- The Option Premium

- Posts

- High-Probability Options Trading: Why Small Profits Win

High-Probability Options Trading: Why Small Profits Win

Learn why high-probability options trading with 78% win rates builds more wealth than chasing home runs. The math, psychology, and strategies that work.

Andrew Crowder

June 28, 2025

High-Probability Options Trading: Why Small, Consistent Profits Beat Home Runs Every Time

At 2:47 PM on a Tuesday in March, Jake hit his third consecutive 200%+ winner on NVDA calls. His $5,000 account had ballooned to $18,600 in six weeks.

"I've cracked the code," he texted me. "These small-time traders playing for 15% returns don't get it."

Three months later, Jake was broke.

His story illustrates the most dangerous misconception in options trading: that spectacular returns indicate superior skill. In reality, they usually indicate superior luck, and luck always runs out.

This is why understanding the Law of Large Numbers isn't just mathematical curiosity. It's the survival knowledge that separates traders who build lasting wealth from those who destroy their accounts chasing the next big win. High-probability options trading, the kind that targets 70-85% win rates with modest but consistent returns, is mathematically, psychologically, and practically superior to home-run speculation.

Let me show you exactly why, and how to implement it.

Why Your Brain Is Wired to Reject High-Probability Options Trading

Harvard neuroscientist Dr. Hans Breiter discovered that massive trading gains activate the same brain circuits as cocaine. This creates what behavioral psychologists call "intermittent reinforcement," the most addictive behavioral pattern known to psychology. It's the same mechanism that keeps people pulling slot machine levers.

Here's how the addiction cycle destroys options traders:

Big win → Dopamine flood → Confidence inflation → Larger positions → Inevitable loss → Account destruction

The math is unforgiving. If you're targeting 300% returns, you only need to be wrong once with an oversized position to lose everything. But our stone-age brains interpret big wins as proof of superior skill, not random luck.

Professional options traders understand this neurochemical trap. They've trained themselves to find satisfaction in statistical edges and consistent execution, not emotional highs.

Evolution wired us for environments where finding one massive food source was better than finding many small ones. This ancient programming creates three specific modern trading disasters:

Recency bias causes us to overweight recent results. Three 12% wins feel less significant than one 40% win, even when the cumulative profit is identical.

Social validation seeking distorts our benchmarks. Nobody posts screenshots of 1.8% monthly gains on social media. But those gains compound to 24% annually, better than nearly every hedge fund on the planet.

Loss aversion asymmetry makes us psychologically need wins twice as large as our losses to feel "worth it," even when the math says smaller, more frequent wins build far more wealth.

Academic research on investor psychology shows that professional investors who overcome these biases think in "batting averages," not "home run statistics." They measure success by consistency, not magnitude.

The Mathematics of Boring Success: Why Base Hits Beat Home Runs

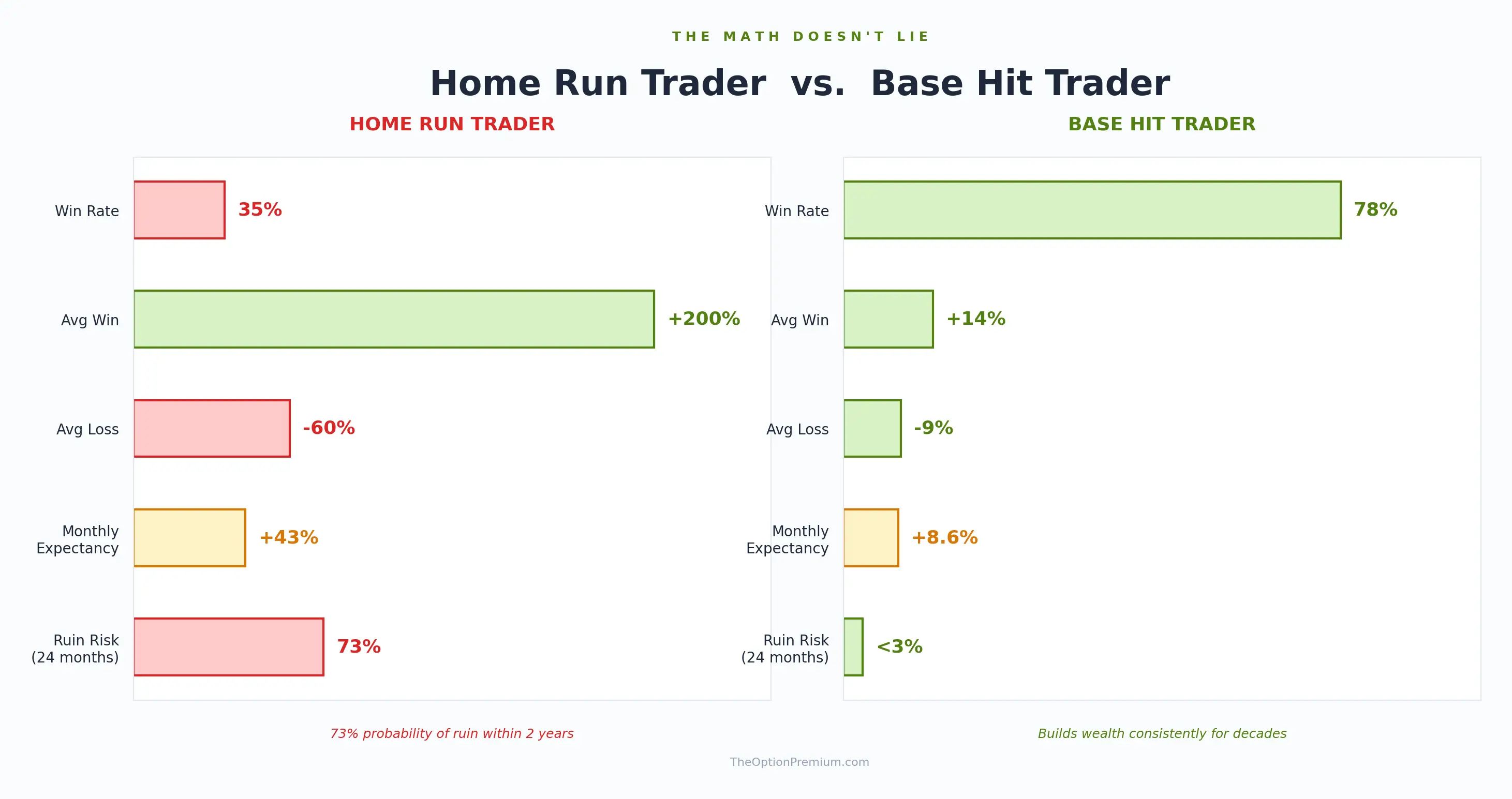

Let me show you exactly why high-probability options strategies outperform home-run approaches over time. The numbers aren't even close.

The Home Run Trader:

35% win rate

+200% average wins, -60% average losses

Monthly expectancy: +43%

Probability of ruin within 24 months: 73%

The High-Probability Base Hit Trader:

78% win rate

+14% average wins, -9% average losses

Monthly expectancy: +8.6%

Probability of ruin within 24 months: less than 3%

High-probability options trading comparison showing 78% win rate base hit trader versus 35% win rate home run trader

The home run trader looks brilliant in small samples. After 10 trades, they might be up 150%. After 100 trades? They're usually wiped out. The base hit trader looks boring in small samples, but they're still compounding wealth decades later.

Starting with $100,000 and compounding at just 18% annually, entirely achievable with a disciplined, high-probability options approach:

Year 5: $228,776

Year 10: $522,859

Year 15: $1,191,459

Year 20: $2,731,905

That's the power of boring consistency compounded over time. No lottery tickets. No 10-baggers. Just steady, methodical premium collection month after month.

Compound growth chart showing $100,000 growing to $2.73M over 20 years with consistent high-probability options trading

The High-Probability Options Trading Playbook

The most successful options traders I know have embraced what I call "statistical serenity": a deep, unshakeable confidence in mathematical processes rather than individual outcomes. Here's the framework they use.

High-Probability Strategy Selection

Not all options strategies offer favorable probabilities. The ones that consistently deliver 65-85% win rates share common characteristics: they sell premium, they benefit from time decay (theta), and they're positioned with a statistical edge using implied volatility and probability analysis.

The core high-probability options strategies include:

Iron condors on underlyings with IV rank above the 70th percentile. By selling both a put spread and a call spread outside the expected move, you create a wide profit zone that benefits from time decay and volatility contraction. Probability of profit on a well-constructed iron condor typically ranges from 70-85%.

Cash-secured puts at tested support levels on high-quality stocks. You collect premium while waiting to buy a stock you want at a lower price. Win rates of 75-85% are common when you sell puts at strikes below key support with 30-45 days to expiration.

Credit spreads positioned outside expected moves. Whether you use bull put spreads in bullish conditions or bear call spreads in bearish ones, defined-risk credit spreads let you choose your own probability of success before entering the trade.

Covered calls on range-bound, dividend-paying stocks. This is the most conservative high-probability approach. You own the stock and sell call premium against it every month.

Poor Man's Covered Calls for traders with smaller accounts who want the covered call experience with less capital. Using LEAPS as a stock replacement reduces capital requirements by 60-80%.

Target Metrics for Consistent Options Income

The numbers that matter aren't the ones most traders track. Forget about your biggest winner. Focus on these:

Win rate: 65-80% across all trades

Average return per trade: 10-20% on deployed capital

Reward-to-risk ratio: 2:1 minimum

Maximum risk per trade: 2% of total account value

Monthly portfolio return: 2-5% on total capital

Process-Focused Trading Questions

After every trade, regardless of outcome, ask yourself:

Did I follow my entry criteria exactly?

Was my position sizing mathematically appropriate?

Did I manage the trade according to my predetermined rules?

What can I learn from this trade, regardless of profit or loss?

When you judge yourself on process execution rather than dollar outcomes, you become immune to the emotional swings that destroy most traders.

Understanding Variance in High-Probability Options Trading

Even with perfect execution, statistical variance creates psychological challenges that trip up even experienced traders. You need to expect it, plan for it, and refuse to let it change your approach.

Good variance periods: You might see 25% annual returns for 2-3 consecutive years. This creates dangerous overconfidence. Traders start increasing position sizes, expanding into unfamiliar strategies, or abandoning risk management rules because they "know what they're doing."

Bad variance periods: You might see 8% annual returns for a year or two. This creates destructive self-doubt. Traders abandon proven strategies, start chasing higher-return approaches, or quit options trading entirely, right before the edge would have reasserted itself.

The Law of Large Numbers tells us both are temporary deviations from your true edge. Professionals trust their process while continuously gathering data about whether their fundamental assumptions remain valid.

Here are the warning signs that variance is affecting your judgment:

Taking larger positions after winning streaks

Abandoning proven strategies during underperformance periods

Adding unproven methods to "boost returns"

Making trade decisions based on recent results instead of your statistical criteria

Comparing your returns to social media traders who are showing you their highlight reel

The antidote to variance-driven emotion is sample size. The more trades you make using your proven approach, the more your actual results will converge with your expected results. This is the Law of Large Numbers in its purest form, and it's the bedrock of every statistically grounded options strategy.

Building an Anti-Fragile High-Probability Options Portfolio

Advanced traders don't just accept the Law of Large Numbers. They design portfolios specifically to benefit from it across multiple dimensions.

Strategy Diversification

Rather than concentrating all capital in a single strategy, blend approaches with different probability profiles:

60% of capital → High-probability, lower-return strategies (80% win rate, 10% average return per trade). This is your foundation. Iron condors on broad market ETFs, cash-secured puts on blue-chip stocks, and covered calls on range-bound dividend payers. This tier produces steady, reliable income.

30% of capital → Medium-probability, medium-return strategies (65% win rate, 18% average return). Credit spreads, jade lizards, and calendar spreads on individual stocks with elevated implied volatility rank. This tier adds growth without excessive risk.

10% of capital → Opportunistic, higher-return strategies (45% win rate, 35% average return). Earnings plays, breakout trades, and directional spreads when conditions are ideal. This tier provides upside potential without threatening your core capital.

Blended result: 72% overall win rate with 14% average return per trade.

Anti-fragile options portfolio allocation with 60% high-probability strategies, 30% credit spreads, 10% opportunistic

Volatility-Based Diversification

Different market environments favor different approaches. Adapt your allocation based on the VIX and implied volatility rank:

Low VIX environments (below 15): Shift toward debit strategies and reduce premium-selling positions. Premium is cheap, so selling it offers less reward relative to risk.

Medium VIX environments (15-25): Run your balanced approach. This is the sweet spot for high-probability premium selling.

High VIX environments (above 25): Lean aggressively into premium selling. Elevated volatility means richer premiums, wider expected moves, and better risk-reward on credit strategies. This is where patient premium sellers make their best returns.

Statistical Validation

Before deploying any strategy with real capital, test it across at least 200 historical scenarios to understand its true win rate, maximum drawdown, recovery period, and performance across different market conditions. This is how you build genuine confidence in your process, confidence that will sustain you through inevitable drawdown periods.

Case Study: From Home Run Chaser to High-Probability Trader

Sarah's trading evolution illustrates the transformation that happens when a trader embraces boring consistency over spectacular volatility.

Year 1: The Home Run Approach:

47 trades, 51% win rate

+47% average wins, -31% average losses

Net annual result: +3%

Emotional state: Constant anxiety, checking positions every 15 minutes, difficulty sleeping before expiration weeks

Year 2: The High-Probability Approach:

52 trades, 77% win rate

+11% average wins, -8% average losses

Net annual result: +19%

Emotional state: Calm confidence, reviewing positions once daily, sleeping soundly

Same trader. Same markets. Same account size. Completely different psychology, completely different results, and far less time spent staring at screens.

The key insight: Sarah didn't become a better market forecaster. She became a better probability manager. She stopped trying to predict where stocks would go and started positioning herself to profit from where they probably wouldn't go.

The Compound Psychology Effect

When you fully embrace high-probability options trading, you develop what I call "compound mental capital," psychological advantages that accumulate over time, just like compound interest on your account balance.

Reduced decision fatigue. When your criteria are clear and your rules are predetermined, you preserve mental energy for high-value analysis instead of spending it on constant stress management. You're not agonizing over every tick in your positions.

Enhanced pattern recognition. Trading the same strategies consistently across hundreds of iterations reveals subtle market inefficiencies that jump-from-strategy-to-strategy traders never discover. You start to see setups that others miss.

Calibrated risk awareness. Regular small losses prevent the overconfidence catastrophes that come from extended winning streaks. You develop a healthy, realistic relationship with risk instead of a fearful or reckless one.

Sustainable motivation. Process success is controllable. Outcome success isn't. When your sense of achievement comes from flawless execution rather than dollar amounts, motivation doesn't evaporate during drawdown periods.

Your High-Probability Implementation Plan

This week, commit to one high-probability options strategy for the next 30 consecutive trades. Not 5 trades. Not 10. Thirty trades, enough for the Law of Large Numbers to start demonstrating your edge.

Recommended Starting Strategies

If you're new to high-probability trading, start with one of these:

Cash-secured puts on oversold, high-quality stocks at 30-45 DTE, delta around 0.25-0.30

Iron condors on SPY or QQQ when IV rank is above the 50th percentile, positioned outside the expected move

Credit spreads outside 1-standard-deviation moves with 30-45 days to expiration

Covered calls on range-bound, dividend-paying stocks with 30-45 DTE

Success Metrics to Track

Measure yourself on these benchmarks after 30 trades:

Win rate above 70%

Average wins at least 1.5x larger than average losses

Maximum portfolio drawdown under 10%

Position sizing never exceeding 2% risk per trade

Your sleep quality unchanged by open positions (this one matters more than you think)

The Paradox of Boring Profits

Here's the beautiful irony of high-probability options trading: once you commit to boring profits, trading becomes genuinely exciting again, but for entirely different reasons.

You get excited about finding setups that perfectly match your criteria. About executing flawlessly regardless of outcome. About watching your account grow steadily month after month while traders around you ride emotional roller coasters.

The excitement comes from mastery, not chaos. From process, not results. From probability, not possibility.

The Law of Large Numbers isn't just a mathematical theorem. It's a philosophical framework that changes how you think about wealth building entirely:

From "How can I get rich quick?" to "How can I get rich consistently?"

From celebrating individual winners to celebrating systematic execution

From fearing small losses to embracing them as business costs

From chasing predictions to positioning for probabilities

This mindset shift separates gambling from investing, entertainment from wealth building, and temporary excitement from permanent security.

Your assignment: Choose boring consistency over spectacular volatility. The Law of Large Numbers will reward your patience with compound wealth that would make any home run hitter envious.

But you have to be willing to be bored long enough to find out.

Probabilities over predictions,

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply