- The Option Premium

- Posts

- Apple PMCC Trade Setup: Building the Position Today

Apple PMCC Trade Setup: Building the Position Today

Full AAPL Poor Man's Covered Call setup with real option chain data. Jan 2028 $210 LEAPS at $78.50 + May $275 short call at $3.45. Capital math, income projections, and earnings management plan.

Andrew Crowder

April 09, 2026

Apple PMCC Trade Setup: Building the Position Today

After writing about how to choose LEAPS contracts and how the income math works in theory, I want to start doing something more direct: showing exactly how I would build a position right now, with real current data, in real market conditions.

This week it's Apple. And the setup is cleaner than it's been in a while.

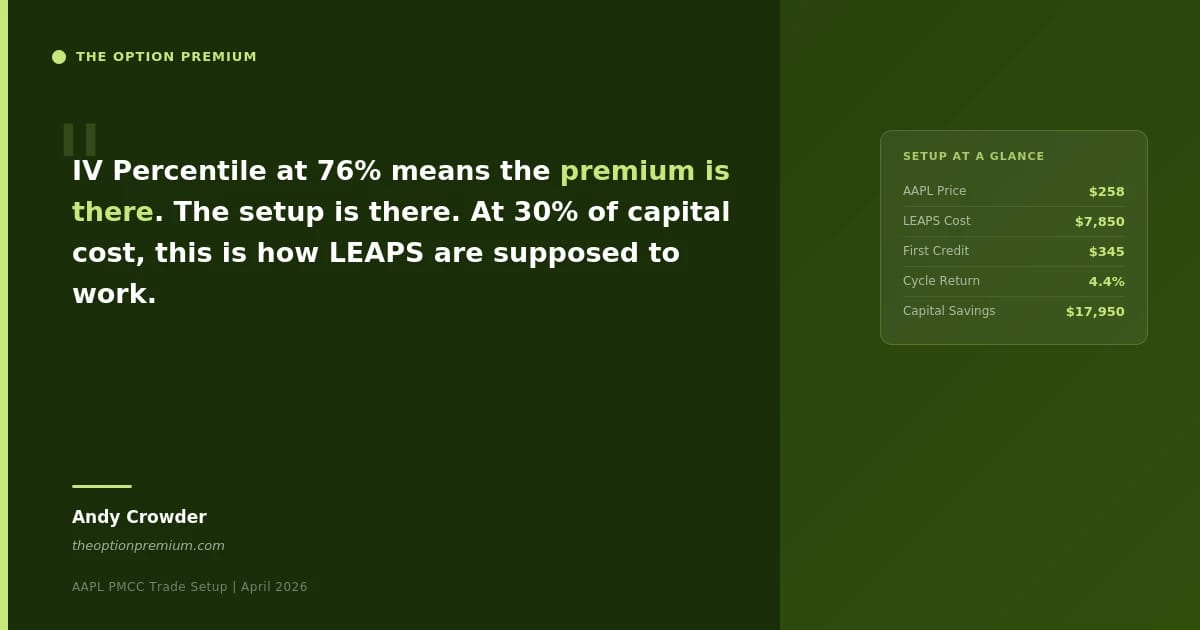

The LEAPS replaces $25,800 in share capital with $7,850, freeing $17,950 for other positions while maintaining 0.78 delta exposure.

Why Apple Right Now

Apple is trading near $258. IV Percentile sits at 76%, which means short call premium is above-average relative to the past year. IV Rank is 24.51% with an IV of 29.06% against a historic volatility of 24.33%. That spread tells you the market is pricing in a modest premium above recent realized moves, enough to make selling worth doing, without screaming that something is broken.

There is one thing to flag immediately: earnings are on 05/07/26. The first short call cycle I'm going to walk through spans that date. I'll tell you how I think about that in a moment.

The LEAPS Leg

The long position here is the January 2028 $210 call.

That's 655 days out, or roughly 22 months of duration. At a cost of $78.50 per share ($7,850 per contract at the mid), here's the value breakdown:

Intrinsic value: $258 minus $210 = $48.00 (61% of what you're paying)

Extrinsic value: $78.50 minus $48.00 = $30.50 for 22 months of time and volatility exposure

Delta: 0.78, the position moves roughly $78 for every $100 move in Apple

For comparison, buying 100 shares outright costs $25,800. You're putting up $7,850, 30% of that capital, for 78% of the price sensitivity. The $17,950 freed up can run two or three other positions simultaneously.

The break-even at LEAPS expiration (before any short call credits) is $210 plus $78.50 = $288.50. That's the number the short call program needs to chip away at over the next 22 months.

Both legs of the PMCC structure with current option chain data. The earnings date on 05/07/26 is the primary management consideration in cycle one.

The First Short Call

The May 15 $275 call is the first short call I'd sell against this LEAPS.

Here's what the chain shows: delta 0.26, Probability OTM 76.43%, bid/ask $3.40/$3.50. At a mid of $3.45, that's $345 collected immediately against the $7,850 LEAPS position.

The $275 strike puts the short call 6.6% above the current stock price. That distance is intentional. At 39 days to expiration, you want enough room that normal market oscillation doesn't immediately threaten the short call. A delta of 0.26 means the market is pricing roughly a 1 in 4 chance this call ends up in-the-money, you're getting paid to take the other side of that.

Return on LEAPS capital for this cycle: $345 / $7,850 = 4.4% in 39 days.

Now, the earnings situation. Apple reports on 05/07/26, which falls inside this cycle. That's not a reason to avoid the trade, it's a reason to have a plan. My preference is to manage the short call before the earnings announcement rather than hold through an unknown binary event uncapped. I'll close or roll the $275 short call in the days leading up to 05/07. If I collect $2.50 to close it, the net is still $0.95 on this cycle. Not a full $3.45, but still positive and the LEAPS stays clean.

The alternative is to use a wider strike from the start, the $280 or $285 call instead of $275, to build in more cushion. The premium is thinner, but so is the risk around earnings.

The Income Math Over 7 Cycles

This isn't about one $345 credit. The structure works because you repeat it.

Seven cycles through November collect a projected $2,285 in premium, reducing the LEAPS cost basis from $7,850 to roughly $5,565 before any Apple price appreciation.

The projections in the table above are illustrative. Real results will vary. Strike levels will shift as the stock moves, and some cycles will be managed early. But the direction of the math is what matters: at roughly 4% per cycle, the LEAPS cost erodes meaningfully over a year. By November, 29% of the original cost basis has been recovered through premium alone.

That cost reduction is not hypothetical. It's the accumulated credits from selling optionality the market is pricing at levels higher than the underlying volatility historically justifies. That spread between implied and realized volatility is what funds the income side of this structure.

The Practitioner Edge

There are two things retail traders consistently miss with the PMCC.

First, they sell the wrong short call. There's a temptation to sell a closer strike for more premium. Selling delta 0.40 instead of 0.26 collects more upfront, but it also caps the LEAPS upside aggressively and creates management headaches. The 0.25-0.30 delta zone is where the probability math and the income math line up for this structure.

Second, they ignore earnings. I have seen retail traders hold short calls through earnings with no plan and end up with an assignment they weren't prepared for. That is not a LEAPS problem, it's a position management problem. Know when earnings are before you put the trade on, not after.

The IV environment right now, 76th percentile, means you're selling above the median. That's worth doing. But elevated IV also means the market is pricing in some uncertainty about the near-term path. Stay nimble with the short call.

All three scenarios for the May expiration. In every case, the PMCC structure outperforms owning 100 shares outright on a capital-efficiency basis.

Risk Reality Check

The LEAPS is not riskless. Apple has dropped more than 25% over the past year from its highs, and the LEAPS participates in that on the downside, at 0.78 delta, it participates quite closely. What the structure does is limit the absolute dollar loss versus full share ownership while the premium income provides a real cushion.

The maximum loss here is the $7,850 paid for the LEAPS, less any premium collected. That's meaningful but it's less than a third of the loss on 100 shares if Apple went to zero. More realistically, if Apple drops 20% to $206, the $48 intrinsic value goes to zero and the position is underwater. The premium collected to that point has cushioned some of it. The key question is whether your thesis on Apple supports holding through a decline, if it does, the premium keeps accumulating. If it doesn't, the position sizes should have been smaller.

Key Takeaways

LEAPS: Jan 2028 $210 call at $78.50 ($7,850 per contract). Delta 0.78. Intrinsic 61%.

First short call: May 15 $275 at $3.45 ($345 credit). 39 DTE. Prob. OTM 76.43%.

Cycle return: 4.4% on LEAPS capital in 39 days.

Capital saved: $17,950 vs. buying 100 shares.

Earnings on 05/07/26: Manage the short call before the event. Have a plan before entry.

7-cycle projection: $2,285 collected, basis reduced to $5,565 by November.

IV context: Percentile at 76%, premium is above average. Good time to be a seller.

IV Percentile at 76% means the premium is there. The setup is there. At 30% of capital cost, this is how LEAPS are supposed to work.

Trade Smart. Trade Thoughtfully.

Andy Crowder.

📩 Want to see how a 24+ year professional options trader approaches the market?

Subscribe to The Option Premium, my free weekly newsletter where I share:

Probability-based strategies that actually work: credit spreads, cash-secured puts, the wheel, LEAPS, poor man's covered calls, and more

Real trade breakdowns with the math behind every decision

Market insights for any environment, whether we're grinding higher, pulling back, or chopping sideways

No hype. No predictions. Just the frameworks I've used to trade options for over two decades.

📺 Want more? Follow me on YouTube for in-depth tutorials, live trade analysis, and the kind of education you won't find anywhere else.

Connect with me:

This newsletter is for educational purposes only and should not be considered investment advice. Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. Always consult with a qualified financial professional before making investment decisions.

Reply