- The Option Premium

- Posts

- Credit Spread Width: $2, $5, or $10 Wide?

Credit Spread Width: $2, $5, or $10 Wide?

Learn which credit spread width is right for your account. Compare $2, $5, and $10 wide spreads on ROC, max loss, 100-trade performance, and a 3-variable decision framework for matching width to your situation.

Andrew Crowder

March 07, 2026

Credit Spread Width: $2, $5, or $10 Wide?

You've selected your short strike by delta. You've confirmed the IV environment. Now comes the question that determines your risk profile for the entire trade: how wide should the spread be?

Spread width is one of the most overlooked decisions in credit spread trading. Most educational content treats it as an afterthought, a fixed variable you set once and forget. But the distance between your short and long strikes directly controls your maximum loss, your return on capital, your capital efficiency, and how many spreads you can run simultaneously. Getting the width right is just as important as getting the delta right.

This guide breaks down the three most common spread widths, when each makes sense, and how to match width to your account size and strategy.

What Spread Width Actually Controls

The width of a credit spread is the distance between the short strike and the long strike. On a $190/$185 bull put spread, the width is $5. On a $190/$180 bull put spread, the width is $10. Same short strike, same delta, same probability of profit, but two very different risk profiles.

Width controls four things simultaneously.

Maximum loss. Spread width minus net credit, times 100. A $5 wide spread with a $1.50 credit has a max loss of $350. A $10 wide spread on the same short strike might collect $2.20 in credit with a max loss of $780. Wider spreads risk more dollars per contract.

Return on capital. The $5 spread produces 42.9% ROC ($1.50 / $3.50). The $10 spread produces 28.2% ROC ($2.20 / $7.80). Narrower spreads are more capital-efficient on a percentage basis because the long option captures more of the short option's premium.

Premium collected. Wider spreads collect more total credit because the long option is further from the money and cheaper. But the additional credit doesn't scale linearly with the additional risk. Going from $5 to $10 wide doubles your risk but typically adds only 30-50% more credit.

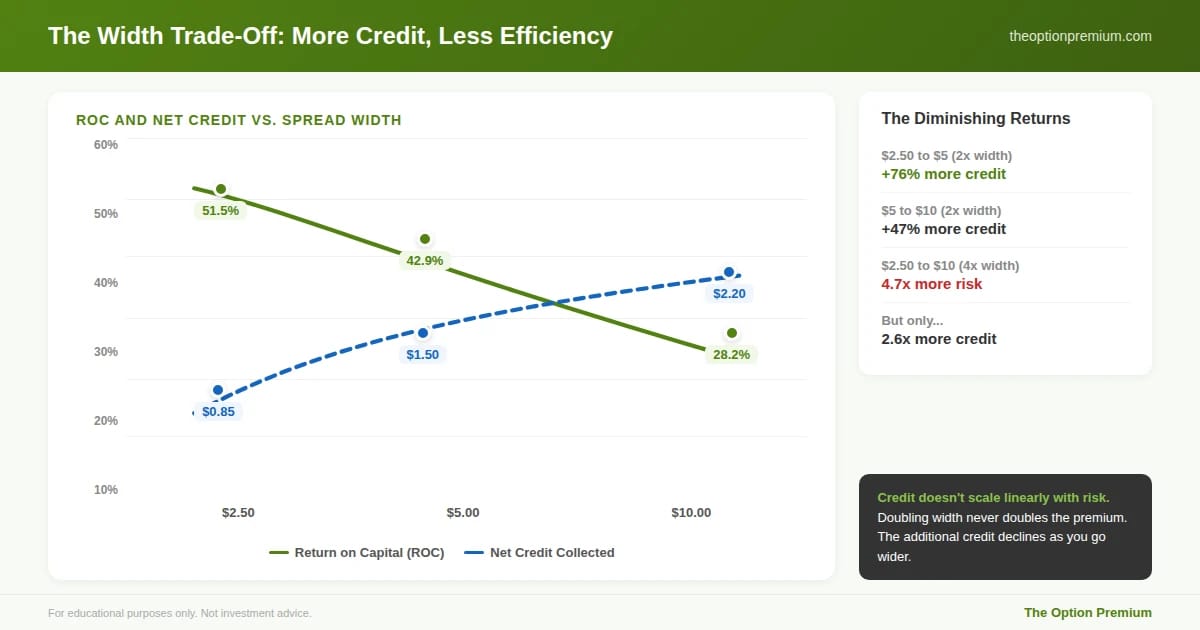

The width trade-off visualized. As width increases, net credit rises (blue dashed line) but ROC declines (green solid line). Credit doesn't scale linearly with risk: going from $2.50 to $5 adds 76% more credit, but $5 to $10 adds only 47% more. Meanwhile, going from $2.50 to $10 wide means 4.7x more risk for just 2.6x more credit.

Number of contracts. For a fixed amount of risk capital, narrower spreads let you trade more contracts. If you're willing to risk $1,000 on a trade, you can do roughly 3 contracts of a $5 wide spread ($350 max loss each) or 1 contract of a $10 wide spread ($780 max loss). More contracts doesn't mean more risk if the total dollar exposure is the same, but it does affect how you scale in and out.

The Three Standard Widths Compared

Let's run the same short strike through all three common widths to see exactly how the numbers change.

Setup: Stock at $200. Sell the 0.20 delta put at $190. Expiration: 35 DTE.

$2.50 wide ($190/$187.50). Net credit: $0.85. Max loss: $1.65. ROC: 51.5%. Max loss per contract: $165. Breakeven: $189.15 (5.4% buffer).

$5 wide ($190/$185). Net credit: $1.50. Max loss: $3.50. ROC: 42.9%. Max loss per contract: $350. Breakeven: $188.50 (5.75% buffer).

$10 wide ($190/$180). Net credit: $2.20. Max loss: $7.80. ROC: 28.2%. Max loss per contract: $780. Breakeven: $187.80 (6.1% buffer).

Notice the pattern. As width increases, you collect more credit and get a slightly better breakeven, but your ROC decreases and your max loss per contract increases substantially. The $10 wide spread collects 2.6x the credit of the $2.50 wide spread but carries 4.7x the max loss.

This is the core trade-off: wider spreads collect more dollars but use those dollars less efficiently.

Same short strike, three widths. $2.50 wide: highest ROC (51.5%), lowest max loss ($165), least credit ($0.85). $5 wide: best balance (42.9% ROC, $350 max loss, $1.50 credit). $10 wide: most credit ($2.20) but highest risk ($780), lowest ROC (28.2%). The $10 spread collects 2.6x the credit of the $2.50 but carries 4.7x the max loss.

When to Use $2-$2.50 Wide Spreads

Narrow spreads are the scalpel of credit spread trading. Small, precise, capital-efficient.

Small accounts. If your account is under $25,000, $2.50 wide spreads let you diversify across more positions without concentrating too much risk in any single trade. A $165 max loss per contract is manageable for a $10,000-$25,000 account. You can run 4-5 different spreads without exceeding a 3-5% risk allocation per position.

High-frequency approach. Traders who sell credit spreads frequently (weekly or bi-weekly) benefit from narrow widths because the higher ROC compounds more efficiently over many trades. A 50% ROC realized over 30 days, repeated 10-12 times per year, is a powerful engine even at small dollar amounts per trade.

Learning phase. If you're still building experience with credit spreads, $2.50 wide spreads limit your tuition costs. Losing $165 while learning management techniques is more sustainable than losing $780.

The downside. Transaction costs eat a larger percentage of the credit on narrow spreads. If you're paying $0.65 per contract and selling a 4-leg position for $0.85 credit, commissions consume 3% of your max profit. On wider spreads collecting $2.20, that same commission is just over 1%. Also, narrow spreads require a higher win rate to overcome the less favorable risk-reward ratio.

When to Use $5 Wide Spreads

Five-dollar spreads are the workhorse width for most retail credit spread traders, and for good reason. They balance efficiency, risk, and practicality better than either extreme.

Medium accounts ($25,000-$100,000). At this account size, $5 wide spreads offer meaningful income per trade ($150 credit in our example) without requiring excessive position sizing. A $350 max loss represents 1.4% of a $25,000 account or 0.35% of a $100,000 account, well within the 3-5% risk guidelines.

Standard position sizing. Five-dollar spreads produce clean math. Risk roughly 2-3 contracts per position for a total max exposure of $700-$1,050. That's a comfortable range for most mid-sized accounts.

Best ROC-to-risk balance. The 42.9% ROC on a $5 wide spread sits in the productive zone: high enough to generate meaningful returns over time, but with manageable per-trade risk. You don't need an extremely high win rate to be profitable, and the credit collected per contract is large enough to absorb transaction costs easily.

My default choice. I use $5 wide spreads on underlyings priced under $200 as my standard width. It's the default I adjust away from only when there's a specific reason to go narrower or wider.

When to Use $10 Wide Spreads

Wide spreads are the power tool. More dollars at risk, more dollars collected, but less forgiving.

Larger accounts ($100,000+). At this account size, a $780 max loss per contract is a small percentage of the portfolio. Wide spreads let you collect meaningful income without needing to manage a high number of contracts. One contract of a $10 wide spread is simpler to manage than three contracts of a $2.50 wide spread.

Higher-priced underlyings. On stocks or ETFs trading above $300-$500, $5 wide spreads can produce awkward strike intervals and thin premiums. A $10 width provides more proportional risk relative to the underlying's price range. I shift to $10 wide spreads on any underlying above $200 and sometimes above $150 when strike intervals allow.

Fewer contracts, simpler management. Each contract of a $10 wide spread does more work. If your portfolio strategy calls for a specific dollar amount of income from a position, you can achieve it with fewer contracts, which means simpler adjustment and exit mechanics.

The downside. The lower ROC (28.2% in our example) means you need a higher win rate or longer time horizon to generate the same percentage returns as narrower spreads. And max loss per contract is substantial. A losing trade hits harder in dollar terms, even if it's a smaller percentage of a large account. The psychological impact of a $780 loss versus a $165 loss is real, regardless of account size.

The Real Decision: Dollar Risk Per Trade

Here's what most width discussions miss: the right width isn't about which one is "better." It's about controlling your dollar risk per trade to match your account size and risk tolerance.

Consider this reframing. You've decided to risk $1,000 on a single credit spread position. Here's how width changes what that $1,000 buys you.

$2.50 wide: 6 contracts. Total credit: $510. Total max loss: $990. ROC: 51.5%.

$5 wide: 3 contracts. Total credit: $450. Total max loss: $1,050. ROC: 42.9%.

$10 wide: 1 contract. Total credit: $220. Total max loss: $780. ROC: 28.2%.

All three positions risk roughly the same dollar amount. But the $2.50 width generates $510 in potential profit versus $220 for the $10 width on similar risk. The narrower spread is more capital-efficient because you're deploying more contracts at a higher ROC per contract.

The trade-off is complexity. Six contracts require more attention when rolling or closing. One contract is simpler. For traders who actively manage their positions, the complexity is worth the efficiency. For traders who prefer simplicity, the wider spread is cleaner.

Same $1,000 risk budget, three structures. $2.50 wide (6 contracts): $510 total credit, most capital-efficient. $5 wide (3 contracts): $450 total credit, best overall balance. $10 wide (1 contract): $220 total credit, simplest to manage. Narrower spreads generate more profit on similar risk.

Width and the 1/3 Credit Rule

The 1/3 rule states that you should collect at least 1/3 of the spread width in total credit. This rule interacts with width in an important way.

Narrow spreads pass the 1/3 rule more easily. A $2.50 wide spread needs $0.83 in credit to hit the 1/3 threshold. In moderate IV environments, this is achievable at 0.20 delta on most liquid underlyings.

Wide spreads struggle in low IV. A $10 wide spread needs $3.33 to hit the 1/3 threshold. In a low-IV environment, this is often impossible at reasonable delta levels. You'd need to move to 0.30+ delta to collect enough, which breaks your probability framework.

This means IV environment and width are linked. When IV is low, narrow spreads are more likely to produce acceptable ROC. When IV is elevated, wider spreads become viable because the extra premium fills the 1/3 ratio at sensible delta levels. Let the IV environment inform your width choice, not just your delta choice.

Matching Width to Your Account: A Sizing Framework

Here's the framework I use and recommend.

Account under $25,000. Default to $2.50 wide spreads. Max 2-3% of account at risk per position. This means 1-2 contracts per trade ($165-$330 max loss). Run 3-5 simultaneous positions for diversification.

Account $25,000-$75,000. Default to $5 wide spreads. Max 3-5% of account at risk per position. This means 2-4 contracts per trade ($700-$1,400 max loss). Run 4-6 simultaneous positions.

Account $75,000-$200,000. Mix $5 and $10 wide spreads depending on underlying price. Max 3-5% risk per position. Run 5-8 simultaneous positions across sectors and expirations.

Account above $200,000. $10 wide spreads as default, with $5 wide on lower-priced underlyings. Max 2-3% risk per position. The dollar amounts are large enough per trade that position count can stay moderate (5-10 positions).

In every case, the total portfolio risk across all open positions should not exceed 20-25% of account value. This ensures that even a worst-case scenario where multiple positions hit max loss simultaneously doesn't destroy the account.

Match width to account size. Under $25K: $2.50 wide, 1-2 contracts, 2-3% risk. $25K-$75K: $5 wide, 2-4 contracts, 3-5% risk. $75K-$200K: mix $5/$10 by underlying price, 5-8 positions. Above $200K: $10 wide default, 5-10 positions. Total portfolio risk: never exceed 20-25%.

Common Width Mistakes

Using the same width on every underlying. A $5 spread on a $50 stock (10% of share price) is proportionally very different from a $5 spread on a $500 stock (1% of share price). Scale your width to the underlying's price.

Going wider to collect more premium without adjusting contracts. Switching from 3 contracts of $5 wide ($1,050 max loss) to 3 contracts of $10 wide ($2,340 max loss) more than doubles your risk. If you go wider, reduce your contract count proportionally.

Ignoring the long strike's liquidity. The further OTM your long option, the wider the bid-ask spread tends to be. On a $10 wide spread, your long strike might have a $0.15-$0.20 bid-ask spread. That slippage costs you on entry and exit. Always check liquidity on both legs.

Defaulting to the widest available. Wider isn't inherently better. It's just different. Match width to your account, the underlying's price, the IV environment, and your management preferences.

Risk Reality Check

The maximum loss on any single credit spread should never represent more than 3-5% of your account. This is true regardless of width. A $2.50 wide spread at 6 contracts can risk the same dollar amount as a $10 wide spread at 1 contract. The width changes the structure, not the risk, as long as you size correctly.

The real danger is treating wider spreads as "the same trade, just bigger." They're not. A $10 wide spread that hits max loss takes 4-5 winning trades to recover from. A $2.50 wide spread that hits max loss takes 2-3 winning trades to recover. The recovery math should influence your width choice.

Key Takeaways

Spread width controls maximum loss, return on capital, premium collected, and how many contracts you can run. Wider spreads collect more dollars but use those dollars less efficiently (lower ROC). Narrower spreads are more capital-efficient but require more contracts for the same dollar income.

The three standard widths serve different purposes. $2.50 wide for small accounts and high-frequency trading (highest ROC, lowest dollar risk). $5 wide as the workhorse default for most retail traders (best balance of ROC and dollar risk). $10 wide for large accounts and higher-priced underlyings (fewer contracts, simpler management).

Reframe the decision around dollar risk per trade, not width alone. All three widths can risk the same $1,000, but narrower spreads generate more potential profit on similar risk because ROC is higher.

IV environment and width are linked. Narrow spreads pass the 1/3 credit rule more easily in low IV. Wide spreads become viable when IV is elevated. Let IV inform your width, not just your delta.

Match width to account size: under $25K use $2.50, $25K-$75K use $5, $75K-$200K mix $5 and $10, above $200K default to $10. Total portfolio risk should never exceed 20-25% of account value across all positions.

Width isn't about finding the best option. It's about finding the right fit for your account, your strategy, and the trade in front of you.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply