- The Option Premium

- Posts

- Cash-Secured Puts Explained: Your Complete Guide to Selling Puts for Income

Cash-Secured Puts Explained: Your Complete Guide to Selling Puts for Income

Learn how cash-secured puts work with a step-by-step example, the 4 structural advantages of selling puts, strike and expiration selection, trade management rules, and position sizing for consistent income.

Andrew Crowder

March 21, 2026

Cash-Secured Puts Explained: Your Complete Guide to Selling Puts for Income

If someone asked me to recommend the single best strategy for a new premium seller to learn first, it would be the cash-secured put. Not because it's the most sophisticated. Not because it generates the biggest returns. But because it teaches you everything that matters about selling options: collecting premium, managing probability, understanding assignment, and learning to profit from stocks you'd be happy to own.

A cash-secured put is the entry point to an entire income-generating framework. It's the first phase of the Wheel Strategy. It's the foundation that covered calls, credit spreads, and more advanced structures all build upon. Master this one strategy and you'll understand 80% of what premium selling is really about.

What Is a Cash-Secured Put?

A cash-secured put means you sell a put option on a stock while holding enough cash in your account to buy 100 shares if you're assigned. That's it. You collect premium upfront in exchange for agreeing to buy the stock at the strike price if the stock falls below that level by expiration.

The "cash-secured" part is critical. It means you have the full collateral set aside. You're not using margin. You're not leveraging beyond what you can cover. If you sell a put at a $50 strike, you have $5,000 in cash reserved to purchase those 100 shares.

Here's the mental model that makes cash-secured puts click: think of it as getting paid to place a limit order. You already want to buy a stock, but instead of placing a buy order at your target price and waiting, you sell a put at that price and collect income while you wait. If the stock drops to your price, you buy it at a discount (your strike minus the premium collected). If the stock never drops that far, you keep the premium and move on to the next opportunity.

How a Cash-Secured Put Works: Step by Step

Let's walk through a real example using round numbers.

You're interested in buying shares of a stock currently trading at $100. You'd be comfortable owning it at $95, but you'd prefer to get paid while waiting for that price.

You sell one $95 put expiring in 30 days and collect $1.50 in premium ($150 per contract).

Now three scenarios play out.

Scenario 1: Stock stays above $95. The put expires worthless. You keep the $150 and your $9,500 in collateral is released. Your return: $150 on $9,500 reserved capital, or 1.58% in 30 days. Annualized, that's roughly 19%. You never bought the stock and you got paid for being willing to.

Scenario 2: Stock drops to $93. You're assigned 100 shares at $95. But because you collected $1.50 in premium, your effective cost basis is $93.50. The stock is at $93, so you're down $0.50 per share on paper. But you bought at a discount to where the stock was when you entered the trade, and you can now sell covered calls against those shares to continue generating income.

Scenario 3: Stock drops to $80. You're assigned at $95 with a cost basis of $93.50. The stock is at $80, so you're sitting on a $13.50 per share unrealized loss. This is the risk. The premium cushion helped, but a significant decline still results in meaningful losses. This is why stock selection matters more than any other variable.

Three outcomes of selling a $95 cash-secured put on a $100 stock for $1.50 premium. Most commonly (Scenario 1) the stock stays above the strike and you keep $150, a 1.58% return in 30 days. If assigned (Scenario 2), your effective cost basis is $93.50. Significant declines (Scenario 3) show why stock selection matters more than any other variable.

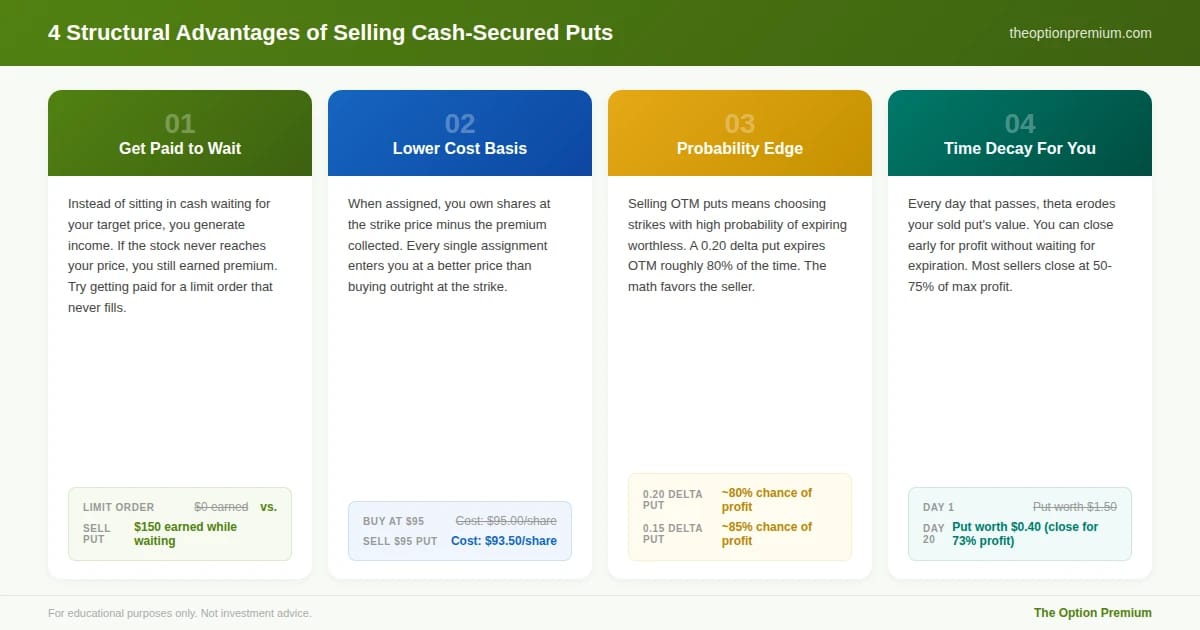

Why Sell Cash-Secured Puts? The Seller's Edge

The appeal of cash-secured puts comes down to four structural advantages that buying stock outright doesn't offer.

You get paid to wait. Instead of sitting in cash waiting for your target price, you generate income. If the stock never reaches your price, you still earned premium. Try getting your brokerage to pay you for a limit order that never fills.

Your cost basis is always lower. When assigned, you own shares at the strike price minus premium collected. On every single assignment, you enter the position at a better price than if you'd simply bought at the strike.

Probability is on your side. When you sell OTM puts, you're choosing strikes with a high probability of expiring worthless. A 0.20 delta put has roughly an 80% chance of expiring OTM. You keep the premium without ever buying the stock roughly eight out of ten times.

Time decay works for you. Every day that passes, your sold put loses value thanks to theta decay. You can close the position early for a profit without waiting for expiration. Most experienced sellers close at 50-75% of maximum profit rather than holding to expiration.

Four advantages that buying stock outright can't match: getting paid to wait (vs. $0 for a limit order), always entering at a lower cost basis, an 80% probability edge at 0.20 delta, and closing early at 50-75% profit as theta decay works in your favor.

Choosing the Right Stock: The Most Important Decision

The single biggest mistake I see from newer put sellers is choosing stocks based on premium size rather than ownership quality. High premium usually means high implied volatility, which usually means the market expects large moves. That's not free money. That's compensation for risk.

Here's my stock selection framework for cash-secured puts.

Would you buy and hold it? If you wouldn't own 100 shares of this stock at the strike price for three to six months, don't sell puts on it. Assignment is not a failure of the strategy. It's the strategy working as designed. You must be comfortable owning what you sell puts on.

Liquid options market. Look for bid-ask spreads under $0.10 on the strikes you're targeting. Wide spreads eat your premium through slippage. Minimum 500 open interest on your target strike.

Moderate implied volatility. IV Rank between 20 and 50 is the sweet spot. Below 20, premiums are usually too thin to justify the trade. Above 50, the market is pricing in a significant move, and you should understand why before selling into it.

Fundamentally sound business. Strong balance sheet, consistent revenue, and a business model you understand. This isn't the place for speculative names, meme stocks, or companies you'd need to Google before explaining what they do.

Selecting Your Strike and Expiration

Once you've chosen the right stock, strike and expiration selection determine your probability profile and income.

Strike selection by delta, not price. I've said it before and I'll say it again: select strikes by delta, not by looking at the strike price. For cash-secured puts, I target the 0.15 to 0.25 delta range. A 0.20 delta put gives you roughly an 80% probability of expiring worthless while still generating meaningful premium.

Expiration: the 30-45 DTE sweet spot. Options lose time value at an accelerating rate, with the steepest decay occurring in the final 30 days. Selling at 30-45 days to expiration captures the most efficient theta decay relative to the time you have capital committed. Going further out ties up capital longer for diminishing marginal premium. Going shorter gives you less time for the stock to move away from your strike.

Avoid earnings. Unless you have a specific strategy for trading through earnings, don't sell puts that expire during or immediately after an earnings announcement. The volatility crush after earnings can work in your favor, but the gap risk can also blow past your strike overnight. For standard income generation, simply check the earnings calendar and sell around it.

Strike selection by delta: 0.15 delta gives 85% probability of profit (conservative), 0.20 gives 80% (balanced default), 0.25 gives 75% (experienced sellers). Expiration sweet spot: 30-45 DTE for peak theta efficiency. Always check the earnings calendar.

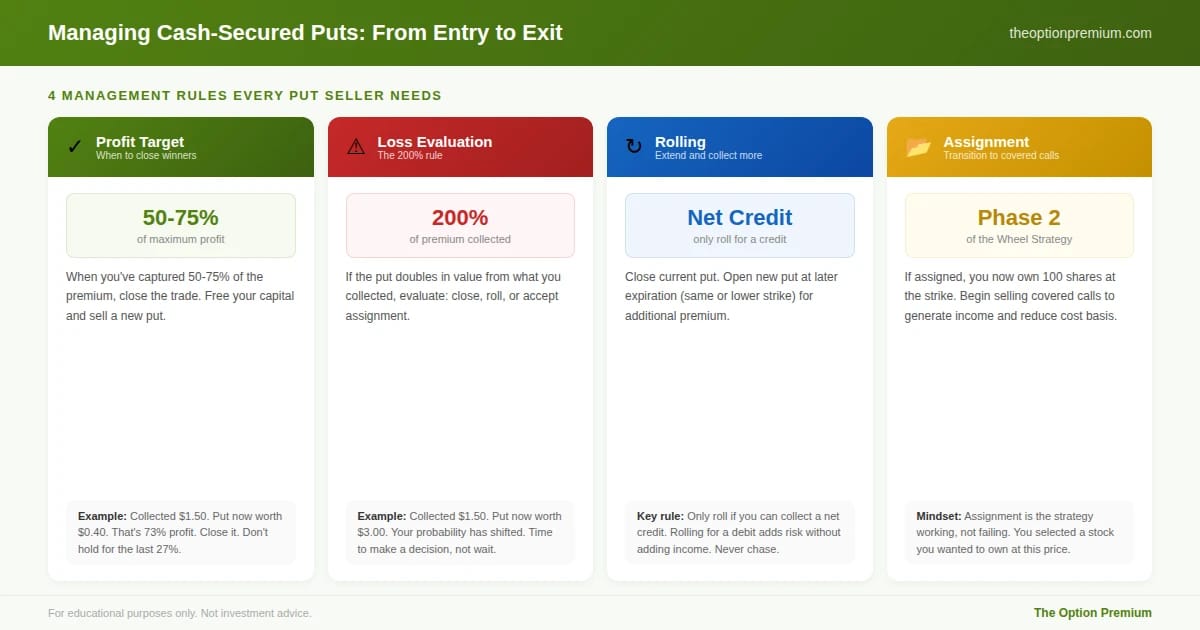

Managing the Trade: From Entry to Exit

The trade doesn't end when you sell the put. Management is what separates consistent sellers from those who get burned.

Profit target: close at 50-75% of max profit. If you collected $1.50 in premium and the put is now worth $0.40, you've captured over 73% of the maximum profit. Close the trade, free your capital, and sell a new put. Holding for the last 25% of profit ties up capital and exposes you to gamma risk near expiration.

Loss management: the 200% rule. If the put doubles in value from what you collected, meaning you collected $1.50 and it's now worth $3.00, evaluate the position. You can close for a loss, roll to a later expiration for additional credit, or accept assignment if you're comfortable owning the stock at your effective cost basis.

Rolling. When a put is moving against you, rolling means closing the current position and opening a new one at a later expiration, often at the same or lower strike, for a net credit. Rolling doesn't eliminate risk, but it gives the position more time and lowers your effective cost basis through the additional premium collected.

Assignment. If your put expires ITM and you're assigned, you now own 100 shares at the strike price. This is where the cash-secured put transitions into the second phase of the Wheel Strategy. You begin selling covered calls against your shares to continue generating income and reduce your cost basis further.

Four management rules for every cash-secured put: close winners at 50-75% of max profit to free capital, evaluate losers at 200% of premium collected, only roll for a net credit (never chase), and transition to covered calls when assigned as Phase 2 of the Wheel Strategy.

The Practitioner Edge: Position Sizing for Cash-Secured Puts

Position sizing is where most put sellers either build sustainable income or blow up their accounts.

Maximum 25% of account per position. No single cash-secured put should require more than 25% of your total account as collateral. For a $50,000 account, that means no single position requiring more than $12,500.

Account for simultaneous assignments. In a market selloff, multiple puts can be tested at once. You need enough capital to handle assignment on at least two positions simultaneously while maintaining your cash reserve. This means you can't deploy 100% of your account into active put positions.

Maintain a 20% cash reserve. Always keep at least 20% of your total account in cash, uninvested. This reserve handles unexpected assignments, allows you to roll positions when needed, and gives you capital to sell new puts when attractive opportunities appear during pullbacks.

Scale to your account. A $25,000 account might run two to three cash-secured puts. A $100,000 account might run five to seven. More isn't better. Better is better. The goal is consistent, manageable income, not maximum capital deployment.

Risk Reality Check

Cash-secured puts are not risk-free income. The risks are real, and you need to understand them before your first trade.

The stock can drop significantly. Your maximum loss on a cash-secured put is the strike price times 100 minus the premium collected. On a $50 stock, that's a theoretical $4,850 loss per contract (if the stock goes to zero). In practice, the risk is a meaningful decline, say 20-30%, that leaves you holding shares well below your cost basis.

Opportunity cost. The cash securing your put is locked up and unavailable. If a better opportunity appears while your capital is committed, you can't act on it without closing the existing position.

Assignment timing. American-style options can be exercised before expiration. Early assignment is rare for puts but not impossible, especially when the stock drops well below the strike near a dividend date.

Your primary defense against all three risks is the same: select quality stocks you want to own, size positions conservatively, maintain your cash reserve, and manage trades actively rather than passively waiting for expiration.

Key Takeaways

A cash-secured put means selling a put while holding enough cash to buy 100 shares if assigned. Think of it as getting paid to place a limit order on a stock you already want to own at a lower price.

The seller's edge comes from four advantages: earning income while waiting, always entering at a lower cost basis, probability on your side (0.20 delta gives ~80% chance of expiring worthless), and time decay working in your favor every day.

Stock selection matters more than any other variable. If you wouldn't hold 100 shares at the strike for three to six months, don't sell the put. High premium on a bad stock isn't income. It's risk compensation.

Target the 0.15-0.25 delta range for strike selection and 30-45 DTE for expiration. Close at 50-75% of max profit to free capital and avoid gamma risk. Evaluate at 200% of premium collected on the loss side.

Size conservatively: max 25% per position, plan for simultaneous assignments, maintain 20% cash reserve. Consistent income comes from sustainable sizing, not maximum deployment.

You don't need to predict where a stock is going to profit from cash-secured puts. You just need to know where you'd be happy to own it, and collect income while you wait.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply