- The Option Premium

- Posts

- The Holy Grail of Trading: Low-Risk Ideas

The Holy Grail of Trading: Low-Risk Ideas

The real holy grail of trading isn't one perfect setup. It's a portfolio of small, defined-risk, positive-expectancy trades where no single outcome can damage your account. Here's the framework.

The Holy Grail of Trading: Low-Risk Ideas

Every trader starts the same way. They're looking for The Trade. The one setup that prints money consistently. The single strategy that unlocks the market and makes everything else irrelevant. They search for it in chart patterns, in indicators, in guru newsletters, in earnings whispers. And they never find it, because it doesn't exist.

The real holy grail of trading has nothing to do with finding one perfect trade. It has everything to do with finding a large number of low-risk ideas that, individually, don't matter much, but collectively produce consistent, compounding returns. This is the principle that separates traders who last from traders who blow up. And it runs directly through the core of premium selling.

The Myth of the Perfect Trade

The search for the perfect trade is the most expensive mistake in trading. Not because any single search costs you money, but because the mindset it creates leads to every other mistake.

Traders chasing the perfect trade concentrate their capital in a small number of high-conviction positions. They size too large because they "really believe in this one." They hold too long because they're waiting for the full move. They skip position sizing rules because this trade is "different." And when the trade goes against them, the loss is catastrophic, not because the market was unfair, but because they bet the account on a single idea.

The math is unforgiving. A 50% loss requires a 100% gain to recover. A 33% drawdown requires a 50% gain. The larger the loss, the more improbable the recovery. And concentrated positions create large losses. It's that simple.

The holy grail isn't a trade. It's a framework. And that framework is built on one principle: keep each individual risk small enough that no single outcome can meaningfully damage your account.

What "Low-Risk Idea" Actually Means

A low-risk idea is not a trade that can't lose money. Every trade can lose money. A low-risk idea is a trade where the maximum possible loss is a small, predefined percentage of your total capital, and where the probability of profit gives you a statistical edge over many occurrences.

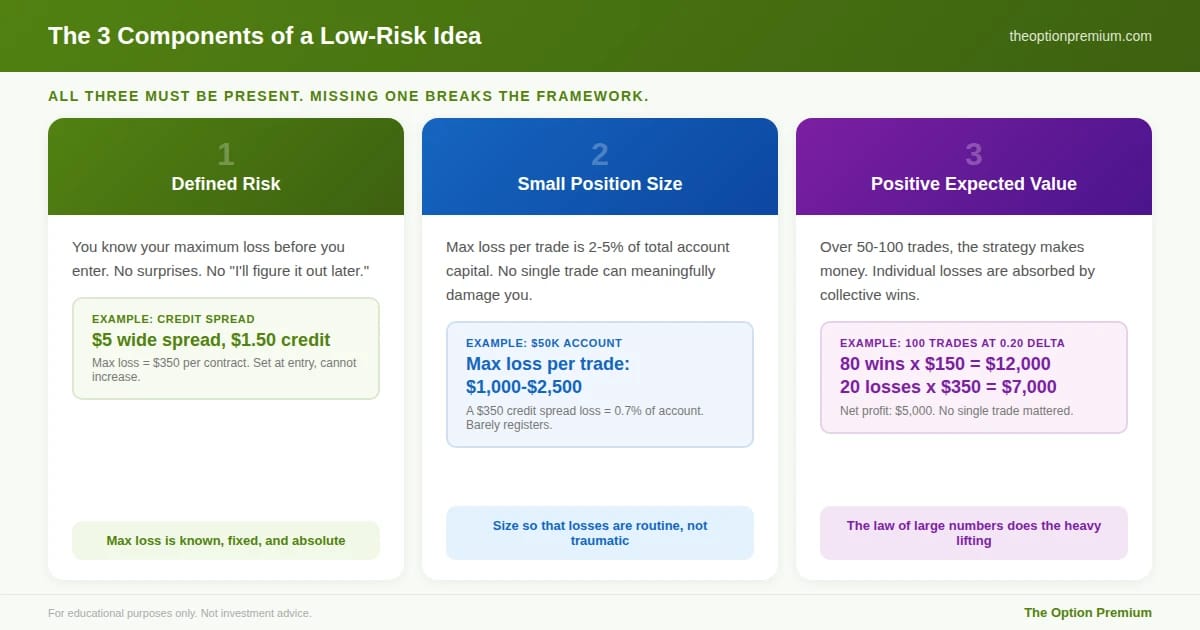

Three components define a low-risk idea.

Defined risk. You know your maximum loss before you enter. No surprises. No "I'll figure it out if it goes against me." Credit spreads are the clearest example: a $5 wide spread with a $1.50 credit has a maximum loss of $350 per contract. That number is set at entry and cannot increase.

Small position size relative to the account. Even a defined-risk trade becomes a high-risk idea if you put 30% of your account in it. A low-risk idea keeps max loss at 2-5% of total capital. On a $50,000 account, that's $1,000-$2,500 per position. The trade itself might have a 20% chance of losing, but if the max loss is 3% of your account, a loss barely registers in the long run.

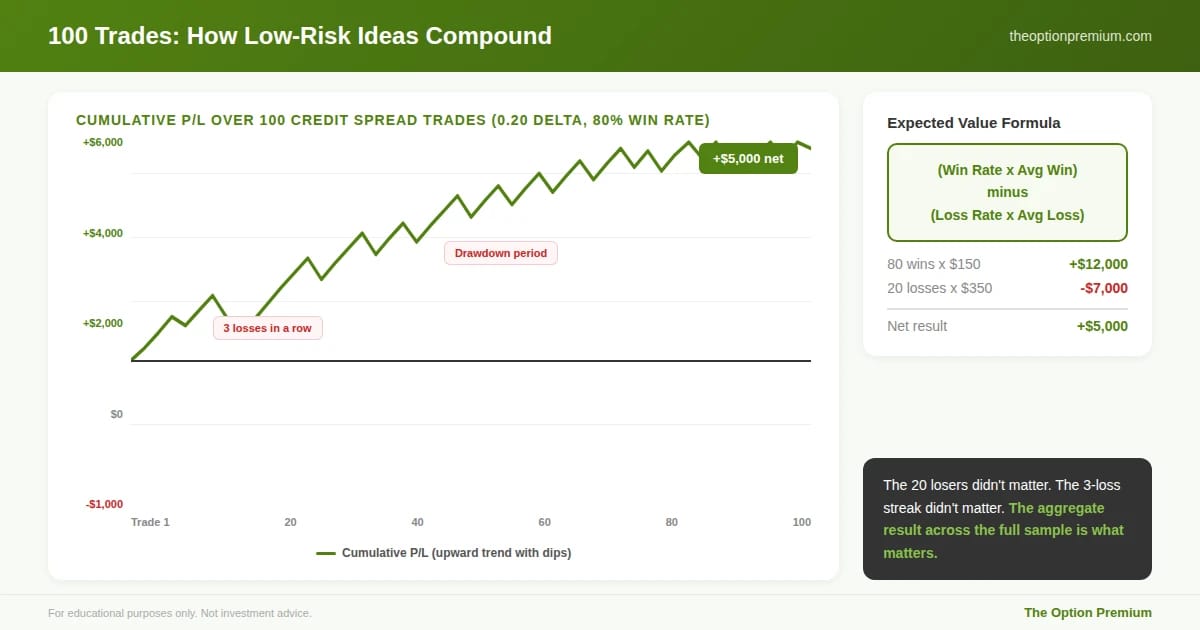

Positive expected value. Over a large sample, the trade makes money. This doesn't mean every trade wins. It means the average outcome across 50 or 100 repetitions is positive. A credit spread at 0.20 delta with a 30-40% return on capital has roughly an 80% win rate. Over 100 trades: 80 winners at $150 each ($12,000) minus 20 losers at $350 each ($7,000) = $5,000 net profit. That's positive expected value.

No single trade in that sample matters. The 20 losers don't matter. The occasional streak of 3-4 consecutive losses doesn't matter. What matters is the aggregate result across the full sample. This is the holy grail: a repeatable process that produces positive expected value through many small, low-risk bets.

All three components must be present. (1) Defined risk: max loss is known, fixed, and absolute before entry. (2) Small position size: 2-5% of total account, so losses barely register. (3) Positive expected value: 80 wins x $150 minus 20 losses x $350 = $5,000 net over 100 trades. No single trade matters.

The Math Behind the Holy Grail

Expected value is the formula that makes this framework work. It's not complicated, but it's the most important equation in trading.

Expected Value = (Win Rate x Average Win) minus (Loss Rate x Average Loss)

Let's apply it to three different approaches.

The concentrated trader. Makes 12 trades per year. Risks 15% of account per trade. Wins 60% of the time, averaging 20% gains and 15% losses. Expected value per trade: (0.60 x 20%) minus (0.40 x 15%) = 12% minus 6% = +6%. Sounds fine. But the risk of ruin is enormous. A streak of 3 consecutive losses (which will happen) creates a 45% drawdown. Most traders can't recover from that, financially or psychologically.

The premium seller with low-risk ideas. Makes 60 trades per year. Risks 3% of account per trade. Wins 78% of the time, averaging 35% ROC on winners and losing the full max loss on losers. Expected value per trade: (0.78 x 1.05%) minus (0.22 x 3%) = 0.82% minus 0.66% = +0.16% of account per trade. That's +9.6% on account annually from expected value alone, with no single trade risking more than 3%. A streak of 3 consecutive losses costs 9% of the account, uncomfortable but entirely recoverable.

The key difference isn't the expected value per trade. It's the risk of ruin. The concentrated trader has a meaningful probability of a catastrophic drawdown. The low-risk trader has essentially zero probability of ruin because no single trade, and no reasonable streak of losses, can destroy the account.

This is what Van Tharp, one of the most influential researchers on trading psychology, called the "holy grail" of trading systems. It's not about the win rate. It's not about the average win. It's about finding enough low-risk, positive-expectancy opportunities that the law of large numbers does the heavy lifting for you.

Two approaches, two completely different risk profiles. The concentrated trader makes 12 trades per year risking 15% each with a 45% potential drawdown from 3 consecutive losses. The premium seller makes 60 trades per year risking 3% each. Same streak of 3 losses costs only 9%. The difference isn't expected value per trade. It's risk of ruin.

Premium selling, by design, produces a high volume of low-risk, positive-expectancy trades. This isn't a coincidence. The mechanics of options pricing create a structural edge that aligns perfectly with the holy grail framework.

The volatility risk premium. Implied volatility overestimates actual realized moves approximately 80-85% of the time. This means options are systematically overpriced relative to the moves that actually occur. When you sell premium, you're selling overpriced insurance. Over time, the insurance pays out less than the premiums collected. That's a structural positive-expectancy edge.

Theta decay is relentless and predictable. Every day that passes with the stock inside your profit zone, your position gains value. You don't need the stock to move in your favor. You just need it to not move too far against you. Time is literally on your side, and it works every single day, including weekends and holidays.

Credit spreads are inherently defined-risk. The maximum loss is known before entry. No gap risk beyond the spread width. No margin call surprises. This makes position sizing precise, which makes the "small percentage of capital" rule easy to implement consistently.

The strategy generates high trade frequency. A premium seller running 5-8 positions at a time, turning them over every 20-30 days (closing at 50-75% of max profit), generates 50-80+ trades per year. That's enough sample size for the law of large numbers to smooth out the variance and deliver results close to the expected value.

100 trades at 0.20 delta, 80% win rate. The line trends upward but isn't smooth. Losing streaks create visible dips. A 3-loss streak appears early but the cumulative result recovers and compounds. Final result: +$5,000. The 20 losses didn't matter. The aggregate result across the full sample is what matters.

Building Your Portfolio of Low-Risk Ideas

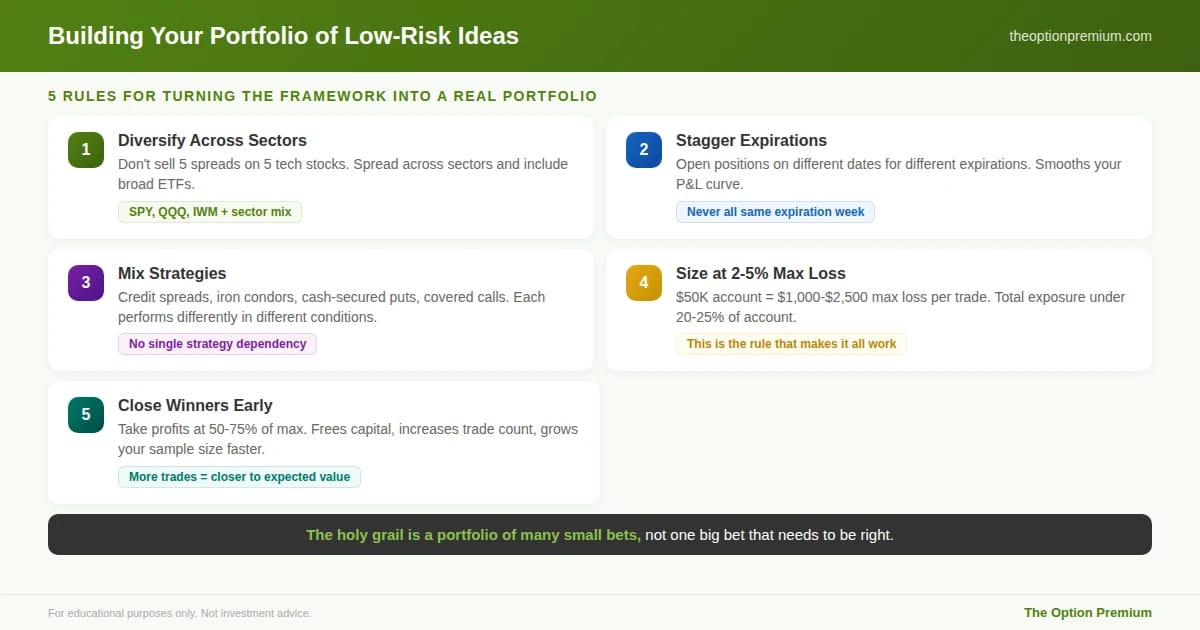

The holy grail isn't one trade. It's a portfolio. Here's how to construct it.

Diversify across underlyings. Don't sell 5 credit spreads on 5 tech stocks. A sector rotation hits all of them simultaneously. Spread across sectors: technology, healthcare, financials, consumer, industrials. Include broad ETFs like SPY, QQQ, and IWM as a core allocation.

Stagger expirations. Don't open all positions in the same week for the same expiration. Stagger entries so positions expire on different dates. This smooths your P&L curve and ensures you're not fully exposed to a single week's market action.

Mix strategies. Credit spreads, iron condors, cash-secured puts, covered calls. Each strategy has different risk characteristics and performs differently in different market conditions. A mix of strategies is more resilient than any single approach.

Size each position at 2-5% max loss. On a $50,000 account, that's $1,000-$2,500 maximum loss per trade. On a $100,000 account, $2,000-$5,000. Keep total portfolio exposure under 20-25% of account value. This is the rule that makes everything else work.

Close winners early. Taking profits at 50-75% of max profit frees capital faster, increases your annualized return on capital, and reduces the time your capital is exposed to risk. It also increases your trade count, which increases your sample size, which brings your actual results closer to your expected value.

Five rules for turning the framework into a real portfolio. (1) Diversify across sectors including broad ETFs. (2) Stagger expirations so you're never fully exposed to one week. (3) Mix strategies for resilience. (4) Size at 2-5% max loss per trade with total exposure under 20-25%. (5) Close winners early to free capital and grow sample size faster.

The Mental Capital Advantage

The holy grail framework doesn't just produce better financial outcomes. It produces better psychological outcomes. And in trading, psychology drives behavior, which drives results.

When no single trade represents more than 3-5% of your account, losing trades don't trigger emotional responses. You don't panic. You don't revenge trade. You don't abandon your system after a bad week. You process the loss as a normal, expected event (because it is), and you move on to the next setup.

Compare this to the concentrated trader who just lost 15% of their account on a single position. Their next decision will almost certainly be influenced by that loss, either through fear (missing the next good trade) or desperation (oversizing the next trade to recover). Both responses make things worse.

The holy grail framework removes the emotional component by making each individual outcome irrelevant. That's not a side benefit. It might be the most important benefit of all.

Risk Reality Check

The holy grail framework doesn't eliminate risk. It distributes it. You will still have losing months. A broad market selloff can test multiple positions simultaneously, which is why total portfolio exposure should stay under 20-25% per strategy approach. Correlation risk is real: "diversified" positions in similar sectors can move together during stress events.

The idea is to avoid concentrating too much risk in any one strategy at a given time. So if you’re running multiple approaches (for example, PMCCs, Wheel, spreads), in my opinion, each one should typically use no more than about 20 to 25% of total account value.

It’s a risk management guardrail. Markets don’t move in straight lines, and even high-probability strategies can go through rough stretches. By keeping exposure capped, you give yourself room to adjust, redeploy capital, and stay in the game without one segment of the portfolio doing outsized damage.

Think of it less as a hard rule and more as a discipline that helps smooth returns and control downside.

The framework also requires discipline that most traders underestimate. Selling a $150 credit spread feels small and boring, especially when you see others posting screenshots of massive gains. The compounding doesn't feel impressive in any single month. It feels impressive after 12-24 months when you look at the cumulative result and realize you achieved it without a single trade that threatened your account.

Key Takeaways

The holy grail of trading is not a single perfect trade or strategy. It's a framework built on many small, low-risk, positive-expectancy trades where no single outcome can meaningfully damage your account. The law of large numbers does the heavy lifting.

A low-risk idea has three components: defined maximum loss (known before entry), small position size relative to account (2-5% max loss per trade), and positive expected value over a large sample (win rate times average win exceeds loss rate times average loss).

Premium selling is structurally built for this framework. The volatility risk premium provides a systematic edge, theta decay works in your favor every day, credit spreads offer defined risk, and the strategy naturally generates the 50-80+ trades per year needed for the law of large numbers to work.

Build a portfolio of low-risk ideas by diversifying across sectors, staggering expirations, mixing strategies (credit spreads, iron condors, cash-secured puts, covered calls), sizing at 2-5% max loss per trade, and closing winners early to increase trade frequency.

The mental capital advantage may be the most important benefit. When no single trade matters, you trade without fear, without desperation, and without the emotional distortions that destroy most accounts. Boring compounding beats exciting destruction every time.

The holy grail isn't hidden. It isn't complicated. It's just not exciting enough for most traders to stick with. That's exactly why it works.

Andy Crowder

🎯 Ready to Elevate Your Options Trading?

Subscribe to The Option Premium, a free weekly newsletter delivering:

✅ Actionable strategies.

✅ Step-by-step trade breakdowns.

✅ Market insights for all conditions (bullish, bearish, or neutral).

📩 Get smarter, more confident trading insights delivered to your inbox every week.

📺 Follow Me on YouTube:

🎥 Explore in-depth tutorials, trade setups, and exclusive content to sharpen your skills.

📘 Join the conversation on Facebook.

Disclaimer: This is educational content only. Not investment, tax, or legal advice. Options involve risk and aren't suitable for all investors. Examples are illustrative. Real results will vary. Talk to professionals before you risk real money.

Reply