback? Go lighter on the short calls. Market feels toppy? Add an extra short call for that month.

You're not locked in. You're adapting.

LEAPS short call ratio dial showing light, balanced, and heavy coverage ratios for monthly income strategies.

Your monthly routine (keep it boring, keep it profitable)

The power of this strategy isn't in being clever. It's in being consistent. Here's what your monthly cycle looks like.

Before you sell: quick market check

Pull up your ticker's IV Rank or IV Percentile. You're hoping to see 25 or higher, that means premium is decent, not anemic. Is the trend still intact? Are the spreads still tight? Good. You're cleared for takeoff.

Selling your calls: the money moment

This is it. You're selling 30 to 45 days out, delta around 0.20 to 0.35, collecting a realistic credit based on current volatility.

Keep your size small and consistent. This isn't the trade where you suddenly decide to double down because you "feel good" about it. Small, repeatable, mechanical.

When it works (winners): take the money and run

Your short call drops to 50% of what you collected? Close it. Don't wait for it to go to zero. That last 50% takes way more time and carries way more risk than just closing, banking the win, and moving to the next cycle.

Winners take care of themselves if you let them.

When the stock runs (managing upside): roll, don't panic

So the stock rallies hard and now your short call is closer to the money than you'd like. No problem. Roll it up and out, higher strike, next expiration, for a net credit.

You're keeping your LEAPS delta intact, you're banking more premium, and you're giving yourself room to keep profiting if the rally continues.

The worst thing you can do is freeze and let a short call drift deep in-the-money into expiration without a plan. Roll early, roll often, roll for credits.

Rinse and repeat

That's it. Next month, you do it again. And the month after that. And the month after that.

Boring? Absolutely. Profitable over time? That's the whole point.

Let's talk real numbers (so you can actually feel this)

Theory is great. Let's see what this looks like with actual strikes and premiums.

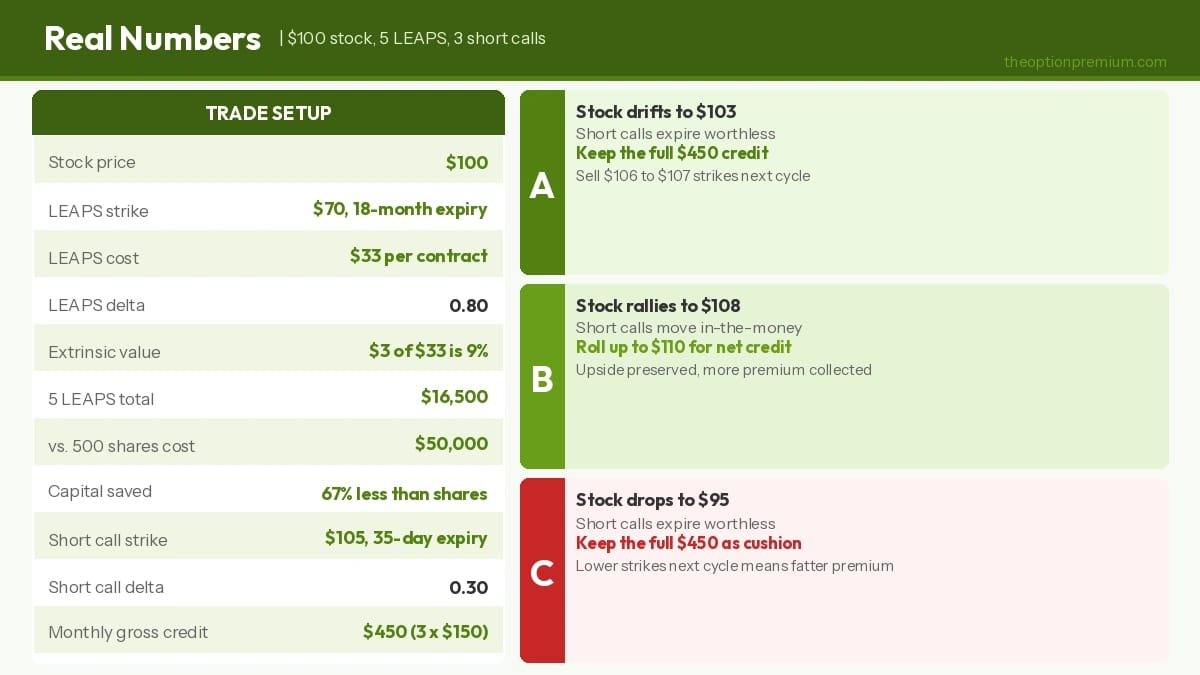

The setup

Say we're looking at a stock trading at $100.

Your LEAPS purchase:

You buy an 18-month call at the $70 strike for $33 (delta around 0.80).

Intrinsic value: $30 (the stock is $30 above your strike)

Extrinsic value: $3 (time premium)

Total capital: $3,300 per contract

Compare that to buying 100 shares at $100 = $10,000. You just controlled the same exposure for one-third the capital.

Your first short call:

You sell a 35-day call at the $105 strike for $1.50 (delta around 0.30).

If you're running a balanced ratio, say 5 LEAPS and 3 short calls, you just collected $450 in premium ($150 × 3) for this cycle.

Your LEAPS cost was $16,500 total (5 × $3,300). So you're looking at roughly $450 per month in gross credit at baseline IV. Some months will be more, some less, depending on where volatility sits.

When the stock moves

Scenario 1: Stock drifts to $103 by expiration

Your $105 calls expire worthless. You keep the full $450. Next month, you sell the $106 or $107 calls and collect again.

Scenario 2: Stock rallies to $108

Your $105 short calls are now in-the-money. No problem. Roll them up and out to $110 strikes in the next expiration, collecting a net credit to do it. You've preserved your upside, you've collected more premium, and you're still in the game.

Scenario 3: Stock drops to $95

Your short calls expire worthless. Your LEAPS have pulled back, but you're not down nearly as much as if you owned shares outright. Plus, next month you can sell lower-strike calls and collect even fatter premium thanks to the pullback.

See how this works? The income cushions the downside. The rolls preserve the upside. And month after month, you're getting paid.

LEAPS synthetic dividend real numbers example: $100 stock, 5 contracts, $450 monthly credit across three scenarios.

What about earnings and ex-dividend dates?

Good question. These events can mess with your carefully laid plans if you're not paying attention.

Earnings: to play or not to play

Here's my take: you're running an income program, not placing bets on earnings beats or misses.

Most experienced income traders do one of three things around earnings:

Skip the cycle – just don't have short calls on during earnings

Go wider – sell further out-of-the-money strikes so even a big move doesn't threaten you

Go smaller – maybe sell 2 calls instead of your usual 3

What you don't want to do is pretend earnings volatility doesn't exist and then act surprised when your position gets hammered.

Ex-dividend dates (if you're trading dividend payers)

If you've got short calls that are near or in-the-money approaching an ex-dividend date, you might get assigned early. The call holder exercises to capture the dividend.

Two ways to handle this:

Roll up and out before ex-div - avoid the assignment risk entirely

Accept the mechanics - know your account will handle it and move on

Just don't be the trader who forgets about ex-div and gets surprised by early assignment. It's avoidable if you're paying attention.

The risk stuff you need to know (seriously, read this twice)

Let's talk about what can actually go wrong. Because it can.

Your maximum risk: the LEAPS cost

If the stock goes to zero, you lose what you paid for the LEAPS. That's your capital at risk per "synthetic stock" position, not the full share price, but not zero either.

On a $100 stock, that might be $3,300 at risk instead of $10,000. Better, but still real money.

The roll rule: net credits only

When you're rolling short calls, you should be collecting more premium, not paying a debit. If you're paying to roll, something's wrong with your strike selection or timing.

Net-credit rolls improve your break-even and reduce risk. Debit rolls dig you deeper. Know the difference.

If the trend breaks, manage first

Got a clear trend filter (ADX, DMI, moving averages, whatever you use) that's flipping against you? And your short strike is getting threatened?

Don't debate the market. Manage the position. Roll, reduce, or close. You can analyze what went wrong after you're out.

Position sizing is the strategy

This is critical: keep your per-ticker exposure modest. Maybe 0.5 to 2% of your portfolio risk per "unit."

I don't care how confident you feel about a trade. The trader who sizes properly survives to trade next month. The trader who goes all-in on one ticker, doesn't always.

The liquidity tax nobody talks about

Wide bid-ask spreads will quietly destroy your returns. You think you're making $150 per contract, but after slippage on entry and exit, you're really making $90.

Stick to liquid names and ETFs where the market is tight. SPY, QQQ, AAPL, MSFT, these trade with penny-wide markets. Some small-cap stock with a fifty-cent spread? Pass.

Tax considerations (talk to a professional)

Short-call premium typically gets taxed as short-term ordinary income, your highest tax rate.

Your LEAPS might qualify for long-term capital gains treatment if held over a year, but there are special rules (straddle rules, wash sales, etc.) that can get complex fast.

And if you're doing this in an IRA or 401(k), different rules apply entirely.

Bottom line: talk to a CPA who knows options before you scale this up. Don't learn tax lessons the expensive way.

Which stocks actually work for this

Not every ticker is a good candidate. Here's what to look for.

The easy wins: major ETFs and large-caps

Start here. SPY, QQQ, DIA, IWM, these trade millions of contracts, spreads are tight, and the options chains go out two years with real liquidity.

For single stocks, think top-tier names: AAPL, MSFT, AMZN, GOOGL, NVDA, TSLA. Household names with massive option volume.

The liquidity test

Before you trade anything, check the bid-ask spread on both the LEAPS you want to buy and the near-term calls you want to sell.

Penny-wide or a few cents? You're good. Quarter-wide? Tolerable if the underlying is worth it. Fifty cents or wider? Walk away. You're giving up too much edge to the market makers.

Also check open interest. You want to see real contracts out there, not a ghost town.

Avoid the traps

Low-liquidity "story stocks" that barely trade options? Hard pass.

Penny stocks or micro-caps with wide spreads and no volume? Nope.

Biotech names that gap 40% on binary trial results? Maybe once you're experienced, but not when you're learning this strategy.

Income programs thrive on consistency and frictionless execution. Trade what's liquid, boring, and easy to manage.

Adapting to different market conditions

Markets don't stay the same. Your strategy shouldn't either. Here's how to adjust based on what the market's giving you.

Grinding uptrend (low-to-mid volatility)

This is the "don't get cute" environment. Market's moving up steadily, volatility is calm, and premiums are decent but not spectacular.

Your adjustment: Go ratio-light. Run something like 5 LEAPS to 2 short calls. You want to participate in the upside, and the market's giving you a smooth ride. Don't choke off your gains for an extra $50 in premium.

When the stock moves higher, roll your short calls up and out for a credit. Keep banking premium while maintaining upside room.

Sideways chop (mid volatility)

Market's going nowhere. Oscillating in a range. Some days it feels bullish, some days bearish, but it's basically stuck.

Your adjustment: Run a balanced ratio, maybe 5 LEAPS to 3 short calls. Place your strikes near the expected move, not too conservative, not too aggressive.

This is prime theta-harvesting territory. Collect premium, hit your 50% profit targets quickly, and redeploy. The more cycles you can run in a choppy market, the better.

Pullbacks and elevated volatility

Market's selling off, or at least threatening to. VIX is spiking, premiums are fat, and everyone's nervous.

Your adjustment: This is when you can temporarily dial up the income. Run 4 or even 5 short calls against 5 LEAPS. Premiums are rich, so you can go wider on strikes and still collect meaningful credit.

The extra income gives you a bigger cushion if the market keeps dropping. And as volatility compresses (which it eventually will), scale back to your normal ratio.

The key is flexibility. Don't lock yourself into one approach across all environments.

When to refresh your LEAPS (the maintenance nobody talks about)

Your LEAPS won't last forever, and you need a plan for when they start aging out. Here's what to watch for.

The expiration countdown

When your LEAPS drop below 9 to 12 months until expiration, start evaluating whether it's time to roll forward.

Why? Two reasons. First, time decay starts accelerating as you get closer to expiration. Second, you might start running into issues where your short calls are too close in time to your long calls, that creates risk you don't want.

The roll-forward process:

Look for new LEAPS 18 to 24 months out at a similar delta (0.75 to 0.85). Ideally, you're paying a debit that's mostly intrinsic value, not time premium.

Yes, you're paying a bit to refresh your position. But you're keeping your income engine running, and time decay on fresh LEAPS is minimal.

The delta drift problem

Sometimes your LEAPS delta drops significantly, maybe the stock pulled back hard and now your 0.80 delta LEAPS is sitting at 0.60.

This is a problem. You're not getting stock-like exposure anymore. You're getting half-stock exposure, and that changes everything about how the position behaves.

The fix: Roll down to a deeper in-the-money strike to re-establish your delta. You want that 0.75 to 0.85 zone. Don't let your LEAPS drift into mediocre delta territory just because you don't want to pay the adjustment cost.

Think of LEAPS maintenance like changing the oil in your car. It costs a bit, you'd rather not do it, but it keeps everything running smoothly for the long haul.

Five mistakes that will cost you (and how to avoid them)

Let's talk about where traders blow up this strategy. Learn from their pain.

Mistake #1: Buying at-the-money or near-the-money LEAPS

You're trying to save money on the entry, so you buy an ATM LEAPS instead of deep ITM. Seems smart, right?

Wrong. You just loaded up on extrinsic value and vega. Now your LEAPS swings wildly with volatility changes, and theta is eating your lunch. You've turned this into a directional bet instead of a stock replacement.

The fix: Go deep in-the-money. Delta 0.75 to 0.85. Keep time value minimal. Yes, it costs more upfront, but you're buying stability and predictability.

Mistake #2: Overselling short calls and choking your upside

You get greedy. "If 3 short calls pay me $450, then 5 short calls will pay me $750!" So you sell 5 calls against 5 LEAPS.

Congratulations, you just created a synthetic short position if the stock rallies. You'll spend the next month stressed, rolling for debits, and watching your LEAPS gains get eaten by short-call losses.

The fix: Use the ratio dial intelligently. 5 LEAPS to 2 or 3 short calls keeps you net-long. Only add more shorts when volatility is elevated and you specifically want that extra cushion.

Mistake #3: Letting short calls drift deep ITM without a plan

The stock rallies, your short calls go in-the-money, and you, freeze. "Maybe it'll pull back." It doesn't. Now you're five days to expiration with deeply ITM calls about to get assigned.

The fix: Roll early. When your short calls get threatened, roll them up and out for a net credit. Don't wait until expiration week. Manage early, manage often.

Mistake #4: Holding winners way too long

Your short call drops from $1.50 to $0.75. You've captured 50% profit in two weeks. But you think, "Why not wait for it to go to $0.20?"

So you wait. And wait. And then the stock bounces and suddenly that $0.75 option is back to $1.20. Now you've given back your profit and you're annoyed.

The fix: Take 50% profit and move on. You'll run more cycles, compound faster, and sleep better. The last 50% of profit takes 80% of the time and carries way more risk.

Mistake #5: Trading illiquid names because "the premium looks good"

Some stock you've never heard of shows options with seemingly fat premium. You jump in. Then you try to exit and realize the bid-ask spread is fifty cents wide and there's no volume.

You just donated a huge chunk of your edge to market makers.

The fix: Liquidity above everything. Trade names where the spreads are tight and the volume is real. SPY, QQQ, and major large-caps exist for a reason.

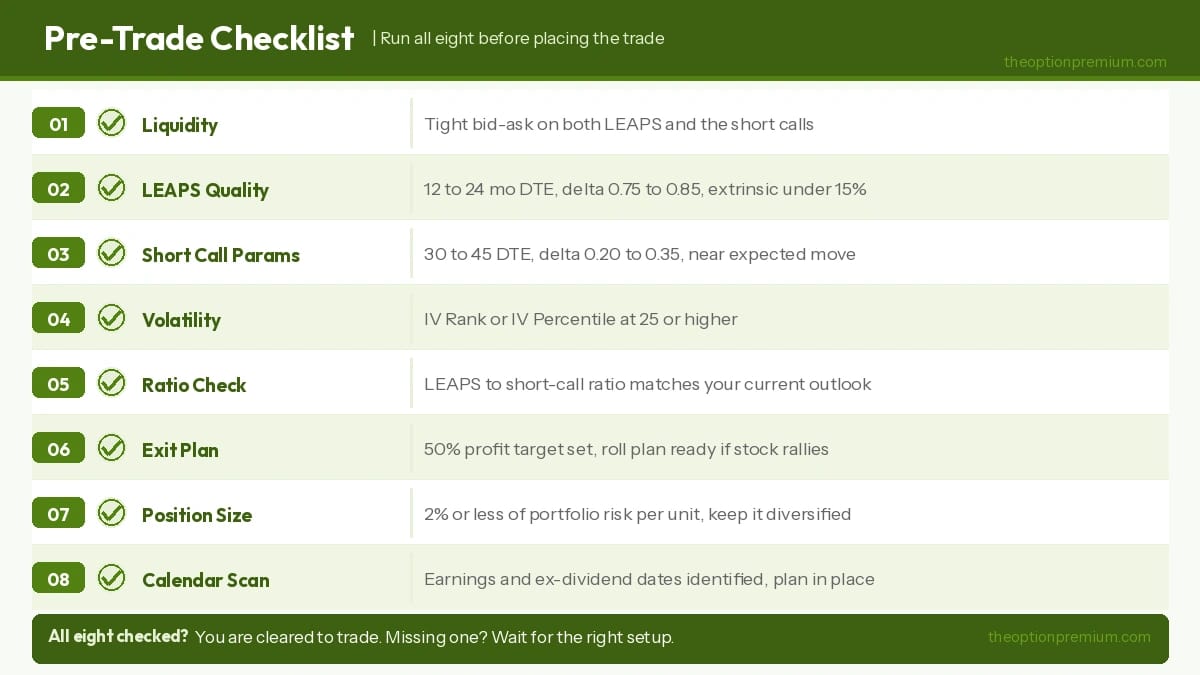

Your 60-second pre-trade checklist (use this every time)

Before you place the trade, run through this quick mental checklist. It takes one minute and will save you from most preventable mistakes.

☐ Liquidity check

Are the spreads tight on both the LEAPS and the short calls? Can you get in and out without hemorrhaging money to the bid-ask? If the answer is no, find a different ticker.

☐ LEAPS quality check

12 to 24 months to expiration? Delta 0.75 to 0.85? Extrinsic value under 15% of total premium? Good. You've got a proper stock replacement.

☐ Short call parameters

30 to 45 days out? Delta 0.20 to 0.35? Placed near the expected move? You're in the sweet spot for theta without excessive risk.

☐ Volatility check

IV Rank or IV Percentile at least 25 to 30? You're getting paid decently for selling premium. Below that and you might want to wait for a better setup.

☐ Ratio sanity check

Does your LEAPS-to-short-call ratio match your market outlook? Bullish = fewer shorts. Want more income or hedge = more shorts. Don't overthink it, but be intentional.

☐ Exit plan locked in

You're taking 50% profit on the shorts, right? And you're rolling up and out if the stock sprints higher? Good. Having a plan means you won't freeze when you need to act.

☐ Position size discipline

Is this 2% or less of your portfolio risk per unit? Are you diversified across multiple names and different expiration cycles? Size kills more traders than bad strategy.

☐ Calendar scan

Is there an earnings announcement or ex-dividend date during your short call cycle? If yes, do you have a plan for it?

Done? Then you're clear to trade.

LEAPS PMCC synthetic dividend pre-trade checklist with 8 items covering liquidity, strike selection, IV rank, and position sizing.

Questions you're probably asking right now

Let's knock out the most common questions before they keep you from getting started.

"Can I lose more money than just owning shares?"

Your maximum risk is the cost of the LEAPS, not the full share price. So on a $100 stock, you might have $3,300 at risk per contract instead of $10,000 for shares.

The risk isn't losing more than shares. The risk is poor management, overselling calls, not rolling when you should, letting positions drift into trouble. Follow the rules in this guide and you'll be fine.

"What kind of monthly return can I realistically expect?"

Here's the honest answer: it depends on the regime.

In elevated volatility environments, you might collect low-single-digit percentage returns per month on your deployed capital. When volatility compresses, those numbers drop.

The key word is consistency. Stop thinking about hitting some magic percentage every month. Think about running a repeatable process that pays you month after month, regardless of market direction.

"Should I hold through earnings announcements?"

Most income traders don't. You're running a cash-flow business, not playing the earnings lottery.

You've got three reasonable options: skip the cycle entirely, go with wider strikes to reduce risk, or reduce your position size for that month. What you shouldn't do is ignore earnings and hope for the best.

"How often do I need to replace my LEAPS?"

Typically when you drop below 9 to 12 months to expiration, or when your delta or extrinsic profile starts deteriorating.

Roll forward to fresh 18 to 24-month LEAPS at a similar delta. Yes, it costs a bit. But keeping your core position fresh means your income engine keeps humming.

The bottom line

Here's what it comes down to.

Traditional dividend investors wait for companies to decide when and how much to pay them. They tie up huge amounts of capital. They accept whatever yield the market offers.

You don't have to play that game.

With LEAPS as your capital-efficient core and a disciplined monthly process of selling short calls, you create your own dividend schedule. You control the timing. You adjust based on market conditions. You collect income on stocks that don't pay dividends.

The strategy isn't complicated: keep your LEAPS deep in-the-money for stability, keep your short calls mechanical and consistent, and let theta do the heavy lifting month after month.

The magic isn't in any single brilliant trade. It's in the compounding power of a boring, repeatable process executed consistently over time.

Most traders fail because they get clever. They overcomplicate. They try to predict.

The ones who succeed? They keep it simple, they follow the rules, and they show up every month to collect their synthetic dividend.

Probabilities over predictions,

Andy Crowder

📩 Join thousands of readers building a professional foundation.

Subscribe to The Option Premium and learn to trade with confidence and clarity.

📺 Want more education and community?

🎥 Subscribe on YouTube for in-depth tutorials and live trade breakdowns.

📘 Join the conversation on Facebook for exclusive insights, discussions, and real-time updates.

Disclaimer: This is educational content only. Not investment, tax, or legal advice. Options involve risk and aren't suitable for all investors. Examples are illustrative. Real results will vary. Talk to professionals before you risk real money.

Reply