- The Option Premium

- Posts

- You've Been Doing Covered Calls Wrong. Here's the Smarter Way to Think About Them.

You've Been Doing Covered Calls Wrong. Here's the Smarter Way to Think About Them.

A covered call and a short put at the same strike have identical risk profiles. Same P&L at every price. Same Greeks. The only difference: $15,000 in capital vs. $3,000. The risk equivalence that changes how professionals deploy capital.

Andrew Crowder

April 19, 2026

You've Been Doing Covered Calls Wrong. Here's the Smarter Way to Think About Them.

The covered call is the first strategy most options traders learn. Buy 100 shares of stock. Sell a call against them. Collect premium. Feel safe.

And it does feel safe. You own the stock. The short call is "covered" by your shares. If the stock goes up, you participate in the gains up to the strike price. If the stock goes down, you still own the shares and the premium you collected reduces your cost basis. Your broker doesn't even require margin because the position is fully collateralized. Everything about it feels conservative, prudent, and well-protected.

But here's the problem. The covered call's risk profile is not what most traders think it is. And once you understand what a covered call actually is, in terms of its risk equivalence, it changes the way you think about capital allocation, strategy selection, and whether the covered call deserves the outsized place it holds in most options portfolios.

This isn't about whether covered calls work. They do. This is about whether the covered call is the most efficient way to express the same trade thesis. In most cases, it isn't. And the capital you're tying up in covered calls could be deployed far more efficiently if you understood the synthetic relationship hiding inside the position.

The Risk Equivalence Most Traders Never Learn

Here's the insight that changed my approach early in my career, and it's one of the most important concepts in options theory.

A covered call has the exact same risk profile as a short put at the same strike.

Not similar. Not roughly equivalent. The same. A covered call and a naked short put at the same strike, in the same expiration, produce identical profit and loss at every price point at expiration.

Let me show you why.

A covered call is two positions: long 100 shares of stock and short one call option. Suppose you own 100 shares of a stock at $150 and you sell the $155 call for $3.00.

If the stock is at $155 at expiration, you keep the $3.00 premium and your shares get called away at $155. Total profit: $5.00 (stock gain) + $3.00 (premium) = $8.00 per share.

If the stock is at $145 at expiration, the call expires worthless. You keep the $3.00 premium but your shares are worth $5.00 less. Net: $3.00 - $5.00 = -$2.00 per share.

If the stock is at $130 at expiration, the call expires worthless. You keep $3.00 but your shares are down $20.00. Net: -$17.00 per share.

Now look at a short $155 put on the same stock, same expiration, collecting a $8.00 credit (which is approximately what the $155 put would command on a $150 stock with $3 of extrinsic value in the call, because of put-call parity).

Actually, let me make the comparison even cleaner. Consider the at-the-money case. You own 100 shares at $150 and sell the $150 call for $5.00. Compare that to selling the $150 put for $5.00.

Covered call (long stock at $150, short $150 call for $5.00): Stock at $160: shares called away at $150, profit = $5.00 (premium only). Max gain = $5.00. Stock at $150: call expires worthless, shares unchanged. Profit = $5.00 (premium). Stock at $145: call expires, shares down $5, net = $5.00 - $5.00 = $0.00 (breakeven). Stock at $130: call expires, shares down $20, net = $5.00 - $20.00 = -$15.00.

Short $150 put for $5.00: Stock at $160: put expires worthless. Profit = $5.00. Max gain = $5.00. Stock at $150: put expires worthless. Profit = $5.00. Stock at $145: put is $5 in the money, loss on put = $5. Net = $5.00 - $5.00 = $0.00 (breakeven). Stock at $130: put is $20 in the money, loss = $20. Net = $5.00 - $20.00 = -$15.00.

Every line is identical. The maximum gain is the same. The breakeven is the same. The loss at every price point is the same. The covered call and the short put are the same trade expressed in two different ways.

This is not a coincidence. It's a mathematical identity called put-call parity, and it holds for all European-style options and very closely for American-style options (with minor differences from dividends and early exercise).

The proof that a covered call and a short put at the same strike are the same trade. Every line is identical: max gain ($5.00), breakeven ($145), and loss at every price below breakeven. The covered call requires $15,000 of stock ownership. The short put requires approximately $3,000 in margin. Same risk profile. One-fifth the capital. This is not approximate. It's a mathematical identity from put-call parity, and it holds at every price point at expiration.

Why This Matters: The Capital Efficiency Problem

If the risk profile is identical, why does it matter which structure you use? Because the capital requirements are radically different.

A covered call on a $150 stock requires you to own 100 shares. That's $15,000 of capital committed to one position. If you have a $100,000 account, a single covered call consumes 15% of your portfolio in one name.

A short put on the same stock, same strike, same expiration, requires approximately $2,500 to $3,500 in margin (depending on your broker and account type). That's roughly one-fifth to one-quarter of the capital for the same risk profile.

The remaining $11,500 to $12,500 that would have been locked in the stock can be deployed elsewhere. It can sit in treasury bills earning interest. It can be used as buying power for additional positions on uncorrelated underlyings. It can serve as your cash reserve. It can be the capital that funds your next three credit spreads or iron condors.

This is the capital efficiency argument, and it's the reason professionals overwhelmingly prefer selling puts to running covered calls when the thesis is the same: neutral-to-bullish, collect premium, willing to own at a lower effective cost basis.

I've written extensively about this in the context of the capital efficiency hybrid: LEAPS for stock exposure at a fraction of the capital, short puts for income generation on freed capital, and covered calls only when shares are actually assigned and you want to continue collecting premium on a position you already hold.

The capital efficiency argument in one image. A $100,000 account running covered calls at $15,000 per position can hold 3-4 names with minimal diversification and high concentration risk. The same account running short puts at $3,000 margin per position can hold 10-15 positions across 8-12 uncorrelated sectors while maintaining a 20-30% cash reserve. Same risk profile per trade. Radically different portfolio. The capital efficiency of short puts enables the diversification that covered calls prevent.

The Delta and Theta Match

If you're skeptical that the risk profiles are truly identical, look at the Greeks.

A covered call (long 100 shares, short one ATM call) has a net delta of approximately +50. You're long 100 deltas from the stock and short roughly 50 deltas from the call. Net: +50.

A short ATM put has a delta of approximately +50. It responds to a $1 move in the stock by approximately the same amount as the covered call.

The theta is also matched. The short call in the covered call position generates time decay at approximately the same rate as the short put at the same strike and expiration. Both positions are collecting premium from the passage of time. Both benefit from implied volatility declining after entry.

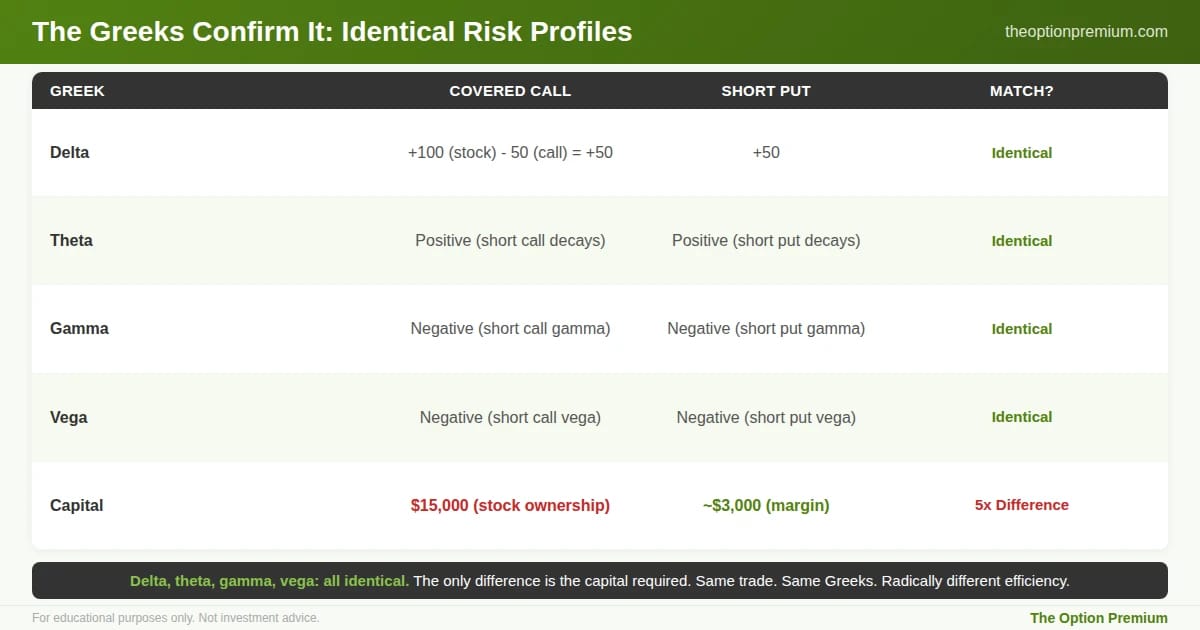

The gamma, vega, and rho characteristics are also equivalent. The covered call and the short put are the same position. The Greeks confirm it.

The Greeks confirm the risk equivalence. Delta: covered call is +100 (stock) minus 50 (short call) = +50. Short put: +50. Identical. Theta: both are positive (both collect time decay). Gamma: both are negative (both get worse as the stock moves against them). Vega: both are negative (both lose when IV increases). Every Greek matches. The only difference is the capital required: $15,000 in stock ownership for the covered call versus approximately $3,000 in margin for the short put. Same trade. Same Greeks. 5x the efficiency.

So When Do Covered Calls Actually Make Sense?

If short puts are more capital efficient and produce the same risk profile, why would anyone ever run a covered call? There are specific situations where the covered call is the correct structure.

When you already own the shares. If you were assigned on a cash-secured put and now hold 100 shares, selling a call against those shares is the natural continuation of the wheel strategy. You didn't buy the shares to run a covered call. You acquired them through assignment. Now you're managing an existing position by collecting premium while waiting for the shares to recover to your target exit price. This is the most legitimate use of covered calls.

When you want the dividend. Stock ownership entitles you to dividends. A short put does not. If the stock pays a meaningful dividend and you want that income stream in addition to the option premium, the covered call captures both. For high-dividend stocks (utilities, REITs, certain financials), the dividend can represent a significant portion of the total return, and the covered call is the structure that collects it.

When you want long-term capital gains treatment. Shares held for over one year qualify for long-term capital gains tax rates, which are lower than short-term rates. Option premium is always taxed as short-term gains regardless of holding period. If you're running covered calls on shares you've held for over a year, the stock appreciation (if any) receives favorable tax treatment. This doesn't apply to most active premium sellers, but it matters for investors who are adding options to an existing long-term stock portfolio.

When you need to manage an in-the-money option with a wide bid-ask spread. This is a more advanced application. If you're short an option that's deep in the money and the bid-ask spread is wide, it can be cheaper to exercise or get assigned and then close the stock position (which always has a tight spread) than to buy back the option at an unfavorable price. Understanding the synthetic equivalence gives you this alternative exit path.

When Short Puts Are the Better Choice

For a premium seller who is starting fresh with no existing stock position, the short put is almost always the more efficient expression of the same thesis. Here's the framework I use.

Your thesis is neutral-to-bullish. You think the stock will stay flat or go up. You want to collect premium. You're willing to own the stock if it drops to your strike. This is the exact thesis of both a covered call and a short put. The short put expresses it with one-fifth the capital.

You want portfolio diversification. The $15,000 locked in a covered call could fund five $3,000 short put positions across five uncorrelated underlyings. Five positions at 2-5% risk each with uncorrelated underlyings is a more resilient portfolio than one position consuming 15% of the account in a single name. The capital efficiency of short puts enables the diversification that covered calls prevent.

You're trading in elevated IV. When IV Percentile is above 50 and you want to sell premium, the short put captures the rich premium without requiring stock ownership. You're selling volatility risk premium, not investing in the stock. The short put is the pure expression of that trade.

You want to manage defined risk. A short put can be paired with a long put to create a bull put spread with defined risk. A covered call cannot easily be converted to a defined-risk structure without selling the shares (which defeats the purpose). If your risk management requires defined max loss on every position, the put spread is the structure and the covered call is not.

The decision framework: default to short puts for new premium-selling positions. Switch to covered calls when you have a specific reason to own the stock. Short puts win when starting fresh (5x less capital), when you want diversification (freed capital funds 5x more positions), in elevated IV (pure premium collection), and when you want defined risk (pair with a long put for a bull put spread). Covered calls win when you already own shares from assignment, want the dividend, want long-term capital gains treatment, or need to manage in-the-money options with wide bid-ask spreads.

The Other Synthetic You Should Know: Protective Put = Long Call

There's a second risk equivalence that follows directly from the first, and it's equally useful.

Long stock plus a long put (the "protective put" or "married put") has the same risk profile as a long call at the same strike.

Think about it. If you own 100 shares at $150 and buy the $150 put for $5.00, your downside is capped at $145 (stock at $150 minus put premium). Your upside is unlimited above $155 (the stock appreciates beyond the premium cost). That's the same payoff as buying the $150 call for $5.00: max loss of $5.00, unlimited upside above $155.

The practical application: if you're considering a protective put on shares you own, compare the cost to simply buying a call. They have the same risk profile. The call is usually simpler to manage and doesn't require holding the stock position. If the protective put costs more than the equivalent call (which can happen due to put skew and bid-ask differences), the call is the cheaper way to get the same exposure.

Understanding these synthetic relationships doesn't change the math. It changes your flexibility. When you know that every stock-plus-option combination has an option-only equivalent, you can always choose the more capital-efficient version.

The Practical Framework: How I Think About It Now

After 24 years, here's how I actually use this knowledge in practice.

Default to short puts for new premium-selling positions. Unless I have a specific reason to own the stock (dividend, tax treatment, existing position), I sell puts rather than running covered calls. Same risk profile. Less capital. More flexibility.

Use covered calls to manage assigned shares. When a short put results in assignment (which happens, and is part of the plan when you sell puts on stocks you'd be willing to own), I sell calls against the assigned shares to continue collecting premium. The covered call becomes a management tool, not an entry strategy.

Think in terms of risk equivalents when managing positions. If a short put is deep in the money and the bid-ask is wide, I consider taking assignment and immediately selling the shares rather than buying back the put at an unfavorable price. If a covered call is approaching max profit and the short call is deep in the money with a wide spread, I consider letting assignment happen and moving on rather than buying back an expensive option.

Never tie up $15,000 in a covered call when $3,000 in a short put creates the same exposure. The freed capital goes into the cash reserve, into additional diversified positions, or into treasury bills earning risk-free interest. Capital efficiency isn't a minor consideration. Over a full year across a portfolio, the difference between 15% of capital per position (covered calls) and 3% per position (short puts) is the difference between running 3 positions and running 15 positions. That's the difference between concentrated risk and a diversified portfolio.

Risk Reality Check

The covered call and the short put share the same risk: substantial downside if the stock drops significantly. Calling a covered call "safe" because the short call is covered doesn't change the fact that you can lose 20%, 30%, or 50% of the stock's value during a downturn. The call premium provides a small buffer, but it doesn't protect against a major decline.

Similarly, calling a short put "risky" because it's "naked" doesn't change the fact that its risk is mathematically identical to the covered call everyone considers safe. The perception of risk and the actual risk are two different things, and understanding synthetic equivalence is what separates the two.

Both structures require the same discipline: sell on stocks you'd be willing to own, at strikes that represent attractive entry prices, in elevated IV environments, at appropriate position sizing. The structure changes. The principles don't.

Key Takeaways

A covered call (long stock + short call) has the identical risk profile as a short put at the same strike. This is not approximate. At every price point at expiration, the profit and loss are the same. The delta, theta, gamma, and vega are matched. This is a mathematical identity from put-call parity.

The capital efficiency difference is dramatic. A covered call on a $150 stock requires $15,000 in stock ownership. A short put at the same strike requires approximately $2,500-$3,500 in margin. Same risk. One-fifth the capital. The freed capital enables diversification across 5x more positions on uncorrelated underlyings.

Covered calls make sense in specific situations: when you already own shares (from assignment), when you want dividends, when you want long-term capital gains treatment, or when you need to manage in-the-money options with wide bid-ask spreads. For new premium-selling positions with no existing stock ownership, the short put is almost always the more efficient structure.

The second synthetic: long stock + long put (protective put) = long call. If you're considering a protective put, compare the cost to buying the equivalent call. Same payoff, often simpler and cheaper.

The practical framework: default to short puts for new positions, use covered calls to manage assigned shares, think in risk equivalents when managing wide bid-ask situations, and never tie up $15,000 in a covered call when $3,000 in a short put creates the same exposure. Capital efficiency is what turns a 3-position portfolio into a 15-position portfolio. That's the difference between concentrated risk and genuine diversification.

The covered call isn't wrong. It's just incomplete. Understanding what a covered call actually is, in terms of its risk equivalence, frees you to make better capital allocation decisions. The smartest covered call you'll ever "run" might be the short put you sell instead.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply