- The Option Premium

- Posts

- Credit Spreads in Heightened Volatility: Why This Is the Seller's Market We've Been Waiting For

Credit Spreads in Heightened Volatility: Why This Is the Seller's Market We've Been Waiting For

VIX above 30 means the same 0.16 delta credit spread collects 50-100% more premium with 2x the buffer. Same probability. 64% more expected income per trade cycle. Here's the playbook.

Andrew Crowder

March 31, 2026

Credit Spreads in Heightened Volatility: Why This Is the Seller's Market We've Been Waiting For

With the VIX sitting above 30, geopolitical tensions reshaping market sentiment weekly, and the S&P 500 roughly 6% off its January highs, the options market is telling us something important: uncertainty is elevated, premiums are rich, and the statistical edge for premium sellers just got wider.

This is what we've been preparing for. Not a crisis to fear, but an environment to exploit.

I've been saying it for 24 years: selling options works because of probabilities. Because implied volatility consistently overestimates realized volatility. Because the market prices in more fear than what actually materializes. And that gap between what the market expects and what actually happens is never wider than in environments like this one.

If you've been building your skills during calm markets, sharpening your position sizing, learning to read IV Percentile, and understanding delta and probability, this is where all of that work pays a dividend. Let me show you exactly how.

The Current Landscape: What Elevated Volatility Means for Premium Sellers

The VIX above 30 means the market is pricing in annualized expected moves of roughly 30% on the S&P 500. To put that in perspective, the S&P 500's average annual return since 1926 is approximately 10%. The market is pricing in three times the average annual move in both directions. That's fear, not fundamentals.

And fear is overpriced. Research confirms that implied volatility exceeds realized volatility roughly 80-85% of the time on SPY. When VIX is elevated, that gap widens because the market overshoots on the fear side. The panic premium that traders pay for protection inflates the very options that we sell.

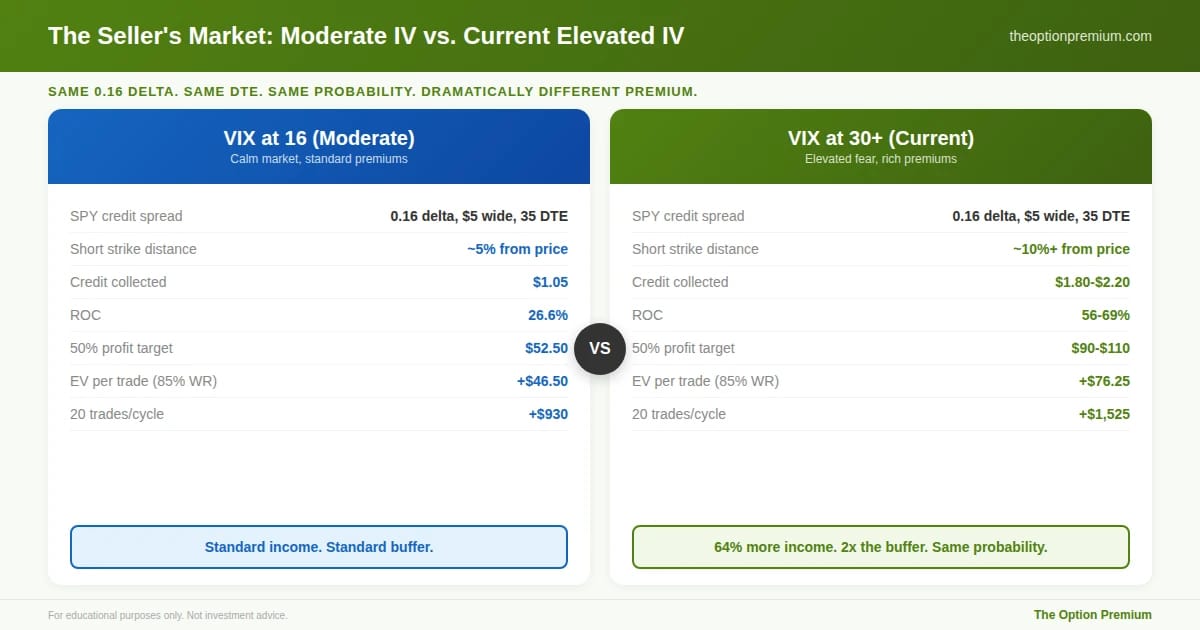

What this means practically. A credit spread that collects $1.05 in a moderate-IV environment (VIX at 16-18) might collect $1.80-$2.20 in the current environment with the exact same delta and DTE. Same probability of success. Same strike distance relative to the expected move. Dramatically richer premium. That's the mathematical definition of a seller's market.

The wider expected move works in your favor. When VIX is at 30, the one-standard-deviation expected move on SPY over 35 days is roughly $60-$65. Your 0.16 delta short strike is $60+ away from the current price. That's a 10%+ buffer. Compare that to VIX at 15, where your same 0.16 delta short strike is only $30 away (5% buffer). Elevated volatility doesn't just pay you more. It gives you more room to be wrong.

Same 0.16 delta. Same DTE. Same probability of success. Dramatically different payoff. At VIX 16, the credit spread collects $1.05 with a 5% buffer from the stock price, producing $46.50 expected value per trade. At VIX 30+, the same trade collects $1.80-$2.20 with a 10%+ buffer, producing $76.25 EV. Over 20 trades, that's $1,525 versus $930: a 64% increase in income with no change in probability or risk profile. This is the mathematical definition of a seller's market.

Why Most Traders Get This Exactly Backwards

Here's what frustrates me most about our industry, and I wrote about this years ago: the traders who should be deploying capital in this environment are sitting on the sidelines, paralyzed by fear. And the traders who should be cautious (the ones buying out-of-the-money options hoping for a lottery ticket) are more active than ever.

The financial media shows you the VIX at 30 and tells you to be scared. Social media is filled with accounts posting 300%, 400%, 1,200% returns on speculative put purchases, acting as if that's a sustainable strategy. It isn't. Those are lottery tickets. They hit occasionally, and when they do, the screenshots go viral. The hundreds of trades that expired worthless? Those never get posted.

I've been in this business for over two decades, and I can tell you: the traders who build wealth over time are not the ones chasing explosive gains on low-probability directional bets. They're the ones who sell premium into elevated IV, collect outsized credits, manage their risk, and compound the proceeds over years and decades.

Statistics don't lie. A stock or ETF only has a 50/50 chance of moving in either direction. That's no better than a coin flip. But when you sell a credit spread with an 80-85% probability of expiring out-of-the-money, you've fundamentally changed the math. You're not flipping coins anymore. You're being the casino, collecting a premium from every player at the table, and the house edge just got wider because fear inflated the premiums.

How to Deploy Credit Spreads in This Environment

The principles don't change in elevated volatility. The execution parameters adjust. Here's the framework.

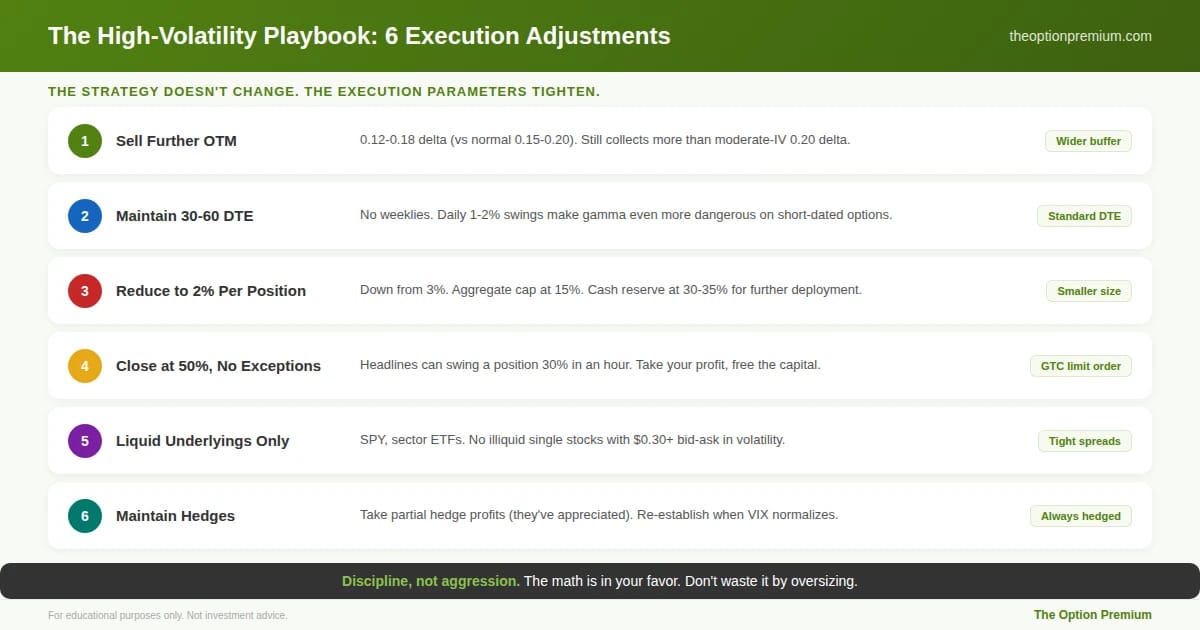

Sell further from the money than usual. In a VIX 16 environment, your 0.16 delta short strike is 5% from the current price. In a VIX 30+ environment, that same 0.16 delta is 10%+ from the current price. You're collecting richer premium at a greater distance. This is the structural advantage of selling in high IV: the expected move does the work for you.

On SPY currently near $560, a 0.16 delta put spread with 35 DTE might have its short strike near $500-$510. That's 9-10% below the current price. A $5 wide spread at this level could collect $1.50-$1.80. That's a 30-56% ROC on a trade with an 84% probability of success. In a moderate-IV environment, the same probability trade collects $0.70-$0.90. The math is dramatically better right now.

Maintain your standard DTE: 30-60 days. Don't shorten your timeframe just because volatility is elevated. The 30-60 DTE window gives you the optimal theta decay per day of risk and keeps you out of the gamma danger zone. In fact, the argument for staying in the 35-45 DTE range is stronger in high volatility because gamma accelerates faster on shorter-dated options when the underlying is swinging 1-2% daily.

Reduce position size, not position count. This is where discipline separates professionals from amateurs. High volatility means larger daily swings, wider bid-ask spreads on some underlyings, and a higher probability of multiple positions being tested simultaneously.

Drop from 3% per position to 2%. Keep your aggregate portfolio exposure at 15-20% instead of the normal 20-25% cap. This gives you room to adjust if needed and cash to deploy additional positions if the market drops further and premiums get even richer.

Close at 50% of max profit, same as always. The 50% profit target is even more important in high volatility. The market can swing 2% in either direction on a single headline. A position that's at 60% profit at 2:00 PM can be at 30% by the close. Take your 50%, free the capital, and redeploy. Don't get greedy when the market is moving this much.

The strategy doesn't change in heightened volatility. The execution parameters tighten. Sell further OTM (0.12-0.18 delta versus the normal 0.15-0.20) because the wider expected move means these strikes still collect more premium than a moderate-IV 0.20 delta trade. Maintain standard 30-60 DTE (no weeklies, daily 1-2% swings make gamma even more dangerous). Reduce position size to 2% with a 15% aggregate cap and 30-35% cash reserves. Close at 50% without exception because a single headline can swing a position 30% in an hour. Liquid underlyings only. Hedges always in place.

The Power of Probabilities: Why the Odds Favor Sellers Right Now

Let me bring this back to what matters: the statistical foundation.

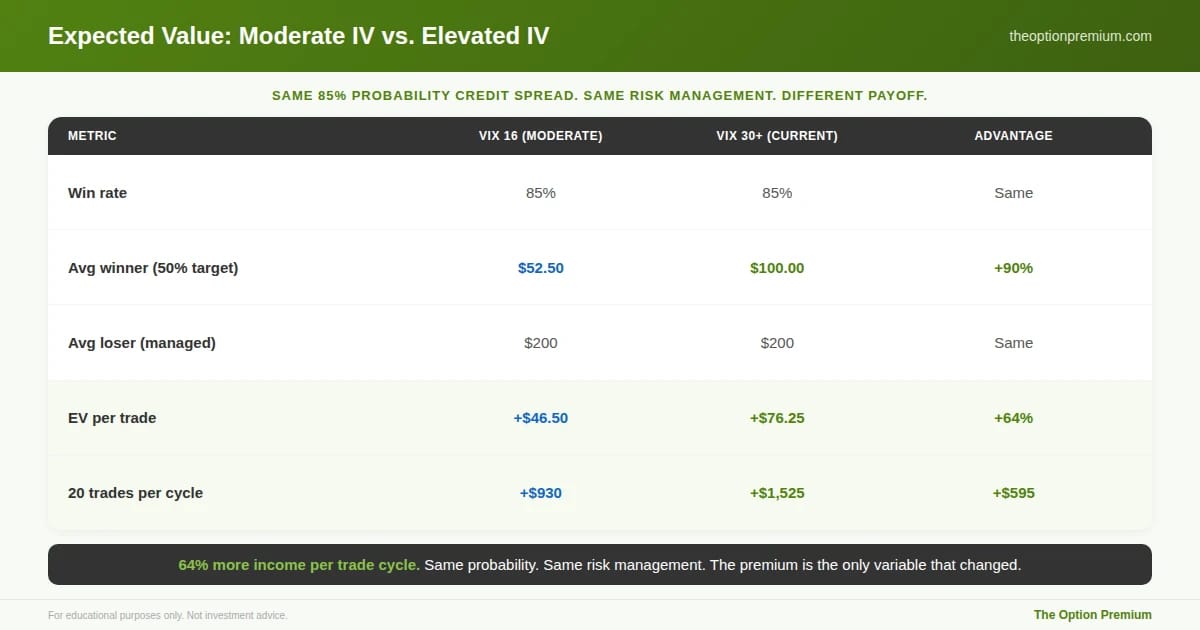

When you sell a credit spread with a 0.15 delta short strike, you have roughly an 85% probability of that option expiring out of the money. That's not a guess. It's derived from the options pricing model, built on decades of statistical analysis.

An 85% probability of success means that out of every 20 trades, you can expect approximately 17 winners and 3 losers. If your average winner (closed at 50% of max profit) is $90 and your average loser (managed at 2x credit evaluation) is $200, your expected value per trade is:

(0.85 x $90) - (0.15 x $200) = $76.50 - $30.00 = +$46.50 per trade.

Over 20 trades: +$930. That's per trade cycle, repeatable quarter after quarter.

Now here's what changes in elevated IV: the average winner increases because you're collecting more premium. That $90 winner becomes $125. The probability stays the same (you're selling the same delta). The expected value per trade jumps:

(0.85 x $125) - (0.15 x $200) = $106.25 - $30.00 = +$76.25 per trade.

Over 20 trades: +$1,525. A 64% increase in expected income, with no change in probability or risk profile. This is why elevated volatility is a seller's market. The math doesn't lie.

The expected value math in black and white. Same 85% probability of success. Same managed average loss of $200. The only variable that changed is the premium collected. At moderate IV, the average winner (closed at 50%) is $52.50, producing $46.50 EV per trade. At elevated IV, the average winner is $100, producing $76.25 EV. Over 20 trades: $1,525 versus $930. The probabilities haven't changed. The payoff per probability point has. That's the seller's edge in heightened volatility.

Is This the Beginning of a Sustained High-Volatility Regime?

It's a fair question. Geopolitical tensions, tariff uncertainty, an evolving interest rate environment, and election-year dynamics suggest that elevated volatility could persist for months, not weeks.

Looking at the broader picture: the VIX spiked above 60 last April during the tariff shock. It settled into a 16-22 range through the summer and fall of 2025. Now, with the Iran conflict and renewed trade tensions, it's back above 30. The market is cycling through volatility regimes faster than it has in years.

For premium sellers, a sustained elevated-volatility environment is the most favorable backdrop possible. Not because it's easy (the daily swings test your emotions and your risk management), but because the premium you collect per trade is 50-100% richer than in calm markets, your short strikes are further from the money in absolute terms, and the volatility risk premium (the gap between implied and realized) tends to widen during periods of sustained fear.

Will this last? Nobody knows. Volatility is mean-reverting, which means VIX at 30 will eventually return toward its long-term average near 19-20. But "eventually" could be next week or next quarter. What I do know is that every day the VIX stays elevated is a day where premium sellers have a structural advantage that doesn't exist in calm markets.

Should you be aggressive? No. You should be disciplined. Smaller position sizes. Wider strikes. Consistent profit targets. Cash reserves. Portfolio hedges in place. The premium sellers who survive decades don't blow out during high-volatility environments because they got greedy. They compound through them because they stayed disciplined.

The Playbook: Exactly What I'm Doing Right Now

Here's the practical framework I'm running in this environment.

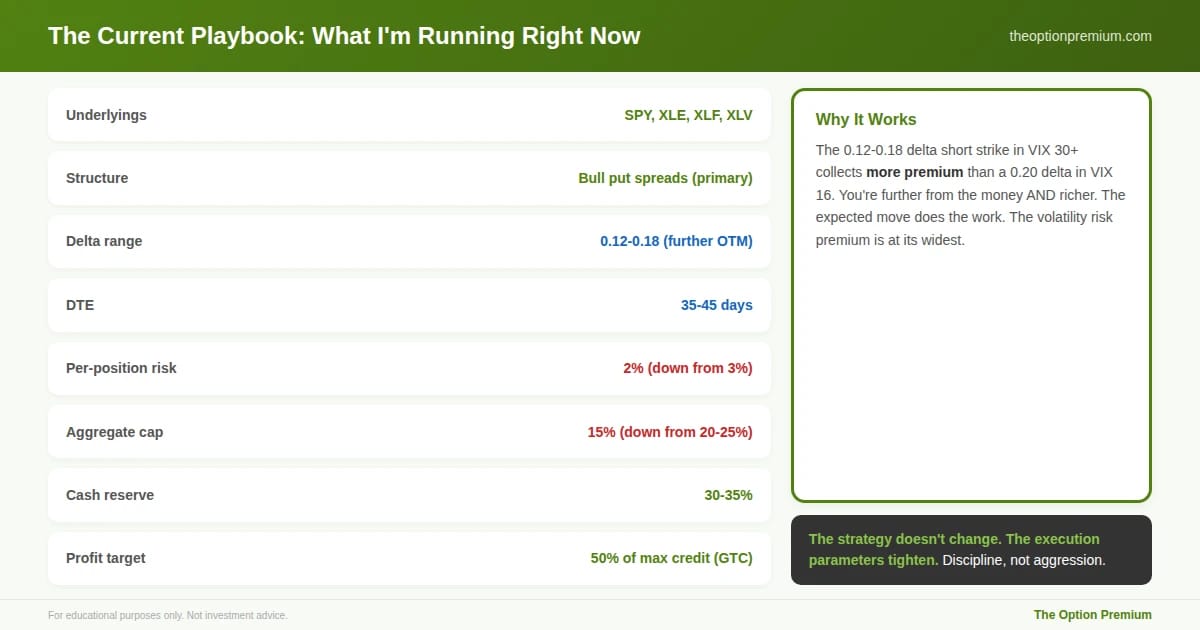

Underlyings: SPY (core), sector ETFs (XLE, XLF, XLV) where IVP is above 70%. Liquid markets only. No illiquid single stocks where bid-ask spreads widen to $0.30+ during volatility.

Structure: Bull put credit spreads as the primary vehicle. Iron condors when ADX is below 20 (range-bound), which is rare in the current environment. Most of the time, the market has a directional lean, so single-sided spreads (puts in a declining market, calls in a rallying one) are more appropriate.

Delta: 0.12-0.18 on the short strike. Further OTM than my normal 0.15-0.20 range. The wider strikes still collect more premium than a 0.20 delta trade in moderate IV.

DTE: 35-45 days. Standard entry window. No weeklies. The daily swings in this environment make weekly options even more dangerous than usual.

Sizing: 2% per position (down from 3%). Aggregate cap at 15%. Cash reserve at 30-35%. I want dry powder available if VIX spikes to 40+ and premiums get even richer.

Profit target: 50% of max credit. GTC limit order at entry. Close the morning the order fills, don't hold for more.

Hedging: This is where I actually reduce hedge allocation slightly, because my existing hedges from the low-VIX period are already working (the puts I bought at VIX 16 are worth 2-3x now). I take partial profits on hedges and set aside the proceeds to re-establish when VIX normalizes.

The specific parameters I'm running in this VIX 30+ environment. Underlyings: SPY and sector ETFs (XLE, XLF, XLV) where IVP is above 70%. Structure: bull put spreads (single-sided, directional lean appropriate). Delta: 0.12-0.18 (further OTM than normal, still richer premium). DTE: 35-45 days. Size: 2% per position (down from 3%), 15% aggregate cap. Cash: 30-35% reserved for further deployment if VIX spikes to 40+. The 0.12-0.18 delta at VIX 30+ collects more premium than a 0.20 delta at VIX 16. Further from the money AND richer.

Risk Reality Check

Elevated volatility is a seller's market, but it's not a free lunch. The same VIX that inflates premiums also means the market moves 1-2% daily. A credit spread that's 10% OTM can be tested in a week if the market drops 8%. The Iran conflict, tariff negotiations, Fed decisions, and earnings season can all produce overnight gaps that blow through your strikes.

This is why position sizing and cash reserves are non-negotiable. In a calm market (VIX 15), a 3-loss streak costs 9% of your account at 3% per trade. In a high-volatility market, those losses are more likely to cluster because the events causing the volatility affect multiple positions simultaneously. By reducing to 2% per trade and 15% aggregate, a 3-loss streak costs 6%, which is recoverable with a month of disciplined trading.

The traders who get hurt in high-volatility environments aren't the ones who sell premium. They're the ones who sell too much premium, size too aggressively, skip their hedges, and abandon their profit targets. The strategy doesn't change in high volatility. The execution parameters tighten.

Key Takeaways

Elevated VIX (currently above 30) creates a structural advantage for premium sellers: the same 0.16 delta credit spread that collects $1.05 in moderate IV collects $1.80-$2.20 now. Same probability of success, same strike distance relative to the expected move, 50-100% richer premium. This is the mathematical definition of a seller's market.

The expected move widens in your favor. At VIX 30, your 0.16 delta short strike on SPY is 10%+ from the current price versus 5% at VIX 15. Elevated volatility doesn't just pay you more. It gives you more room to be wrong. And historically, implied volatility exceeds realized volatility 80-85% of the time, a gap that widens in fearful environments.

Adjust execution, not strategy. Sell further from the money (0.12-0.18 delta). Maintain 30-60 DTE. Reduce position size to 2% (down from 3%). Lower aggregate cap to 15%. Close at 50% of max profit without exception. Keep 30-35% cash reserves for further deployment if premiums get even richer.

Statistics are your foundation. An 85% probability credit spread in elevated IV produces +$76.25 expected value per trade versus +$46.50 in moderate IV. Same risk profile, 64% more income. Over 20 trades per cycle, that's $1,525 versus $930. The math doesn't lie, and the math is heavily in the seller's favor right now.

Stay disciplined, not aggressive. Elevated volatility tests your emotions daily. The premium sellers who compound through these environments don't get greedy. They take their 50%, manage their risk, keep their hedges, and let the probabilities play out over dozens of trades. This is the seller's market we've been preparing for. Don't waste it by oversizing.

The options market is offering us the richest premiums we've seen since last April's tariff shock. The probabilities haven't changed. The payoff per probability point has. Use it wisely, stay disciplined, and let the statistics do what they've always done.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply