- The Option Premium

- Posts

- Income Math with LEAPS - Basis Reduction, Yield on Capital, and Realistic Expectations

Income Math with LEAPS - Basis Reduction, Yield on Capital, and Realistic Expectations

Learn the real income math behind LEAPS (PMCC) strategies: basis reduction tracking, yield on capital calculations, and realistic expectations with practical examples and risk rules.

Income Math with LEAPS: Basis Reduction, Yield on Capital, and Realistic Expectations

Most people fall in love with LEAPS income strategies for one reason: they feel like discovered leverage.

Instead of tying up $18,000 to buy 100 shares outright, you spend perhaps $4,000 to $8,000 on a deep in-the-money LEAPS call, then sell short-term calls against it as if you owned the stock. That's the Poor Man's Covered Call in plain terms, a covered call structure built on options rather than actual shares.

The mechanics are straightforward enough. But the strategy doesn't become real until you can answer three questions with actual numbers: How much have you genuinely reduced your cost basis? What yield are you earning on the capital you've actually deployed? And what should you realistically expect without indulging in fantasy projections?

Let's build a framework you can apply consistently, month after month.

The Three Numbers That Matter

Every PMCC position should be tracked against these three metrics every single cycle. If you're only watching the premium line, you're missing the point.

Net Debit

Your net debit is the cost of the LEAPS minus any premium collected at entry. Most traders track what they paid for the LEAPS and stop there. That's insufficient. In a PMCC structure, your true cost basis evolves over time because you're continuously collecting, and sometimes returning, premium through the short call overlay.

Think of net debit as the outstanding balance on a loan. It's what you still have at risk after accounting for all premium activity.

Basis Reduction

Basis reduction is the cumulative net premium from your short calls after accounting for buybacks, rolls, and adjustments. If you sell a call for $1.20 and buy it back for $0.25, your net premium for that cycle is $0.95, or $95 per contract.

That $95 isn't merely income in the traditional sense. It's basis reduction. It lowers what you've effectively paid for the LEAPS position over time. If you execute ten similar cycles, you haven't simply "made $950." You've reduced your effective LEAPS cost by $950, which fundamentally alters your risk profile.

Yield on Capital

This is where most traders accidentally deceive themselves. Yield on capital measures net premium collected divided by the net debit you've actually deployed. If your LEAPS cost $5,000 and you collect $1,000 in net premium over a period, your yield on capital is 20%.

That's meaningful because it's measured against the capital you actually used, not some notional stock value. But the trap comes next: annualizing that return as if it's guaranteed, smooth, and infinitely repeatable. It isn't.

A Realistic Example With Clean Numbers

Consider a stock trading at $180. You structure a classic PMCC by purchasing a deep in-the-money LEAPS call with roughly 0.80 delta for $50.00, or $5,000 total. Each month you sell a short call around 0.25 to 0.35 delta. Over six months, you complete six call cycles.

Using conservative, realistic assumptions: you sell the call for $1.10 and later buy it back or roll it for $0.30, producing net premium of $0.80, or $80 per cycle. Over six months, that's $480 in net premium collected.

What have you accomplished? You've achieved $480 in basis reduction. Your six-month yield on capital is $480 divided by $5,000, or 9.6%. Annualized, that suggests roughly 19% to 20%.

But notice what we haven't assumed. Perfect fills at mid-price every time. Uninterrupted premium selling without defensive adjustments. Constant volatility. No early assignment complications. That restraint is what makes this projection realistic rather than promotional.

The Basis Reduction Ledger You Should Actually Track

Most traders track PMCC profit and loss the way they'd track a stock position. That's a category error.

A PMCC behaves more like a small business operation. Your LEAPS is the capital equipment. Your short calls generate monthly revenue. Your roll losses and adjustments are operating expenses. You wouldn't run a business without a P&L ledger. Don't run a PMCC without one either.

Start with your LEAPS cost. Update it every cycle with net premium, not gross premium. After six cycles, the $5,000 LEAPS carries $4,520 in effective basis. That's the core economic engine working as designed.

The tracking method is simple. Start with your initial LEAPS cost. Each month, add the short call credit received, subtract the cost to close or roll that short call, and record the net premium for that cycle. Then update your effective basis by subtracting cumulative net premium from the original cost.

After six cycles in our example, your LEAPS cost remains $5,000 on paper. But you've collected $480 in net premium. Your effective basis has dropped to $4,520. That's not just psychological comfort. It's the core economic engine of the strategy, systematically lowering your breakeven while maintaining long exposure.

The Uncomfortable Truth About Income

A PMCC can generate income, sometimes substantial income. But that income isn't free. It arrives with three built-in trade-offs.

Know these before the market teaches you the hard way. Each trade-off has a corresponding rule that keeps the math from working against you.

First, you're short convexity on the upside. The short call is your income engine. It is also a cap on your upside participation. When the stock rallies hard, you feel the constraint. The LEAPS provides some buffer through its higher delta, but the short call can still become a management problem quickly. Have explicit roll triggers before entry, not emotional reactions when it happens.

Second, the income isn't stable. Premium varies with implied volatility, realized volatility, trend strength, earnings cycles, and broader market conditions. Some months deliver excellent premium. Other months you barely collect anything worthwhile. Some months you're forced to roll for a debit just to maintain the structure. Plan around 0.5% to 3% monthly, net and not gross. Not every month will deliver.

Third, annualized yield figures are often marketing fiction. If you generate 3% on capital during a high-volatility month and annualize that to 36%, you've created a number, not a plan. A genuine plan survives the bad months without requiring you to abandon the strategy. Measure yield on net debit. Compare to real alternatives. Not to the theoretical maximum.

A Realistic Expectations Framework

If you want to set expectations professionally, stop asking "What percentage can I make per month?" Start asking better questions.

What market environment are you operating in? During low-volatility grinding bull markets, income will be smaller, rolls more frequent, and managing the upside more critical. During high-volatility choppy markets, income may be larger, but drawdowns and whipsaws become real concerns. In bear markets, call income helps cushion losses, but you're still carrying long exposure through the LEAPS itself.

What's your realistic sellable premium range? For many liquid underlyings, major ETFs and large-cap stocks, a reasonable expectation for monthly short calls might be 0.5% to 3% of LEAPS cost in net premium, depending on implied volatility and strike selection. Not every month. Not guaranteed. But a sane planning range that accounts for real market behavior.

0.5% to 3% of LEAPS cost per month is the honest planning range. The environment determines where you land within it. Neither the low end nor the high end is guaranteed.

What's your rule when things go wrong? Because they will. You need clearly defined protocols for when the stock rips through your short strike, when the stock drops and volatility spikes, for earnings week complications, for when bid-ask spreads widen uncomfortably, and for when you're forced to choose between rolling at a loss and resetting the entire position.

If you can't describe your defensive protocols in two sentences, your expectations are too optimistic.

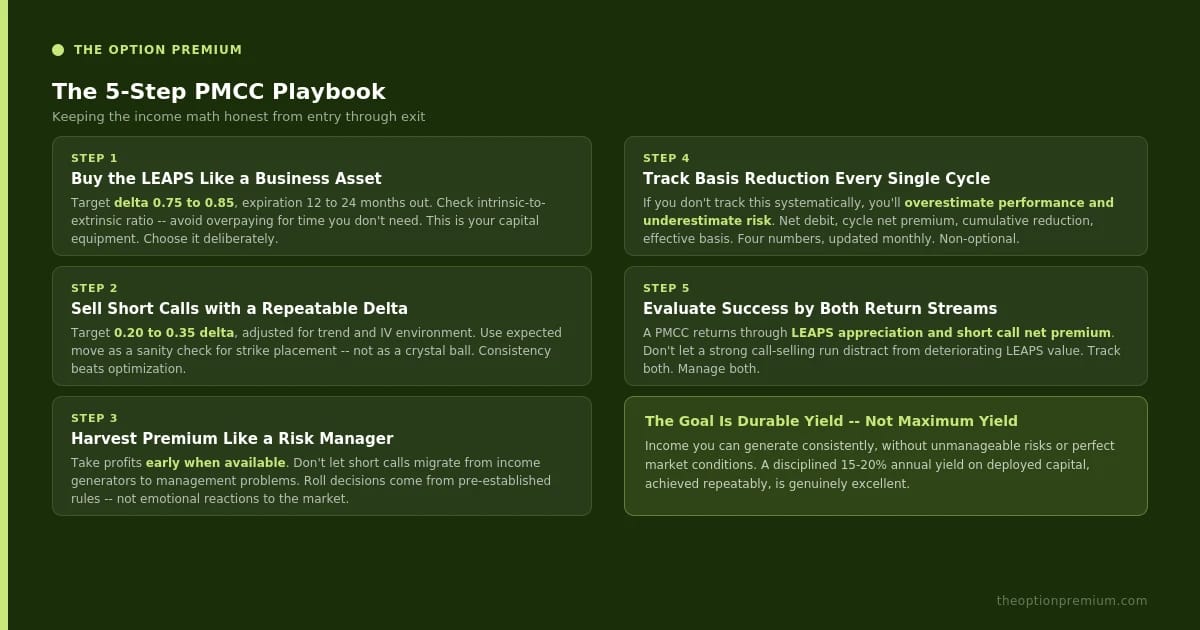

The Practical Playbook: Keeping the Math Honest

Five steps, executed consistently. Step 4, tracking basis reduction every cycle, is the one most traders skip. It's also the one that separates professional execution from wishful thinking.

Step 1: Buy the LEAPS like you're acquiring a business asset. Target delta around 0.75 to 0.85, expiration 12 to 24 months out, and modest extrinsic value. You want something that behaves like stock without overpaying for time decay you don't need.

Step 2: Sell short calls with a repeatable delta. A common range is 0.20 to 0.35 delta, adjusted for trend strength and volatility environment. Use expected move as a sanity check for strike placement, not as a crystal ball. Consistency beats optimization.

Step 3: Harvest premium like a risk manager. Take profits early when they're available rather than waiting for maximum decay. Avoid letting short calls migrate from income generators to management problems. Make roll decisions based on pre-established rules, not emotional reactions to market movement.

Step 4: Track basis reduction every cycle. If you don't track this systematically, you'll overestimate performance and underestimate risk exposure. This isn't optional record-keeping. It's core position management.

Step 5: Evaluate success correctly. A PMCC generates returns through two streams: LEAPS appreciation or depreciation, and short call net premium. Effective management means you're not blind to either component. Don't let a string of successful short calls distract you from deteriorating LEAPS value, and don't let LEAPS gains tempt you into sloppy short call selection.

A Quick Reality Check

Before labeling any PMCC position "excellent income," run through these five questions honestly.

Are you reducing basis net of all rolls and buybacks, or just collecting gross premium? Are you comparing income to net debit deployed, not to the notional stock price? Are you assuming you can sell calls every month without interruption or defensive adjustments? Do you have clearly defined rules for sharp rallies, and separately for earnings weeks? Is your position size small enough that one adverse move doesn't paralyze your decision-making?

If any answer is no, recalibrate your expectations accordingly.

The Goal Isn't Maximum Yield

The goal is durable yield, income you can generate consistently without taking unmanageable risks or requiring perfect market conditions.

The PMCC isn't magic. It's simply an intelligent trade-off: less capital than outright stock ownership, a disciplined income overlay through short calls, and a basis reduction mechanism that compounds quietly over time when managed properly.

If you maintain honest accounting, tracking net premium, basis reduction, and yield on deployed capital, you stop chasing the idealized version of the strategy and start executing the real one. And the real version, executed with discipline, is good enough.

That's not a compromise. It's the difference between sustainable income and eventual disappointment.

Trade Smart. Trade Thoughtfully.

Andy Crowder.

📩 Join thousands of readers building a professional foundation.

Subscribe to The Option Premium and learn to trade with confidence and clarity.

📺 Want more education and community?

🎥 Subscribe on YouTube for in-depth tutorials and live trade breakdowns.

📘 Join the conversation on Facebook for exclusive insights, discussions, and real-time updates.

Disclaimer: This is educational content only. Not investment, tax, or legal advice. Options involve risk and aren't suitable for all investors. Examples are illustrative. Real results will vary. Talk to professionals before you risk real money.

Reply