- The Option Premium

- Posts

- The Capital Efficiency Hybrid: How LEAPS, Cash-Secured Puts, and Covered Calls Make Every Dollar Work

The Capital Efficiency Hybrid: How LEAPS, Cash-Secured Puts, and Covered Calls Make Every Dollar Work

LEAPS control stock at 30% of the cost, freeing 65-75% of capital to sell cash-secured puts. When assigned, covered calls generate income on shares. A $50,000 hybrid portfolio runs 10+ income streams where a traditional portfolio runs 3.

Andrew Crowder

April 11, 2026

The Capital Efficiency Hybrid: How LEAPS, Cash-Secured Puts, and Covered Calls Make Every Dollar Work

Most individual investors have a portfolio where half their capital is doing nothing. They own shares of good companies. Those shares sit in their accounts. They collect dividends, maybe, and they appreciate over time, hopefully. But the capital tied up in those shares is locked. It's not generating additional income. It's not producing premium. It's just sitting there, waiting for the stock to go up.

There is a better way. And once you see the math, it's difficult to go back.

The approach is a hybrid that combines three strategies most traders learn separately but rarely connect. LEAPS options to control stock exposure at a fraction of the capital cost. Cash-secured puts funded by the capital that LEAPS freed up. And covered calls on any shares you acquire through assignment. Each piece generates income or provides exposure. Together, they create a portfolio where every single dollar is working.

This isn't theory. It's the framework I use across multiple portfolios at The Option Premium, and it's the reason capital efficiency has become one of the most important concepts in how I think about building long-term wealth with options.

The Problem With Owning Stock Outright

Let me start with the math that most investors never think about.

You want exposure to 100 shares of a stock trading at $180. That costs $18,000. The money is deployed. It's working in the sense that you participate in the stock's upside (and downside). But from a premium-selling perspective, that $18,000 is locked. The only way to generate additional income on those shares is to sell covered calls against them.

That's fine. Covered calls are a solid strategy. But think about what's happening at the portfolio level. You have $18,000 producing one income stream (the covered call premium) and participating in one stock's price movement. The capital is concentrated, single-purpose, and immobile.

Now imagine you could get similar upside exposure to that same stock for $3,000 instead of $18,000. The remaining $15,000 would be free to generate income elsewhere. That's what LEAPS options make possible.

LEAPS: Controlling $18,000 of Exposure for a Fraction of the Cost

A LEAPS option (Long-Term Equity Anticipation Security) is simply a long-dated call option, typically with 12 to 24 months until expiration. When you buy a deep in-the-money LEAPS call, you're purchasing the right to buy 100 shares of the stock at the strike price, and because the option is deep in the money, it behaves very similarly to owning the shares themselves.

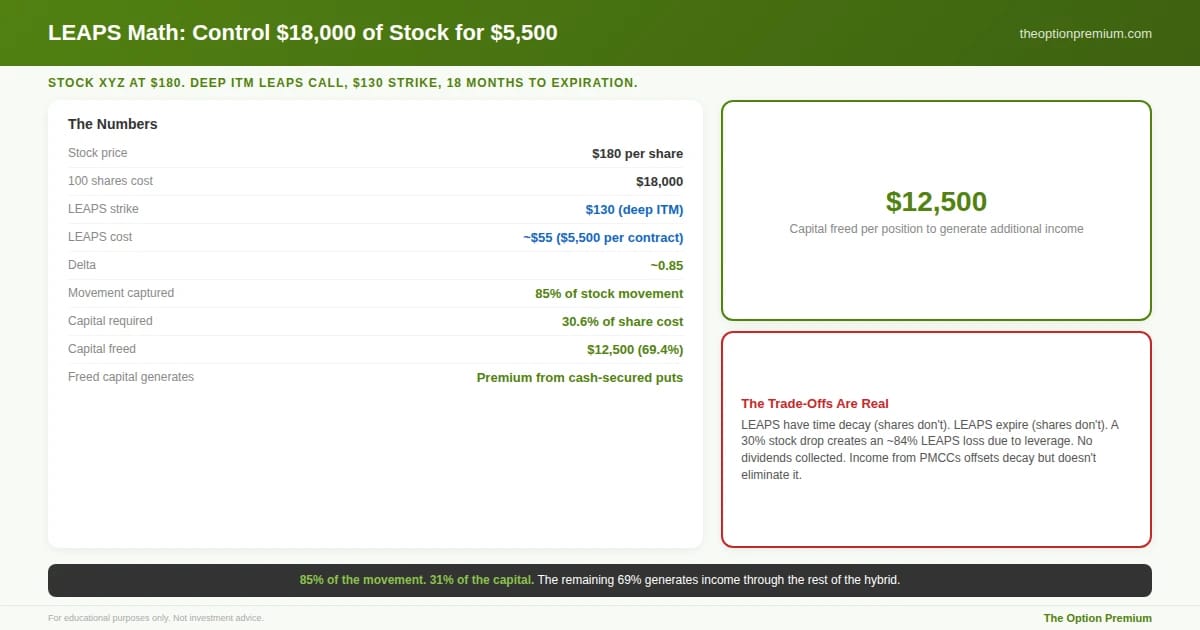

Here's a real-world example. Stock XYZ is trading at $180. You buy a LEAPS call with a strike price of $130, expiring in 18 months. The option costs approximately $55 per contract, or $5,500 for one contract controlling 100 shares.

That $5,500 gives you exposure to 100 shares worth $18,000. The LEAPS has a delta of roughly 0.85, meaning for every $1 the stock moves, your LEAPS moves approximately $0.85. You're capturing 85% of the stock's movement for 30% of the capital cost.

The trade-off is real and I want to be upfront about it. LEAPS have time decay, shares don't. LEAPS expire, shares don't. If the stock drops significantly, the LEAPS can lose value faster than shares would because of the leverage involved. And you don't collect dividends on a LEAPS position (though the option's pricing partially reflects expected dividends). These are genuine costs that must be weighed against the capital efficiency benefits.

But here's the part that changes the equation. You just freed up $12,500 ($18,000 minus $5,500). That capital isn't sitting idle anymore. It's available to generate income through the second piece of the hybrid.

The LEAPS math that makes the hybrid possible. Stock XYZ at $180: 100 shares cost $18,000. A deep ITM LEAPS call at the $130 strike with 18 months to expiration costs approximately $5,500 with a delta of 0.85, capturing 85% of the stock's movement for 30.6% of the capital cost. That frees $12,500 per position to generate income through cash-secured puts. The trade-offs are real and disclosed: LEAPS have time decay (shares don't), LEAPS expire (shares don't), a 30% stock decline creates approximately 84% LEAPS loss due to leverage, and no dividends are collected. Income from poor man's covered calls offsets decay but doesn't eliminate it.

Cash-Secured Puts: Putting the Freed Capital to Work

With $12,500 now available, you can sell cash-secured puts on stocks you'd be willing to own at lower prices. A cash-secured put means you sell a put option and keep enough cash in your account to buy the shares if you're assigned. You collect premium upfront, and one of two things happens: the stock stays above your strike and you keep the premium as profit, or the stock drops below your strike and you buy shares at an effective cost basis that's reduced by the premium you collected.

Either outcome is acceptable when you've selected the right underlying at the right implied volatility level.

With $12,500 in freed capital, you could sell cash-secured puts on several different underlyings. Maybe you sell a put on a $45 stock (securing $4,500), a put on a $35 stock (securing $3,500), and a put on a $40 stock (securing $4,000). That deploys $12,000 of the freed capital across three additional positions, each generating premium income.

Let's put real numbers on this. Selling a 30-45 DTE put at the 0.20 to 0.30 delta on a stock with elevated IV Percentile might generate 1.5% to 3% of the secured capital per cycle. On $12,000 deployed across three puts over a 30-45 day cycle, that's $180 to $360 in premium. Repeat that 8 to 10 times per year, and you're looking at $1,440 to $3,600 in annual income from capital that would have been locked inside stock shares doing nothing.

And the LEAPS position is still providing your stock exposure the entire time. The capital is working twice.

When Assignment Happens: Covered Calls Complete the Cycle

The third piece of the hybrid activates when one of your cash-secured puts results in assignment. The stock dropped below your strike, and now you own 100 shares at your chosen price, reduced by the premium you collected.

This is not a failure. This is the strategy working as designed. You selected a stock you wanted to own at a price you were comfortable paying. The premium you collected lowered your effective cost basis. And now you have shares.

What do you do with shares? You sell covered calls against them.

The covered call generates additional income on the assigned shares. You sell a call at a strike above your cost basis, collect premium, and one of two outcomes occurs: the stock stays below the call strike and you keep the premium plus the shares, or the stock rises above the call strike and your shares are called away at a profit (strike price minus your cost basis, plus the premium collected).

Either outcome is profitable. And notice what has happened at the portfolio level. The same capital that was originally going to buy 100 shares of one stock is now producing income from three sources simultaneously: the LEAPS provides upside exposure (and can have short calls sold against it as a poor man's covered call), the cash-secured puts generate premium on the freed capital, and the covered calls generate premium on any assigned shares.

Every dollar is working. That's the point.

Three income engines running on one capital base. Engine 1: LEAPS and poor man's covered calls provide upside exposure and short call income at 25-35% of the capital cost of owning shares. Engine 2: the freed capital (65-75% of what shares would have cost) sells cash-secured puts across 4-6 underlyings, generating 1.5-3% per cycle, 8-10 cycles per year. Engine 3: when put assignments occur, covered calls generate income on the acquired shares. When shares are called away at a profit, the capital recycles back to Engine 2. The cycle is self-reinforcing: LEAPS free capital, freed capital sells puts, assignments create covered calls, called-away shares return capital to the put-selling cycle.

The Full Hybrid in Practice: One Portfolio, Three Income Engines

Let me walk through how this looks with a $50,000 account.

Traditional approach. You buy 100 shares of Stock A at $180 ($18,000), 100 shares of Stock B at $160 ($16,000), and 100 shares of Stock C at $150 ($15,000). Total deployed: $49,000. Cash remaining: $1,000. Income options: covered calls on three positions. That's it.

The hybrid approach. You buy a deep ITM LEAPS on Stock A for $5,500 (controls 100 shares worth $18,000). You buy a deep ITM LEAPS on Stock B for $4,800 (controls 100 shares worth $16,000). You buy a deep ITM LEAPS on Stock C for $4,500 (controls 100 shares worth $15,000). Total deployed in LEAPS: $14,800. Capital freed: $34,200.

Now you sell poor man's covered calls against each LEAPS position, generating premium just like traditional covered calls. And you deploy a significant portion of the freed $34,200 into cash-secured puts across 4 to 6 additional underlyings, generating premium every 30-45 days on capital that would have been locked in stock.

The income streams multiply. The LEAPS provide the upside exposure. The poor man's covered calls generate income on that exposure. The cash-secured puts generate income on the freed capital. And any assignments convert into covered call positions that generate yet another income stream.

The $50,000 account now has exposure to 3 stocks through LEAPS, income from 3 sets of short calls against those LEAPS, income from 4-6 cash-secured put positions, and the potential for covered call income on any assigned shares. Compared to the traditional approach (3 stock positions, 3 covered call income streams), the hybrid is running 10 or more simultaneous income-generating positions from the same capital base. The diversification benefit alone is significant, as the traditional approach concentrates the entire account into three names.

Same $50,000. Fundamentally different capital deployment. The traditional approach locks $49,000 in 3 stock positions with $1,000 remaining, generating 3 covered call income streams. The hybrid deploys $14,800 in LEAPS (controlling the same stock exposure), frees $34,200 for cash-secured puts across 4-6 additional underlyings, and runs 10+ simultaneous income streams. The diversification improves from 3 names to 7-9 across multiple strategies, with a 20-30% cash reserve maintained at all times. The difference is entirely attributable to capital efficiency.

The Compounding Effect Over Time

The real power of this framework isn't any single month. It's what happens over 12, 24, and 36 months as the income compounds and the capital recycling continues.

Consider the cash-secured put cycle. Every 30-45 days, you collect premium on 4-6 positions. Over a year, that's 8-10 cycles. The premium income accumulates. Some of that income can be used to fund additional LEAPS positions, creating more exposure and more freed capital. Some can be held as a cash reserve (I always keep 20-30% uninvested). Some can be deployed into additional cash-secured puts, increasing the income further.

Meanwhile, when assignments occur, the shares generate covered call income for as long as you hold them. If the shares are called away at a profit, the capital recycles back into cash-secured puts. The cycle is self-reinforcing. Premium funds new positions, new positions generate premium, and capital continuously recycles through the three strategies.

Over two or three years, an investor running this hybrid framework will have generated meaningfully more income than an investor holding the same stocks outright and only selling covered calls. The difference is entirely attributable to capital efficiency, to the fact that LEAPS freed up capital that would otherwise have been locked and idle.

The Risks Are Real (And Must Be Managed)

I would be doing you a disservice if I presented this framework without a clear-eyed discussion of the risks.

LEAPS time decay. Your LEAPS options lose a small amount of time value every day. Over 18 months, the extrinsic value in a deep ITM LEAPS will decay to zero. If the stock is flat for the entire holding period, you'll lose the extrinsic value component of what you paid. The income from poor man's covered calls is designed to offset this decay, but it's not guaranteed to fully cover it.

Downside leverage. If the stock drops 30%, your LEAPS will lose more than 30% of its value because of the leverage embedded in the position. The LEAPS cost $5,500 to control $18,000 of exposure. A 30% stock decline ($54 per share) would reduce your LEAPS value by approximately $46 (0.85 delta times $54). That's a 84% loss on a $5,500 position. Shares would show a 30% loss. The LEAPS shows a much deeper percentage loss. This leverage cuts both ways.

Assignment risk on cash-secured puts. When the stock drops below your put strike, you're buying shares at a price that may be above the current market. The premium collected reduces your cost basis, but if the stock continues to fall, you're holding an underwater position. The covered calls you sell afterward generate income, but they also cap your upside if the stock recovers sharply.

Concentration and correlation. Running 10 or more positions simultaneously requires monitoring the overall portfolio's correlation exposure. If you're selling cash-secured puts on five different tech stocks, a sector-wide selloff can trigger multiple assignments simultaneously, concentrating your capital into a single sector at exactly the wrong time.

The management requirement. This is not a set-and-forget portfolio. LEAPS need to be rolled before they lose too much time value (typically when they have 4-6 months remaining). Cash-secured puts need monthly attention for new entries and management. Covered calls need rolling and replacement. The income is real. So is the work.

Position sizing remains the cornerstone. No single LEAPS position should represent more than 10-15% of the portfolio. No single cash-secured put should risk more than 5% of total capital. And the aggregate exposure across all positions should leave 20-30% of the account in cash as a buffer against correlated moves and unexpected assignments.

Capital efficiency without risk management is leveraged gambling. Five rules that make the hybrid sustainable. No single LEAPS exceeds 10-15% of portfolio value. No single cash-secured put risks more than 5% of total capital. 20-30% of the account stays uninvested as a buffer for unexpected assignments and correlated selloffs. LEAPS are rolled to new 18-24 month expirations when they reach 4-6 months remaining. And sector exposure is monitored to prevent multiple assignments from concentrating capital into one area during a downturn. The hybrid amplifies returns. Without these sizing rules, it also amplifies losses.

Key Takeaways

LEAPS options allow you to control stock exposure at 25-35% of the capital cost of buying shares outright. A deep ITM LEAPS with 0.80-0.85 delta captures 80-85% of the stock's movement while freeing 65-75% of the capital that would otherwise be locked in shares. The trade-off is time decay and downside leverage, both of which are real costs that must be managed.

The freed capital runs cash-secured puts on additional underlyings, generating premium income every 30-45 days on capital that would have been completely idle in a traditional stock portfolio. At 1.5-3% per cycle across 8-10 cycles per year, this income stream materially increases the portfolio's total return.

When cash-secured put assignments occur, covered calls complete the cycle by generating income on the acquired shares. The capital continuously recycles: LEAPS provide exposure, freed capital generates premium through puts, assignments create covered call opportunities, and called-away shares return capital to the put-selling cycle.

The compounding effect over time is the real power. A $50,000 hybrid portfolio can run 10 or more simultaneous income-generating positions compared to 3 covered call positions in a traditional stock portfolio. The diversification and income multiplication are both direct results of capital efficiency.

The risks require active management. LEAPS decay, downside leverage amplifies losses on percentage terms, assignments can concentrate capital during selloffs, and the framework demands consistent attention. Position sizing (10-15% max per LEAPS, 5% max per put, 20-30% cash reserve) is the structural protection that makes the hybrid sustainable through volatile periods.

The hybrid framework doesn't ask you to choose between owning stocks and selling premium. It does both simultaneously, using LEAPS to compress the capital requirement of stock exposure so that the freed capital can generate income through premium selling. The result is a portfolio where every dollar serves a purpose: growth, income, or reserve. Nothing sits idle. Nothing is wasted.

That's capital efficiency. And once you build a portfolio around it, you understand why professionals treat idle capital as one of the most expensive mistakes an investor can make.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply