- The Option Premium

- Posts

- How to Build an Options Portfolio That Can Take a Hit

How to Build an Options Portfolio That Can Take a Hit

Five pillars that keep premium sellers in the game: position sizing at 2-5%, uncorrelated positions across 8-12 underlyings, a permanent 20-30% cash reserve, strategy diversification, and a written drawdown plan with pre-committed actions at every level.

Andrew Crowder

April 11, 2026

How to Build an Options Portfolio That Can Take a Hit

Every premium seller eventually faces the same week. The market drops 4% on Monday. Two of your credit spreads are breaching their short strikes. An earnings play gaps through your call side overnight. Your account is down 8% in three days and the VIX is still climbing. You haven't made a mistake on any individual trade. Each position was properly sized, well-constructed, and entered at elevated IV. But the portfolio, taken as a whole, is telling you something that no single trade could: your positions were more connected than you thought.

This is the week that separates portfolios that survive from portfolios that don't. And the difference is almost never about the individual trades. It's about how the portfolio was built before the week started.

Over 24 years of professional options trading, I've learned that the traders who compound over decades are not the ones with the best entries. They're the ones who built a portfolio structure that could absorb a bad week, a bad month, or even a bad quarter without forcing them out of the game. The math of recovery is brutal. A 20% drawdown requires a 25% gain to break even. A 30% drawdown requires 43%. A 50% drawdown requires 100%. The single most important job you have as a premium seller is making sure you never reach the drawdown level where the recovery math becomes a prison sentence.

This article is the framework for building that portfolio.

The First Rule: No Single Trade Can Matter Too Much

This sounds obvious. It is obvious. And yet position sizing remains the number one reason premium sellers blow up.

The failure mode is always the same. A trader finds a high-conviction setup. The IV Percentile is above 80. The expected move is wide. The stock has been on a watchlist for weeks. Everything lines up perfectly, and the trader decides this trade deserves a bigger allocation. Instead of 3% of the account, they put on 8%. Or 12%. Or, in the worst cases I've seen, 20%.

The trade loses. It was always going to lose sometimes. An 80% probability of profit means 20% of the time the trade goes against you. That's not a malfunction. That's the math working exactly as expected. But at 3% risk, the loss is a bruise. At 12%, it's a broken bone. At 20%, it can be career-ending.

My rule: no single position should ever risk more than 2 to 5 percent of total account equity. On a $100,000 account, that's $2,000 to $5,000 of maximum loss per trade. This isn't a guideline. It's structural. It's the difference between a losing streak that dents your account and a losing streak that destroys it.

The Law of Large Numbers only works if you survive long enough to accumulate large numbers. Position sizing is what keeps you at the table.

The Correlation Problem: Why "Diversified" Portfolios Aren't

Here's where most premium sellers fail even when their position sizing is correct.

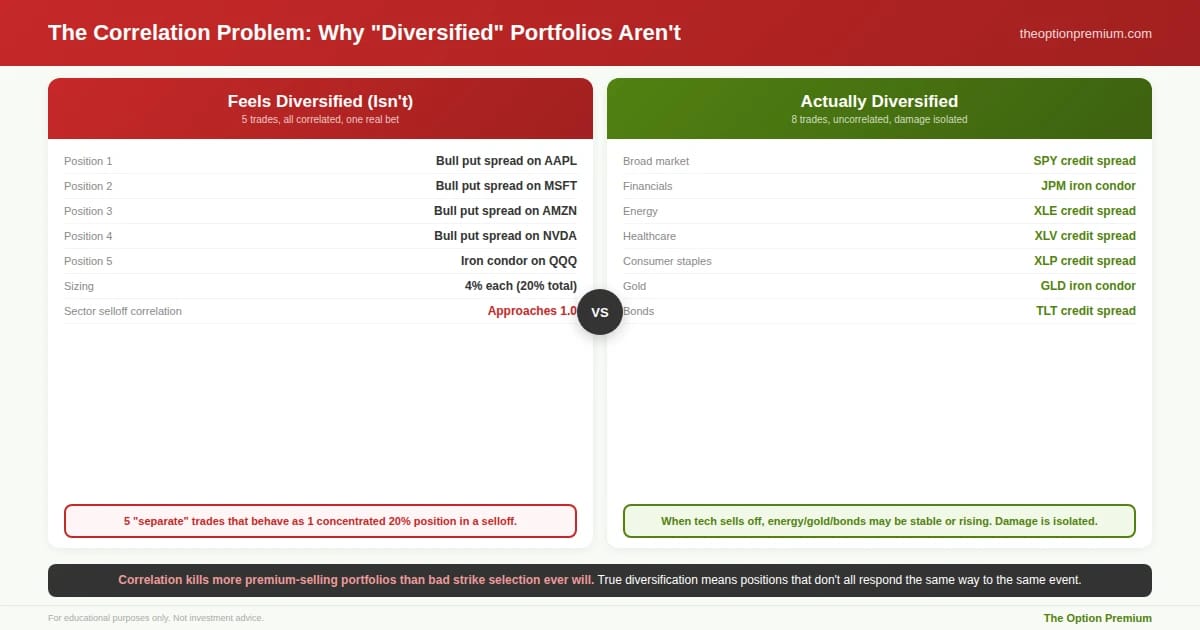

You sell a bull put spread on AAPL. A bull put spread on MSFT. A bull put spread on AMZN. A bull put spread on NVDA. And an iron condor on QQQ. Each position is 4% of your account. You're running five trades at conservative sizing. You feel diversified.

You're not.

Every single one of those positions is a bet that large-cap technology stocks don't fall significantly. When a sector-wide selloff hits (tariff escalation, regulatory news, a single mega-cap earnings miss that drags sympathy selling across the group), all five positions lose simultaneously. Your "diversified" portfolio of five trades behaves like one concentrated position at 20% of your account. The correlation between those underlyings during a selloff approaches 1.0. They move together. They lose together. Your five separate 4% risks become one 20% risk.

This is the correlation problem, and it kills more premium-selling portfolios than bad strike selection ever will.

True diversification in an options portfolio means spreading your positions across genuinely uncorrelated underlyings. Not five tech stocks. Not three semiconductor names and two cloud companies. Genuinely different sectors, asset classes, and risk profiles.

A portfolio that can take a hit might include SPY or SPX for broad market exposure. A financial name (JPM, GS) for rate sensitivity and banking sector exposure. An energy name (XOM, CVX) or energy ETF (XLE) for commodity-driven volatility. A healthcare name (UNH, JNJ) or healthcare ETF (XLV) for defensive, low-correlation exposure. A consumer staples name (PG, KO) or ETF (XLP) for non-cyclical stability. GLD for gold exposure, which historically moves inversely to equities during stress. TLT for long-duration bond exposure, providing a potential hedge during equity selloffs. And IWM for small-cap exposure that captures a different risk profile than large-cap technology.

The specific names matter less than the principle: when one sector is getting hit, you want other positions in your portfolio that are either stable or moving in your favor. Perfect negative correlation is rare and unnecessary. What you need is low correlation, meaning your positions don't all respond the same way to the same event.

The correlation problem in action. Five credit spreads on AAPL, MSFT, AMZN, NVDA, and QQQ at 4% each feels like diversification. It isn't. During a tech selloff, correlation approaches 1.0 and all five lose simultaneously, behaving as one concentrated 20% position. True diversification spreads across genuinely uncorrelated sectors: broad market, financials, energy, healthcare, consumer staples, gold, bonds. When tech sells off, energy and gold may be stable or rising. Damage is isolated, not compounded. Correlation kills more premium-selling portfolios than bad strike selection ever will.

How Many Positions Is Enough (and How Many Is Too Many)

Research on portfolio diversification, both in equities and in options-based portfolios, consistently shows that diversification benefits increase rapidly from 1 to 8 positions and then flatten significantly beyond 12 to 15. Adding the 20th uncorrelated position provides far less marginal risk reduction than adding the 6th.

For a premium-selling portfolio, I target 8 to 15 simultaneous positions across uncorrelated underlyings. Fewer than 8 leaves too much concentration risk. More than 15 creates management complexity without meaningful additional diversification, and the monitoring burden can lead to sloppy management decisions, which is where real risk lives.

The sweet spot for most individual traders running accounts between $25,000 and $250,000 is 8 to 12 positions. That provides enough diversification to absorb a sector-specific hit while remaining manageable for a trader who is also living a life outside of the markets.

Each position is sized at 2 to 5 percent maximum loss. With 10 positions at an average of 3% risk each, the total portfolio risk if every single position hit max loss simultaneously would be 30%. That's a severe scenario, but it's survivable. A 30% drawdown requires a 43% recovery. Difficult, but achievable over 12 to 18 months with disciplined premium selling. Compare that to a portfolio with 5 correlated positions at 8% risk each: the same total risk on paper (40%), but the correlation means they're far more likely to all lose together. The concentrated portfolio's worst case isn't theoretical. It's probable during a correlated selloff.

The Cash Reserve: Your Most Important Position

I keep 20 to 30 percent of my account in cash at all times. Not deployed. Not committed to any position. Sitting idle, on purpose.

This sounds like wasted capital, and to new traders, it feels like leaving money on the table. But the cash reserve serves three critical functions that make it the most important "position" in the portfolio.

First, it absorbs unexpected assignments. When cash-secured puts get assigned during a selloff, you need capital to accept those shares without liquidating other positions at unfavorable prices. The cash reserve prevents forced selling.

Second, it provides opportunity capital during VIX spikes. The best premium-selling opportunities in any given year occur during the 3 to 5 days of peak fear, when implied volatility is highest and the credits available on credit spreads are richest. If your account is fully deployed when the spike happens, you can't take advantage of it. The cash reserve is the capital that lets you sell premium into fear while everyone else is frozen or getting margin-called.

Third, it provides psychological stability. When your account is down 10% and you know you have 25% in cash, the emotional pressure is fundamentally different than when your account is down 10% and every dollar is committed. The cash reserve gives you the mental space to make rational decisions rather than emotional ones. And rational decisions during drawdowns are what separate the traders who recover from the traders who spiral.

Strategy Diversification: Not Just Underlyings, but Approaches

A portfolio that can take a hit diversifies across strategies, not just underlyings. Different options strategies respond differently to the same market moves.

Credit spreads (bull put spreads and bear call spreads) are directional bets with theta tailwinds. They profit from time decay and from the stock not moving too far in one direction. Iron condors are range-bound plays that profit from the stock staying within a defined zone. They make money in sideways, low-movement markets. Cash-secured puts are bullish positions that generate income while waiting to acquire shares at lower prices. Covered calls and poor man's covered calls generate income on existing stock or LEAPS positions while capping upside.

A portfolio that runs only credit spreads has one risk profile. A portfolio that mixes credit spreads, iron condors across different underlyings, cash-secured puts on stocks you'd be comfortable owning, and covered calls on shares you already hold has multiple risk profiles operating simultaneously. When a directional move hurts your credit spreads, your iron condors on uncorrelated names may be untouched. When a volatile market whipsaws your iron condors, your cash-secured puts may be generating premium on the elevated IV.

The goal isn't to eliminate losses. You can't eliminate losses in a probability-based strategy. The goal is to ensure that losses in one part of the portfolio are offset (or at least not compounded) by the rest of the portfolio. This is what "taking a hit" looks like in practice: one area of the portfolio absorbs a loss while the other areas continue generating income and providing stability.

The Drawdown Plan: What You'll Do Before You Need to Do It

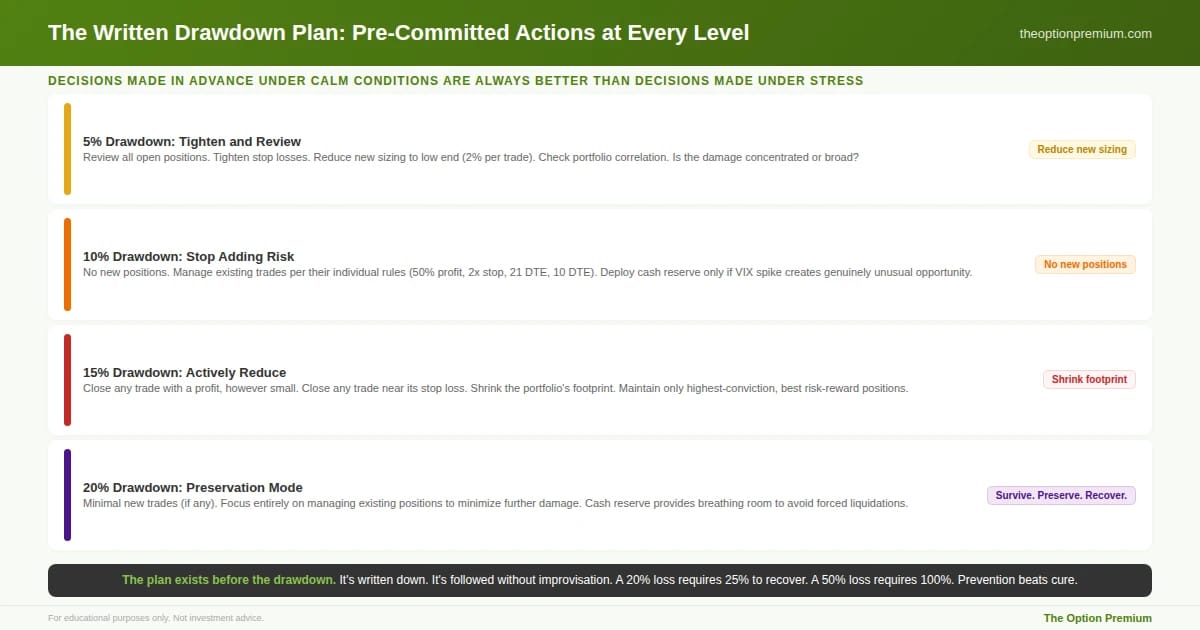

Every portfolio needs a written drawdown plan. Not a mental note. Not a vague intention. A written, specific, pre-committed plan for what happens when the account drops 5%, 10%, 15%, and 20%.

Here's mine.

At a 5% drawdown, I review all open positions, tighten any stop losses that haven't been triggered, and reduce new position sizing from my standard range to the low end (2% per trade instead of 3-4%). I also check portfolio-level correlation to see if the drawdown is concentrated or broad.

At a 10% drawdown, I stop opening new positions entirely. I manage existing positions according to their individual rules (50% profit target, 2-2.5x stop, 21 DTE review, 10 DTE exit) but I don't add risk. I deploy the cash reserve only if IV has spiked to levels where the premium available on conservative, wide credit spreads represents a genuinely unusual opportunity.

At a 15% drawdown, I begin actively reducing positions. I close any trade that has a profit, no matter how small, to free capital and reduce exposure. I close any trade that is near its stop loss. The goal at this level is to shrink the portfolio's footprint while maintaining only the highest-conviction positions with the most favorable risk-reward.

At a 20% drawdown, the portfolio is in preservation mode. Minimal new trades (if any). Focus entirely on managing existing positions to minimize further damage. This is where the cash reserve proves its value: it provides the breathing room to avoid forced liquidations and the psychological stability to think clearly.

The specific numbers can be adjusted based on your risk tolerance. The principle is non-negotiable: the plan exists before the drawdown, it's written down, and it's followed without improvisation. Decisions made in advance under calm conditions are always superior to decisions made in real time under the stress of watching your account decline.

The written drawdown plan with specific pre-committed actions at every level. At -5%: review all positions, tighten stops, reduce new sizing to 2% per trade, check portfolio correlation. At -10%: stop opening new positions entirely, manage existing trades per their rules, deploy cash reserve only for genuinely unusual VIX-spike opportunities. At -15%: actively reduce by closing any trade with a profit (however small) and any trade near its stop, shrink the portfolio footprint. At -20%: preservation mode, minimal new trades, focus on managing existing positions to prevent further damage. The plan exists before the drawdown. It's written down. It's followed without improvisation.

The Math of Recovery: Why Prevention Beats Cure

The reason this entire framework matters comes down to a simple asymmetry that governs all of investing.

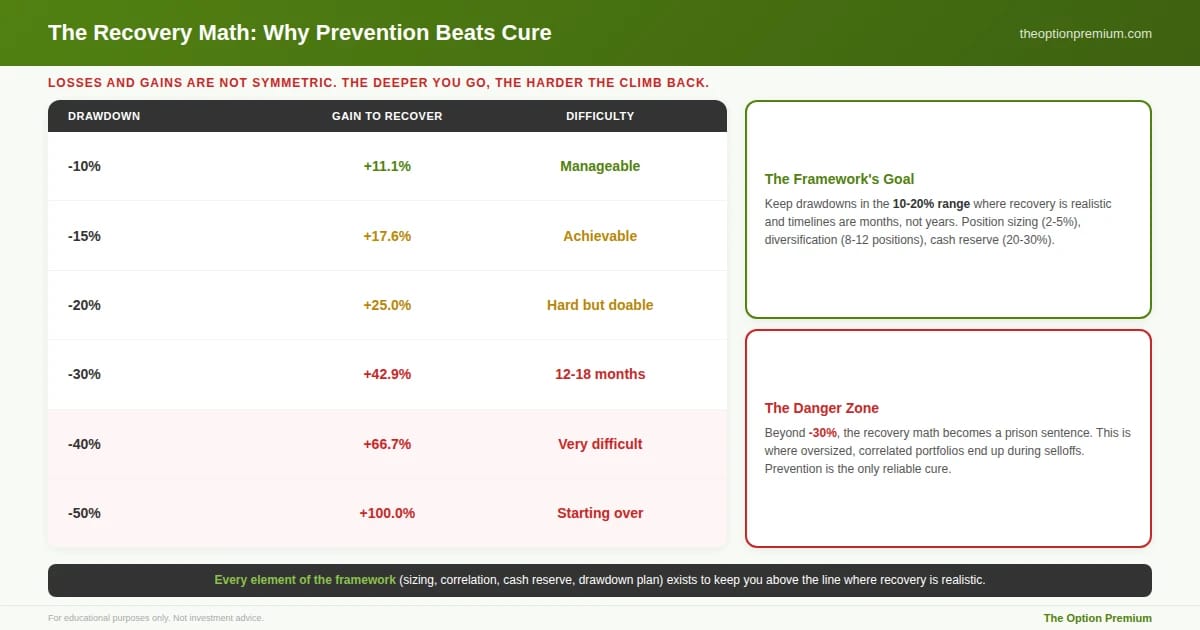

Losses and gains are not symmetric. A 10% loss requires an 11% gain to recover. That's manageable. A 20% loss requires a 25% gain. Harder, but achievable within a year. A 30% loss requires a 43% gain. Now you're talking about 12 to 18 months of disciplined trading to get back to even. A 50% loss requires a 100% gain. At that point, you're effectively starting over.

Every element of this framework, position sizing at 2-5%, uncorrelated underlyings, 8-12 positions, cash reserve of 20-30%, strategy diversification, and a written drawdown plan, exists to keep drawdowns in the 10-20% range where recovery is realistic. The goal is never to avoid losses entirely. That's impossible in a probability-based approach. The goal is to keep losses at a level where the recovery math is on your side and the timeline for recovery is measured in months, not years.

The asymmetry that governs all of investing. A 10% loss requires an 11.1% gain to break even. Manageable. A 20% loss requires 25%. Harder, but achievable. A 30% loss requires 42.9%. Now you're talking 12-18 months of disciplined trading just to get back to even. A 50% loss requires 100%. You're starting over. Every element of the framework (2-5% sizing, 8-12 uncorrelated positions, 20-30% cash reserve, written drawdown plan) exists to keep drawdowns in the 10-20% range where recovery is realistic and timelines are months, not years. Beyond -30%, the math becomes a prison sentence. Prevention beats cure.

Risk Reality Check

Even a perfectly constructed portfolio can experience drawdowns that exceed your plan. Correlated selloffs can be deeper and longer than historical patterns suggest. Black swan events can gap markets through levels that render stop losses ineffective. The 2020 COVID crash, the 2008 financial crisis, and the 2022 inflation selloff all tested even the most disciplined portfolios.

The framework described here reduces the probability and severity of catastrophic drawdowns. It does not eliminate them. The cash reserve, the position sizing, the correlation management, all of it is designed to keep you in the game through the worst periods so that the Law of Large Numbers can reassert itself over the hundreds of trades that follow. But there will be periods where the portfolio takes a hit that no framework could have fully prevented. The measure of the framework isn't whether it prevents all pain. It's whether it prevents the kind of pain from which you can't recover.

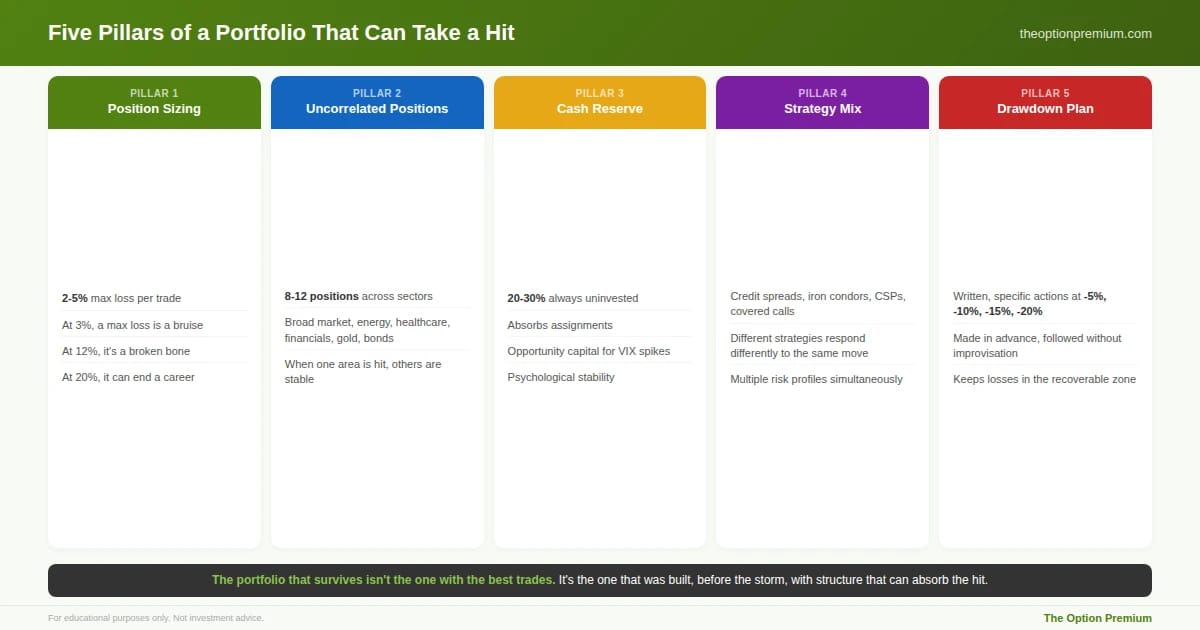

The five structural pillars that determine whether a portfolio survives a bad week, a bad month, or a bad quarter. Position sizing (2-5%) keeps any single loss at bruise level. Uncorrelated positions (8-12 across sectors) ensure a sector-specific selloff damages one area while others remain stable. Cash reserve (20-30%) absorbs assignments, provides VIX-spike opportunity capital, and delivers psychological stability. Strategy diversification means credit spreads, iron condors, cash-secured puts, and covered calls each respond differently to the same market move. And a written drawdown plan with specific actions at -5%, -10%, -15%, and -20% ensures decisions are made in calm, not in crisis.

Key Takeaways

No single trade should ever risk more than 2 to 5 percent of account equity. Position sizing is the structural foundation that makes everything else possible. The Law of Large Numbers only works if you survive long enough to accumulate large numbers. At 3% risk per trade, a max loss is a bruise. At 12%, it's a broken bone. At 20%, it can end a career.

Correlation is the hidden risk that kills "diversified" portfolios. Five credit spreads on five tech stocks is one concentrated bet, not five separate trades. True diversification means spreading positions across genuinely uncorrelated sectors and asset classes (broad market, financials, energy, healthcare, commodities, bonds) so that a sector-specific selloff damages part of the portfolio while the rest remains stable or benefits.

Target 8 to 12 simultaneous positions with a permanent 20-30% cash reserve. Diversification benefits plateau beyond 12-15 positions. The cash reserve absorbs unexpected assignments, provides capital to sell premium during VIX spikes when opportunities are richest, and delivers the psychological stability needed to make rational decisions during drawdowns.

Diversify across strategies, not just underlyings. Credit spreads, iron condors, cash-secured puts, and covered calls each respond differently to the same market conditions. When directional moves hurt credit spreads, iron condors on uncorrelated names may be untouched. When volatility whipsaws condors, cash-secured puts may be thriving on elevated IV. Multiple risk profiles operating simultaneously reduce the chance of portfolio-wide damage.

Write a drawdown plan before you need it. Specific, pre-committed actions at 5%, 10%, 15%, and 20% drawdown levels. Decisions made in advance under calm conditions are always better than decisions made under the stress of a declining account. The plan keeps drawdowns in the 10-20% range where recovery math is on your side and timelines are measured in months, not years.

The portfolio that survives a bad week, a bad month, or a bad quarter isn't the one with the best individual trades. It's the one that was built, before the storm arrived, with position sizing that prevents catastrophe, diversification that isolates damage, cash reserves that provide stability and opportunity, and a management plan that was written in calm and executed under pressure. That's what it means to build a portfolio that can take a hit.

Andy Crowder

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply