- The Option Premium

- Posts

- How to Build a Dividend Aristocrats Portfolio with a Poor Man's Covered Call

How to Build a Dividend Aristocrats Portfolio with a Poor Man's Covered Call

Build an Aristocrat-style income portfolio using deep ITM LEAPS instead of stock. Same exposure, ~70% less capital, monthly premium income.

Andrew Crowder

May 09, 2026

How to Build a Dividend Aristocrats Portfolio with a Poor Man's Covered Call

Maximizing income with a fraction of the capital, a smarter way to own the most reliable dividend payers in the S&P 500.

In a market where investors are again hunting for steady cash flow, dividend stocks remain the default answer. And among dividend stocks, the Dividend Aristocrats sit at the top of the food chain. These are S&P 500 companies that have raised their dividend for at least 25 consecutive years. Boring? Sometimes. Reliable? Almost always. Capital efficient? Not even close.

That last part is the problem. Buying 100 shares of every Aristocrat you'd actually want to own is a six-figure exercise. And once your money is parked in those shares, it's not doing anything else.

The Poor Man’s Covered Call (PMCC) fixes that problem. Same income engine, fraction of the capital, and a structure that lets you build a diversified Aristocrat-style portfolio without writing a giant check. I’ve covered the mechanics in detail across the LEAPS Series, but this piece walks through how to apply that framework to the Aristocrats specifically, with real numbers from a position I’d actually take today.

Why the Aristocrats Are Worth the Effort

Dividend Aristocrats are a rare breed. To make the list, a company has to keep raising its payout through every recession, every credit crunch, every messy political cycle of the last quarter century. That's not luck. That's a balance sheet built to take punches.

As of 2026, there are roughly 70 names on the list. The S&P Dow Jones Indices methodology document lays out the exact criteria if you want to read the rules yourself. For income-focused investors, this universe offers a rare combination of reliability and long-term performance.

But here's the catch most articles skip: liquidity is everything in options trading.

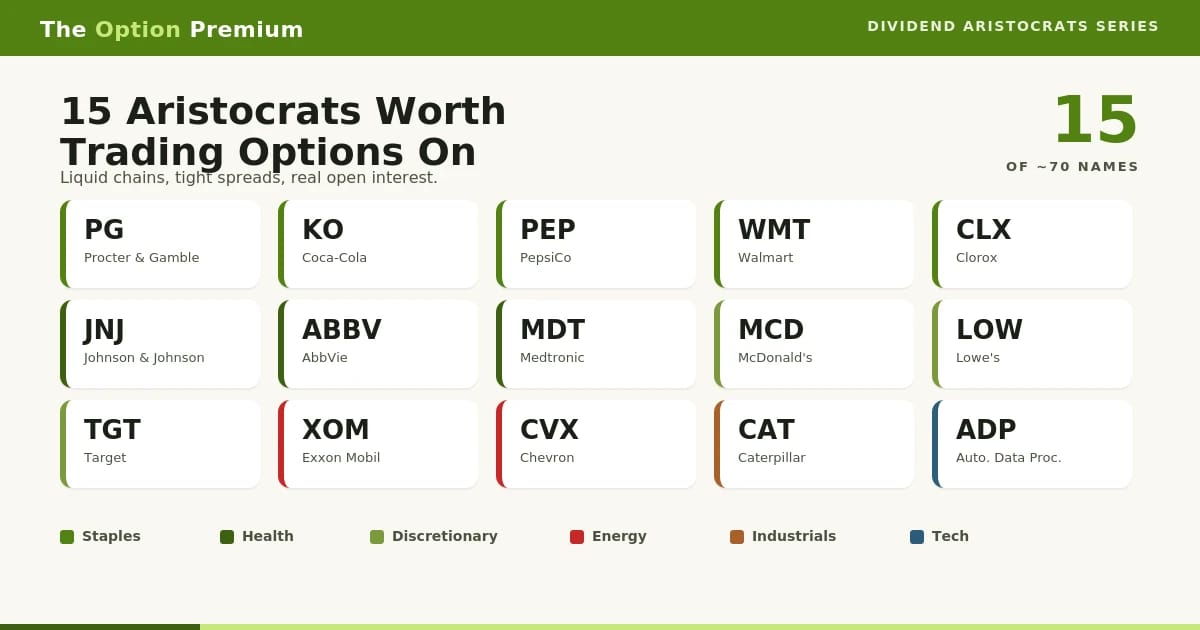

Of those 70 or so Aristocrats, only about 15 have options markets liquid enough to trade without bleeding capital to the bid-ask spread. The rest carry wide spreads, thin open interest, and daily option volume measured in dozens of contracts. Beautiful businesses, awful options chains.

Here's the working list of Aristocrats with the kind of options liquidity that makes a PMCC actually viable, grouped by sector.

Consumer Staples: Procter & Gamble (PG), Coca-Cola (KO), PepsiCo (PEP), Walmart (WMT), Clorox (CLX).

Health Care: Johnson & Johnson (JNJ), AbbVie (ABBV), Medtronic (MDT).

Consumer Discretionary: McDonald's (MCD), Lowe's (LOW), Target (TGT).

Energy: Exxon Mobil (XOM), Chevron (CVX).

Industrials: Caterpillar (CAT).

Information Technology: Automatic Data Processing (ADP).

If you want a refresher on what makes an options chain tradable, I went deep on bid-ask spreads, open interest, and volume in this primer on options liquidity. It's the single most important filter I run before I touch any new ticker.

Consumer Staples and Health Care anchor the list because that's where the dividend growth has been steadiest.

Why Aristocrats Trade Like Aristocrats

Before we get to the mechanics, it's worth pausing on why these names behave differently from the broader market.

Most Aristocrats run with a beta below 1.0, meaning they tend to move less than the S&P 500 in both directions. Many sit well below 0.5. That's not a marketing slogan. It's a function of who owns these stocks (pension funds, ETFs, long-horizon holders), what sectors they live in (Staples, Healthcare, parts of Industrials), and how their cash flows behave through a cycle.

Lower volatility shows up in three places that matter for an options seller. Drawdowns are usually shallower. Earnings shocks tend to be smaller in magnitude. And the implied volatility on their options chains is steadier, which means the premium you sell month after month doesn't whipsaw the way it does on a high-flying tech name.

That said, Aristocrats are not bulletproof. Rising rates can pressure dividend stocks broadly. Energy Aristocrats still ride the oil curve. Even the most reliable name can post a bad earnings report. The strategy isn't "you can't lose." It's "you can structure your exposure with less capital and more flexibility than buy-and-hold gives you."

The PMCC, Briefly

A traditional covered call requires you to own 100 shares before you can sell a call against them. That's the capital problem. The Poor Man's Covered Call keeps the same income mechanic but swaps the 100 shares for a single deep in-the-money LEAPS call option. The LEAPS acts as a stock substitute. You then sell shorter-dated calls against it for income, just like you would with the underlying.

Two parts. The long LEAPS gives you the directional exposure. The short call generates the cash flow.

For a much deeper walk through the mechanics, my PMCC primer is the right starting point. What follows assumes you already know roughly how the structure works.

Picking the LEAPS

Three rules I follow on the long side.

First, target an expiration around two years out. Some traders go shorter, twelve to sixteen months. I've found the extra runway is worth a small premium because it slows time decay and gives the position room to breathe through whatever the market hands you.

Second, pick a strike with a delta of roughly 0.80. That keeps the option moving close to dollar for dollar with the stock and minimizes the percentage of your premium that's pure time value.

Third, demand liquidity. Tight bid-ask spreads, real open interest, and a willing market maker on the other side. If you have to chase the ask price, the position is already costing you money before it's even open.

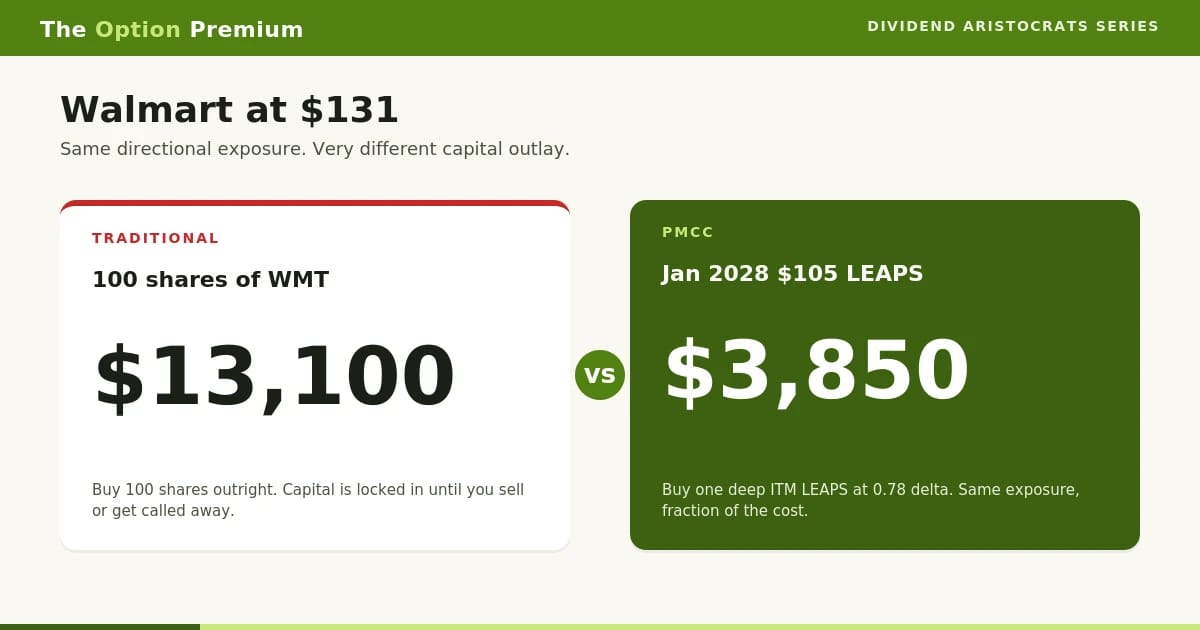

The Walmart Setup, in Real Numbers

Let's anchor this with a position you could actually structure today. Walmart is trading near $131 as I write this. A traditional covered call would mean buying 100 shares for roughly $13,100. That's a lot of capital for a single Aristocrat exposure.

Now look at the same trade through the PMCC lens.

The longest-dated standard LEAPS available on WMT is the January 21, 2028 expiration, roughly 626 days out. Walking the chain, the $105 call carries a delta of 0.78 and shows a bid of $36.45 against an ask of $41.00. That's a wide quote, which is normal on a deep ITM LEAPS. Always with a limit order, never the ask. A patient mid-price working order around $38.50 typically fills inside the spread on a name with this much underlying liquidity.

Capital comparison is straightforward.

Buying 100 shares of WMT: $13,100 of capital deployed.

Buying the January 2028 $105 LEAPS at $38.50: $3,850 of capital deployed.

That's roughly $9,250 of capital saved, or about 71% less capital tied up for essentially the same directional exposure. That freed-up capital is now available for diversification, additional PMCC positions across other Aristocrats, or simply staying in cash earning yield.

Same directional exposure, less than a third of the capital outlay. That capital efficiency is the entire point of the structure.

Selling Calls Against the LEAPS

With the LEAPS open, the income engine starts.

I sell short-dated calls against the LEAPS at 30 to 45 days to expiration, targeting a delta between 0.20 and 0.30. That delta range corresponds to roughly a 70% to 80% probability of expiring worthless, which is the math I want on a recurring income trade.

For Walmart at $131, a $140 call expiring in 44 days carries a 0.28 delta and trades $2.16 bid against $2.26 ask. Call it $2.20 of premium on a mid-price fill. On the $3,850 LEAPS, that's a 5.7% return collected in 44 days. Annualize that and you're north of 45% on capital. Will every cycle land that cleanly? No. Some months you collect less, some months you have to roll the short call up and out to dodge assignment. But over a full year of disciplined call selling, premium yields in the 25% to 45% range on the LEAPS cost basis are a realistic target.

Compare that to the same Walmart position structured as a traditional covered call. The same $140 short call against 100 shares generates the same $220 of premium, but on $13,100 of deployed capital. That's roughly 1.7% per cycle, or about 14% annualized.

The PMCC produces more than three times the yield on capital. Same short call. Same underlying. Different denominator.

The short call premium is identical. The capital base is what changes the equation.

Managing the Position

Two adjustments matter.

When the LEAPS gets inside 8 to 12 months from expiration, I roll it. Closing the existing LEAPS and opening a new two-year contract resets the time value runway and keeps the position from getting clipped by the steeper part of the decay curve. I cover the mechanics of that roll in this guide on rolling LEAPS.

If the underlying rallies hard and your short call goes deep in the money, you have a choice. You can roll the short call up and out for a credit, or you can let it get assigned and the LEAPS will cover delivery. Either way, the position has a defined ceiling, just like any covered call.

What About the Dividend?

Here's the honest trade-off with PMCCs on Aristocrats. LEAPS holders don't receive dividend payments. So if the entire reason you owned PG, KO, or JNJ was that quarterly check, you're giving something up.

But look at what you're getting in exchange. A typical Aristocrat yields 2% to 3% annually in dividends. The premium income from selling monthly calls against a properly chosen LEAPS routinely runs 2% to 4% per cycle on capital. Compounded across twelve cycles in a year, you're looking at premium income that comfortably exceeds the dividend yield, often by a factor of ten or more.

You're not collecting dividends. You're manufacturing your own income stream from the option premium, and you're doing it on less than a third of the capital. That's the trade.

Beyond the Aristocrats: Portfolio Templates

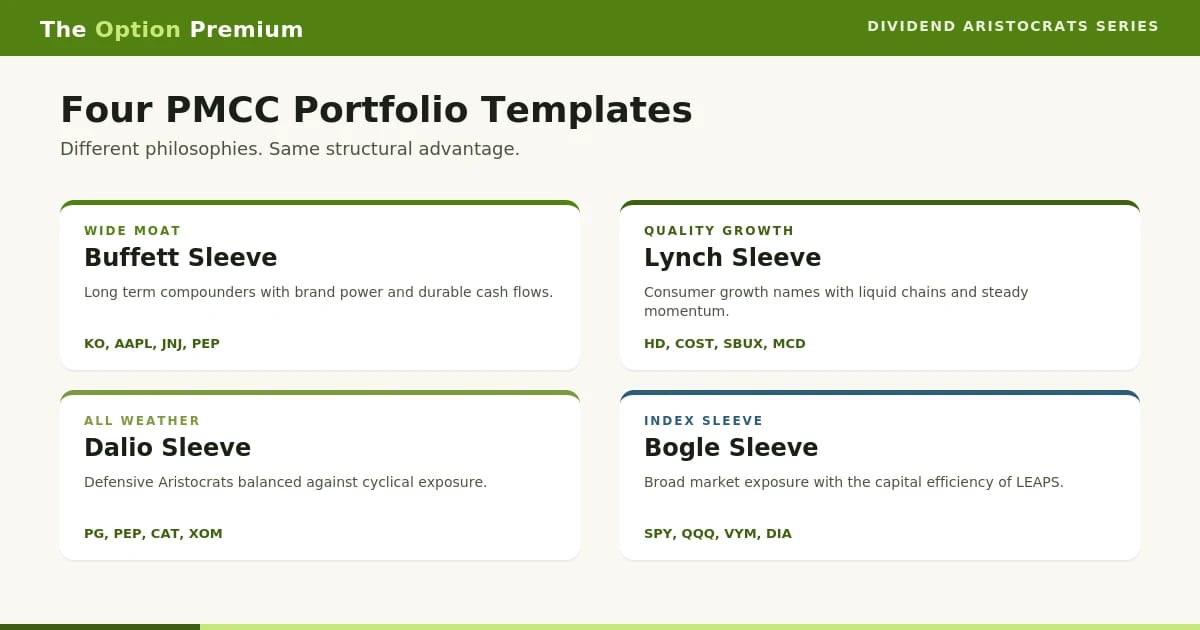

The PMCC framework isn't limited to Aristocrats. Once you're comfortable with the structure, you can build entire portfolios around different investing philosophies, all on a fraction of the buy-and-hold capital. A few starting points.

A Buffett-inspired sleeve focuses on wide-moat compounders like Coca-Cola, Apple, and Johnson & Johnson. Long LEAPS on each, monthly call sales for income.

A Lynch-inspired sleeve targets high-quality consumer growth names with liquid options chains. Home Depot, Costco, Starbucks. Same structure, different beta profile.

A Dalio-inspired all-weather sleeve mixes defensive Aristocrats (PG, PEP) with cyclical exposure (CAT, energy names) to balance the cash flow stream across regimes.

A Bogle-inspired index sleeve uses the same PMCC structure on liquid ETFs like SPY, QQQ, or VYM. You get index-level diversification with the capital efficiency of the LEAPS substitute.

The point isn't that any one of these is "right." The point is that the PMCC is a structural tool, and once you know how to use it, you can apply it across whatever investing framework actually fits your goals.

Different inputs, same structural advantage. Capital efficiency stacks regardless of which philosophy you're running.

The Bottom Line

Building a dividend-style income portfolio using PMCCs gives you four things buy-and-hold doesn't.

You drastically reduce the capital required to maintain exposure to blue-chip names. You generate a self-made income stream that, in most cycles, exceeds the dividend yield by a wide margin. You get true diversification across multiple stocks and sectors instead of concentration in a handful of high-yielders. And you keep flexibility, the position can be adjusted, rolled, or closed at any time without breaking the income engine.

Execution is the whole game. Choose the right LEAPS. Sell calls systematically. Roll on schedule. Skip the names with bad liquidity, no matter how much you love the underlying business.

Done with discipline, the PMCC turns the Aristocrats from a capital-heavy income strategy into something far more efficient, and far more scalable, than the buy-and-hold version most investors default to.

Continue the Poor Man’s Covered Call series

The Aristocrats are one application. Here are other portfolios built on the same structure:

A PMCC on SPY: the same approach on the most liquid equity ETF.

A PMCC on Gold: applying it to a non-equity, inflation-sensitive underlying.

The Dividend Kings approach: the same income structure on an even longer dividend-growth track record.

Trade Smart. Trade Thoughtfully.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply